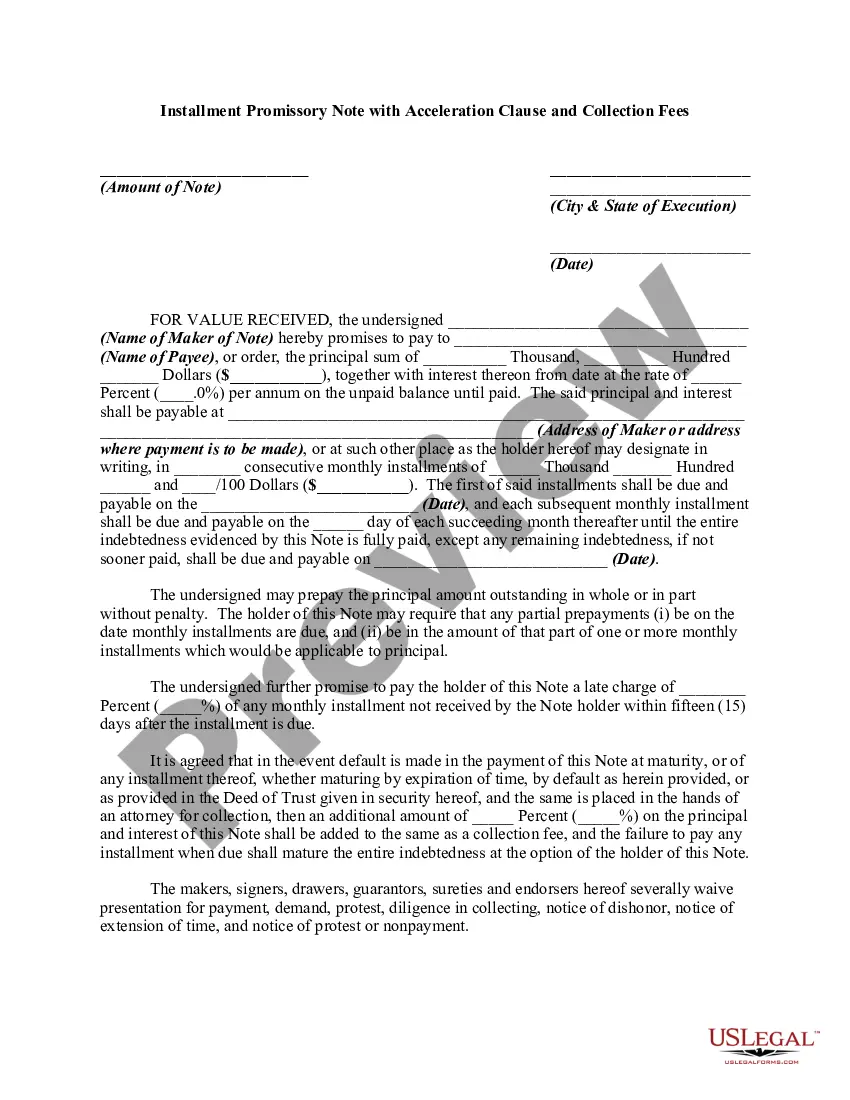

This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

Acceleration Clause In A Mortgage

Category:

State:

Multi-State

Control #:

US-01392BG

Format:

Word;

Rich Text

Instant download

Description Promissory Note With Pdf

Free preview Installment Promissory Note Template