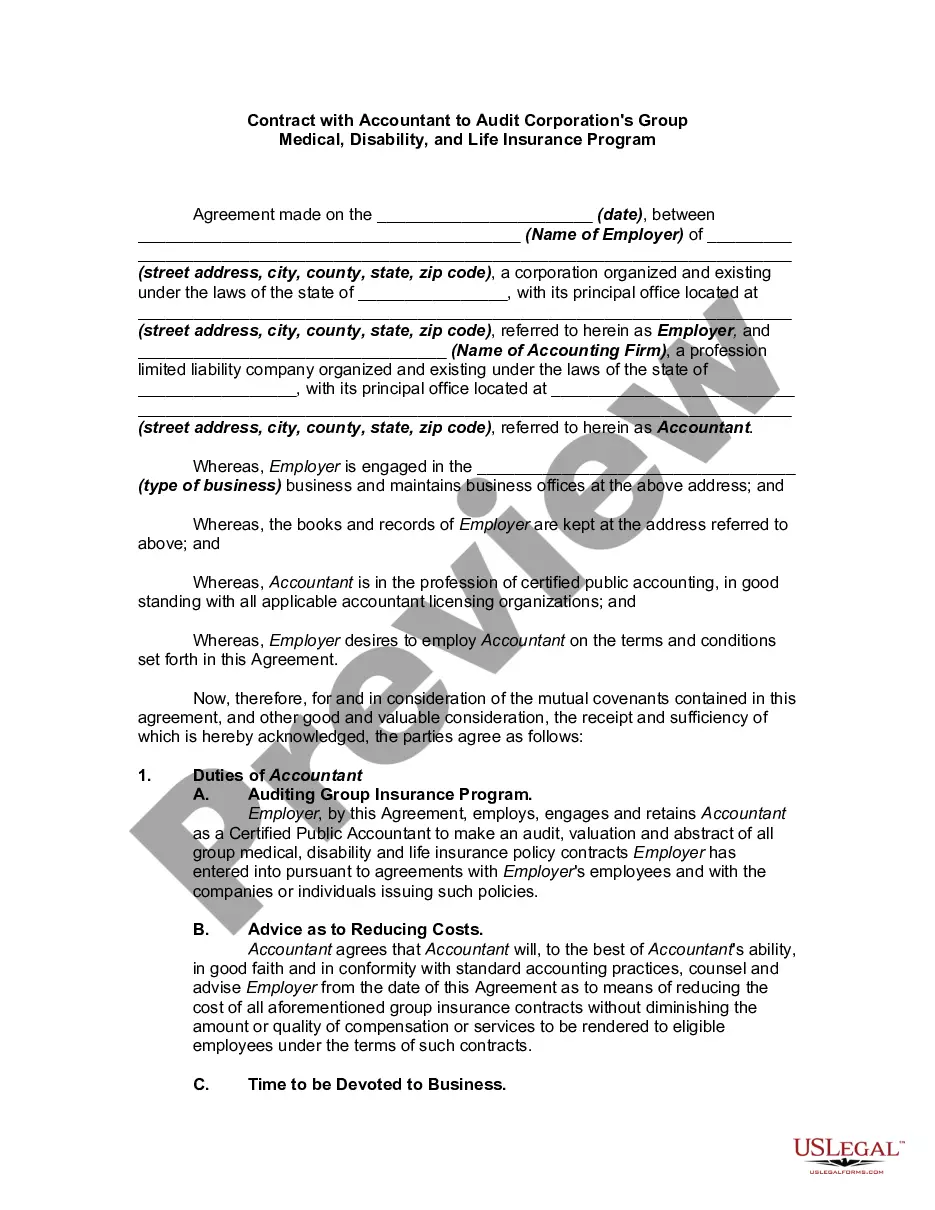

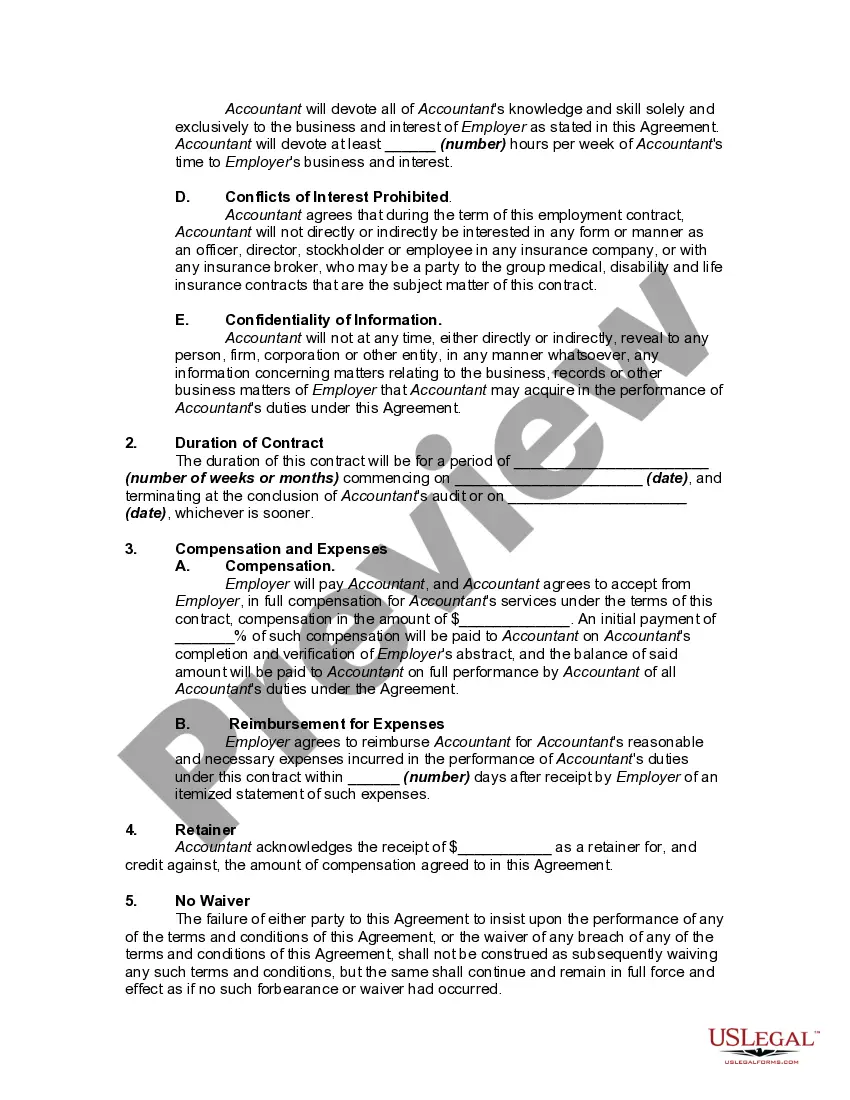

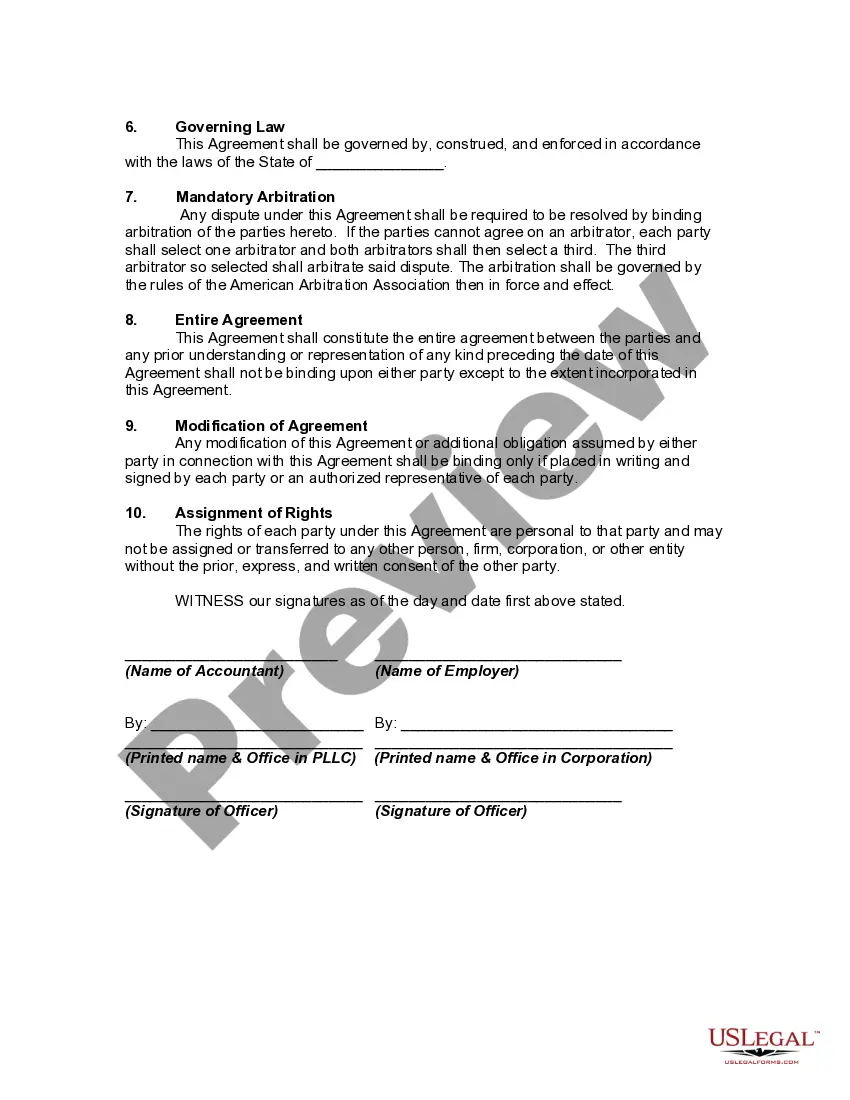

Generally, a contract to employ a certified public accountant need not be in writing.

However, such contracts often call for services of a highly complex and technical nature, and hence they should be explicit in their terms, and they should be in writing. In particular, a written employment contract is necessary in order to avoid misunderstanding with the employer regarding the amount of the accountant's fee or compensation and the nature of its computation. This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

Accounting for insurance proceeds is a process adopted by insurance companies to appropriately record and report the financial impact of insurance claims. The accounting methods used for insurance proceeds are crucial in ensuring accurate financial statements and compliance with accounting standards. PricewaterhouseCoopers (PwC), a renowned accounting firm, offers expertise and guidance in this regard. One type of accounting for insurance proceeds is the recognition and measurement of an insurance claim. When an insured event occurs, such as property damage or an accident, the insured party can file a claim with their insurance company. PwC advises on the assessment of the claim's validity and quantification of the probable amount to be received. This involves analyzing the insurance policy, scrutinizing the extent of coverage, and determining the fair value of the loss or damage. Another aspect of accounting for insurance proceeds is the timing of recognition. PwC helps insurance companies determine the appropriate point at which to recognize the insurance proceeds in their financial statements. This involves considering factors such as the occurrence of the insured event, the completion of any necessary investigations, and the likelihood of receiving the funds. PwC also provides guidance on the presentation and disclosure of insurance proceeds in financial statements. Insurance companies need to clearly disclose the nature and extent of insurance-related transactions, including the significant terms and conditions of the policies, the amounts received, and any contingent liabilities. Proper presentation ensures transparency and allows stakeholders to make informed decisions. Furthermore, PwC offers expertise in determining the tax implications of insurance proceeds. Depending on the jurisdiction and the nature of the insurance claim, tax regulations may require specific treatment of the proceeds. PwC helps navigate through these complexities, ensuring compliance with tax laws and optimizing tax implications for insurance companies. In summary, Accounting for insurance proceeds PwC involves the recognition, measurement, timing, presentation, disclosure, and tax treatment of insurance claims. It encompasses thorough analysis of insurance policies, assessment of claims, quantification of losses, and appropriate recording and reporting in financial statements. By following PwC's guidance, insurance companies can accurately reflect the financial impact of insurance claims, comply with accounting standards, and provide transparent financial information to stakeholders.