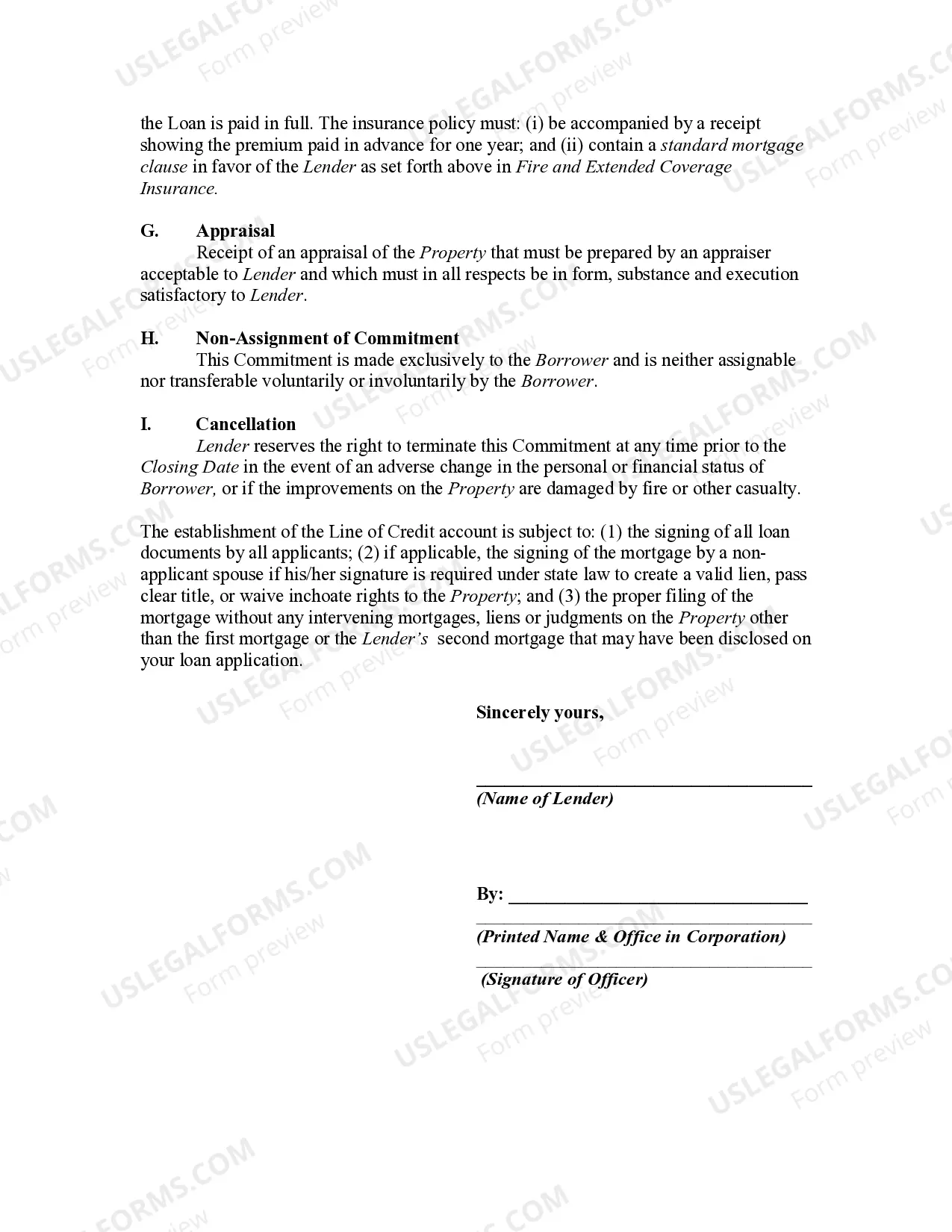

A home equity line of credit is a form of revolving credit in which your home serves as collateral. Because the home is likely to be a consumer's largest asset, many homeowners use their credit lines only for major items such as education, home improvements, or medical bills and not for day-to-day expenses. A home equity line of credit differs from a conventional home equity loan in that the borrower is not advanced the entire sum up front, but uses a line of credit to borrow sums that total no more than the amount, similar to a credit card.

Another important difference from a conventional loan is that the interest rate on a home equity line of credit is variable based on an index such as prime rate. This means that the interest rate can - and almost certainly will - change over time. The margin is the difference between the prime rate and the interest rate the borrower will actually pay.

Title: Personal Loan Agreement Examples: Exploring Different Types and Key Components Introduction: A personal loan agreement is a legally binding contract between a lender and a borrower that outlines the terms and conditions of a personal loan. This agreement provides clarity and protection for both parties involved in the lending process. In this article, we will delve into what a personal loan agreement entails, discuss its key components, and shed light on different types of personal loan agreement examples. Key Components of a Personal Loan Agreement: 1. Parties Involved: The agreement should clearly state the names and contact details of the lender (individual or institution) and the borrower. 2. Loan Amount and Interest: The agreement should specify the principal loan amount and the interest rate applied. Additionally, it may state the method of interest calculation, such as simple or compound interest. 3. Repayment Terms: It is essential to outline the repayment schedule, including the number of installments, their frequency, and the due dates. Details regarding any late payment penalties or grace period should also be mentioned. 4. Collateral or Security: If the loan is secured against an asset, the agreement must describe the pledged collateral, its value, and the consequences of defaulting on repayments. 5. Loan Purpose: This section may mention the purpose for which the loan is being taken, such as debt consolidation, home improvement, education, or medical expenses. 6. Rights and Responsibilities: The agreement should clearly outline the rights and responsibilities of both the lender and the borrower, including any rights to access or inspect the borrower's credit history or financial information. 7. Termination and Default: The process for terminating the agreement, the consequences of defaulting on payments, and potential remedies must be clearly stated. 8. Governing Law and Jurisdiction: The agreement may specify the legal jurisdiction and the governing law that will govern the agreement in case of disputes. Different Types of Personal Loan Agreements: 1. Unsecured Personal Loan Agreement: This type of agreement does not require any collateral, making it suitable for borrowers who do not possess valuable assets. 2. Secured Personal Loan Agreement: In contrast to an unsecured loan, this agreement involves collateral, providing more security for the lender. 3. Co-signer Personal Loan Agreement: In certain situations, a co-signer may be added to the agreement to enhance the borrower's creditworthiness, providing an additional repayment guarantee. 4. Employer-Employee Personal Loan Agreement: This type of agreement is between an employer and an employee, usually offering the employee a personal loan based on their employment contract and salary. Conclusion: Personal loan agreements are crucial documents that help lenders and borrowers establish a clear understanding of their financial obligations. By outlining the key components within a personal loan agreement and discussing different types of agreements, borrowers can be equipped with the necessary knowledge to make informed decisions and protect their interests. Remember, it is always advisable to consult with legal professionals to ensure the agreement complies with local laws and regulations.