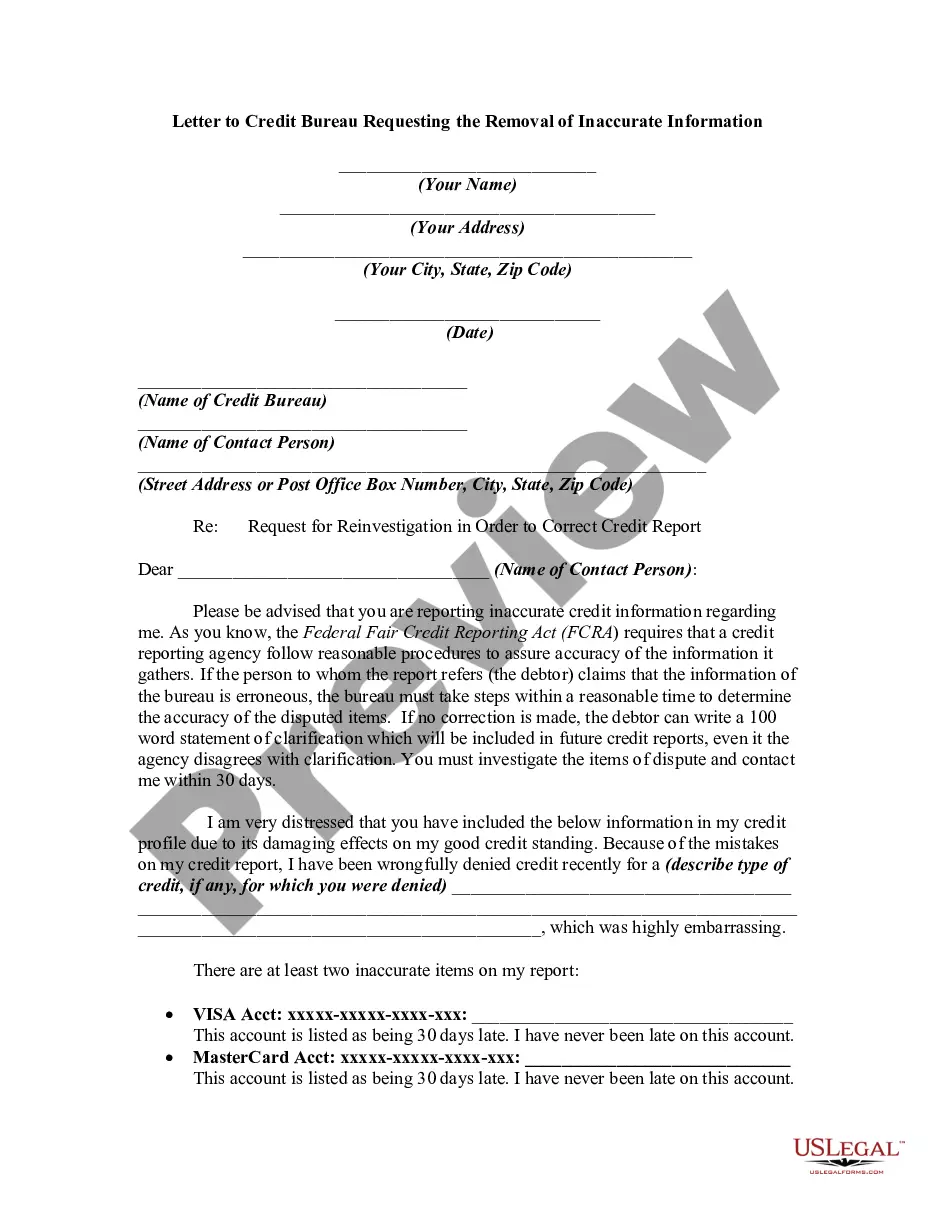

This form is a sample letter requesting the removal of inaccurate information. Always include any copies of proof you may have (e.g., copies of cancelled checks showing timely payments). If the person claims that the information of the bureau is erroneous, the bureau must take steps within a reasonable time to determine the accuracy of the disputed items. If no correction is made, the debtor can write a 100 word statement of clarification which will be included in future credit reports, even it the agency disagrees with clarification.

A credit dispute letter for hard inquiries is a written communication that consumers use to dispute or challenge the inclusion of certain hard inquiries on their credit reports. It is an effective way to address potential inaccuracies, unauthorized inquiries, or inquiries that are no longer relevant. Hard inquiries are created when a lender or creditor accesses a consumer's credit report to make a lending decision, such as when applying for a credit card, a loan, or a mortgage. These inquiries can have a temporary impact on an individual's credit score and may be seen by other potential lenders or creditors when assessing creditworthiness. However, when there are hard inquiries that are incorrect or unauthorized, it is crucial to take action to have them removed. A credit dispute letter for hard inquiries should include relevant information such as the consumer's name, address, and phone number. It should also clearly specify the disputed hard inquiries, providing details such as the inquiry date, the name of the creditor or lender, and any other pertinent information found on the credit report. Additionally, the consumer should explain the reasons for disputing each hard inquiry and provide any supporting documents that can back up their claims. There are different types of credit dispute letters for hard inquiries, depending on the nature of the inquiries and the consumer's circumstances. These may include: 1. Inquiries resulting from identity theft: If a consumer suspects that certain hard inquiries were made without their consent due to identity theft, they can write a credit dispute letter specifically addressing this issue. This type of letter should highlight the unauthorized inquiries, provide details of the identity theft incident, and include any supporting evidence or documentation provided by law enforcement or credit monitoring agencies. 2. Inquiries due to errors or inaccuracies: Sometimes, credit reports may contain incorrect information regarding hard inquiries. Consumers can draft a credit dispute letter focused on disputing these inaccuracies, explaining which specific inquiries are incorrect and providing evidence to support their claims. This could include documentation showing that the consumer did not apply for credit with the creditor or lender in question. 3. Unverified inquiries or inquiries for which there is no permissible purpose: In some cases, a consumer might discover that specific hard inquiries were made without their authorization or without a permissible purpose under the Fair Credit Reporting Act (FCRA). In these instances, a credit dispute letter can help challenge these inquiries and request their removal from the credit report. The letter should clearly state that there was no legitimate reason for the inquiry and emphasize the consumer's rights under the FCRA. It is essential to send credit dispute letters via certified mail with a return receipt requested. This way, consumers have proof of their communication and the date it was received by the credit reporting agencies. Additionally, it is advisable to keep copies of all correspondence, including the credit dispute letter itself, as well as any attached supporting documentation. Overall, a credit dispute letter tailored specifically to hard inquiries is an effective tool for consumers wanting to correct inaccuracies, remove unauthorized inquiries, or address inquiries that no longer hold relevance. By providing relevant information, explaining the reasons for the dispute, and including any supporting documentation, individuals can increase the likelihood of a successful resolution and maintain accurate credit reports.