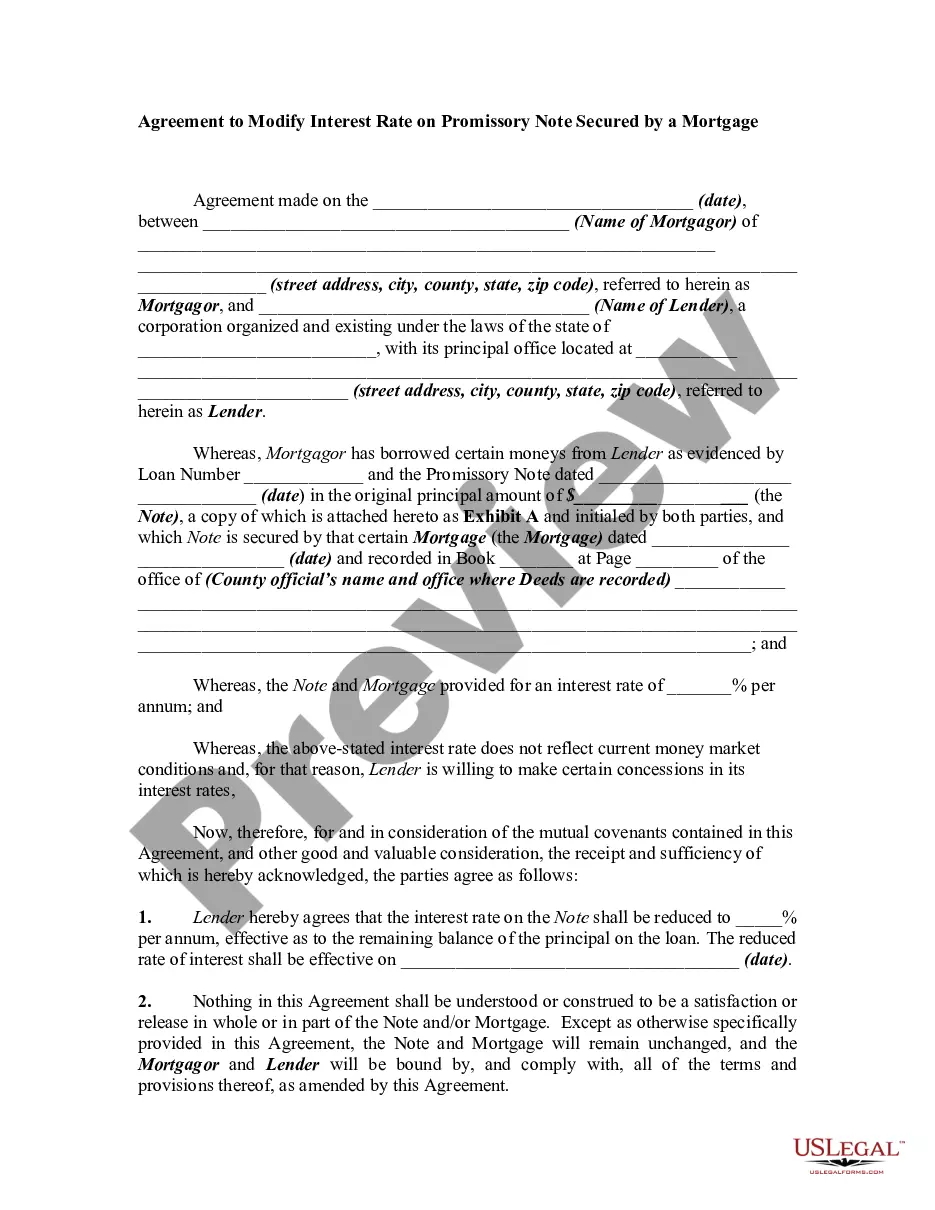

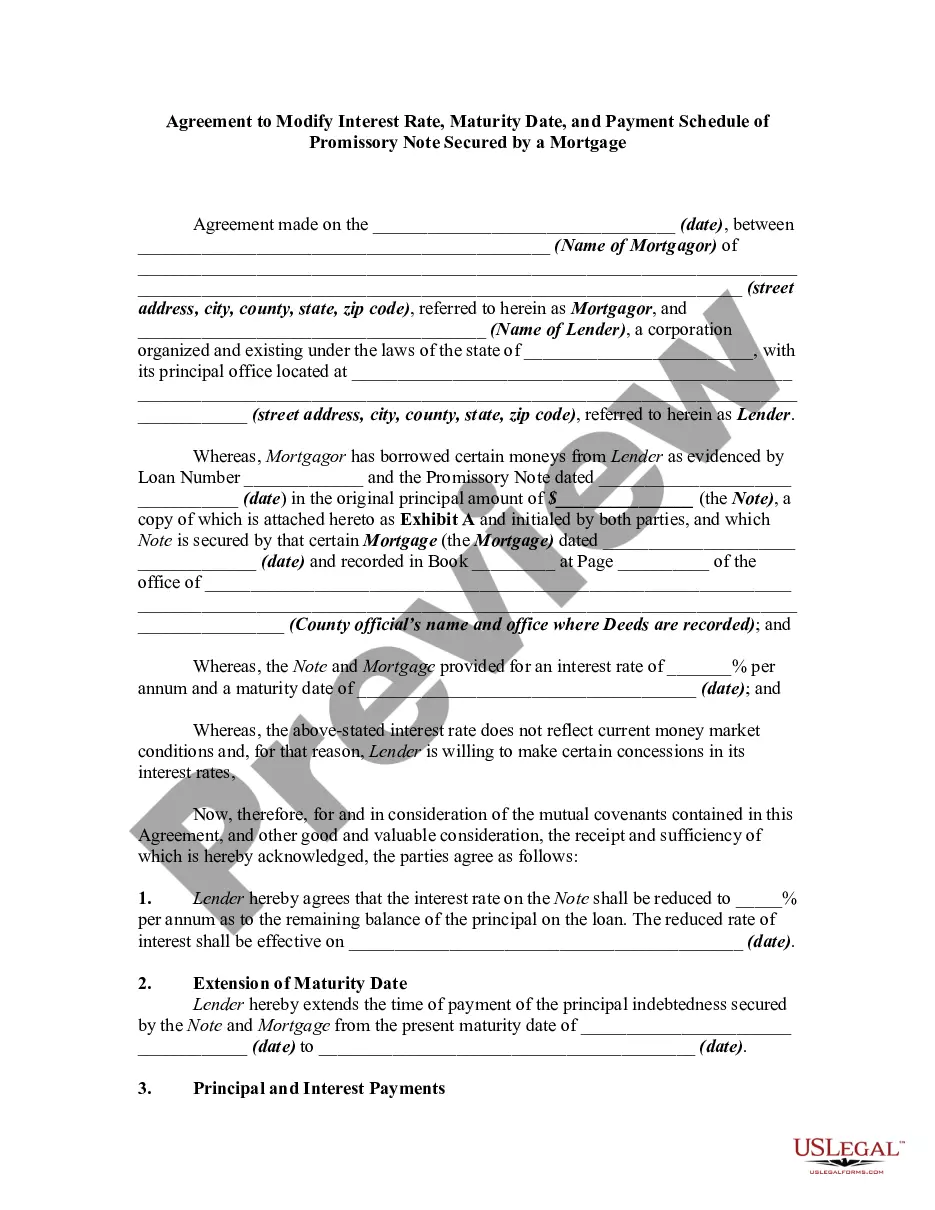

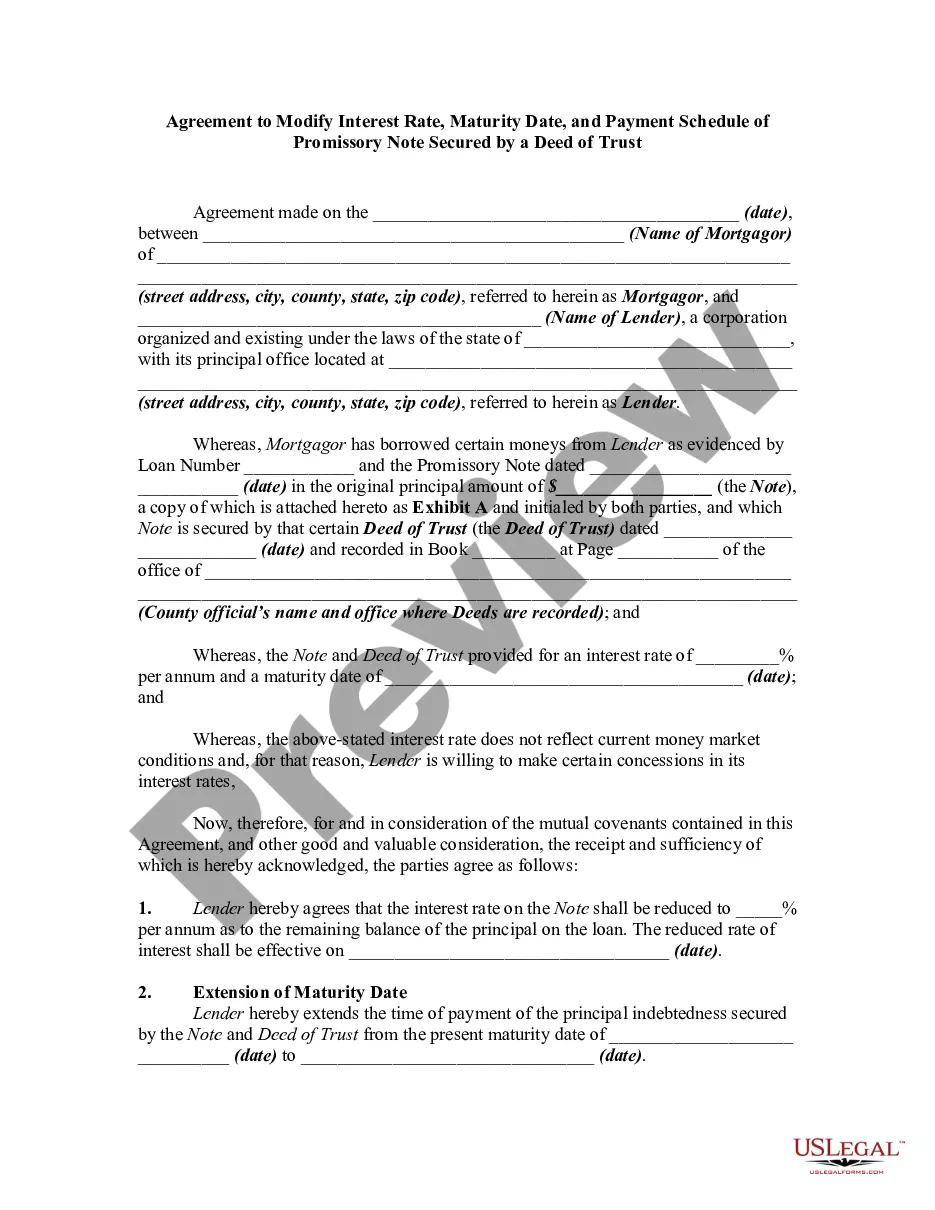

Promissory Note For Extension Of Payment

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Agreement To Modify Promissory Note And Mortgage To Extend Maturity Date?

Handling legal paperwork and processes can be a lengthy addition to your entire day.

Promissory Note For Extension Of Payment and similar forms usually necessitate that you locate them and comprehend how to fill them out accurately.

Thus, whether you are managing financial, legal, or personal issues, utilizing a thorough and user-friendly online directory of forms at your disposal will greatly assist.

US Legal Forms is the premier online platform for legal templates, featuring over 85,000 state-specific documents and a range of resources to facilitate your document completion easily.

Is this your first time using US Legal Forms? Sign up and create an account in a few minutes, and you will gain entry to the form directory and Promissory Note For Extension Of Payment. Then, follow the steps below to finalize your form: Ensure you have found the correct document using the Review feature and examining the form description. Select Buy Now when prepared, and choose the subscription plan that suits you best. Click Download, then fill out, sign, and print the document. US Legal Forms has twenty-five years of experience assisting clients in managing their legal documents. Locate the form you need today and streamline any process effortlessly.

- Explore the collection of pertinent documents accessible to you with just a single click.

- US Legal Forms provides you with state- and county-specific forms available for download at any time.

- Protect your document management procedures by utilizing a top-tier service that enables you to generate any form within minutes without any extra or hidden charges.

- Simply Log In to your account, locate Promissory Note For Extension Of Payment, and retrieve it instantly from the My documents section.

- You can also access previously saved documents.

Form popularity

FAQ

An example of a contract extension clause might state that if the borrower encounters financial difficulties, they may request an extension of the payment term by an additional 30 days. This clause would outline the process for making such a request and any conditions that must be met. Including a well-defined contract extension clause in your promissory note for extension of payment can offer reassurance and clarity to both parties.

An extension clause in a legal document allows for the postponement of a deadline or the extension of a term. This clause can be particularly useful in financial agreements, such as a promissory note for extension of payment, as it provides both parties with a clear understanding of how to handle potential delays. Crafting a precise extension clause helps in maintaining trust and clarity in the agreement.

The promissory note extension clause is a provision that allows the borrower to extend the payment deadline under specific circumstances. This clause can be beneficial in providing flexibility, especially if unforeseen financial challenges arise. Including a well-defined extension clause in your promissory note for extension of payment can help both parties navigate changes in payment schedules smoothly.

To write a promissory note for payment, start by clearly stating the date, names of the parties involved, and the amount owed. Include the repayment terms, interest rates, and any grace periods you wish to allow. Lastly, ensure that both parties sign the document to validate the agreement, providing a clear path for future transactions.

Using a promissory note carries several risks, including potential default by the borrower, which can lead to financial loss for the lender. Additionally, if the terms are unclear, disputes may arise regarding payment schedules or amounts owed. Therefore, it is crucial to draft a clear promissory note for extension of payment to mitigate misunderstandings and protect both parties involved.

The grace period of a promissory note refers to the time allowed after the due date for the borrower to make a payment without incurring penalties. Typically, this period can range from a few days to several weeks, depending on the terms set in the note. Understanding the grace period is essential, especially if you are considering a promissory note for extension of payment, as it provides flexibility in financial planning.

A promissory note can indeed be extended, provided both the borrower and lender agree to the new terms. This extension typically requires a new written agreement that reflects the revised payment schedule. If you need assistance with a promissory note for extension of payment, uslegalforms offers resources to help you draft the necessary documents easily and accurately.

Yes, you can extend a promissory note by creating a new agreement that outlines the updated payment terms. Both parties must agree to the extension and sign the new terms to ensure it is legally binding. If you wish to extend a promissory note for extension of payment, consider using templates available on platforms like uslegalforms to streamline the process.

To write a letter requesting an extension of payment, start by clearly stating your intent and providing relevant details such as the original payment terms and the reason for your request. Be polite and concise, and suggest a new timeline for payment. Utilizing a promissory note for extension of payment can formalize any new agreement and protect both parties' interests.

When a promissory note expires, it typically means that the borrower is no longer legally obligated to repay the debt stated in the note. However, the lender may still have options to recover the amount owed if they act promptly. If you are facing an expired promissory note for extension of payment, consider reaching out to a legal professional for guidance on your next steps.