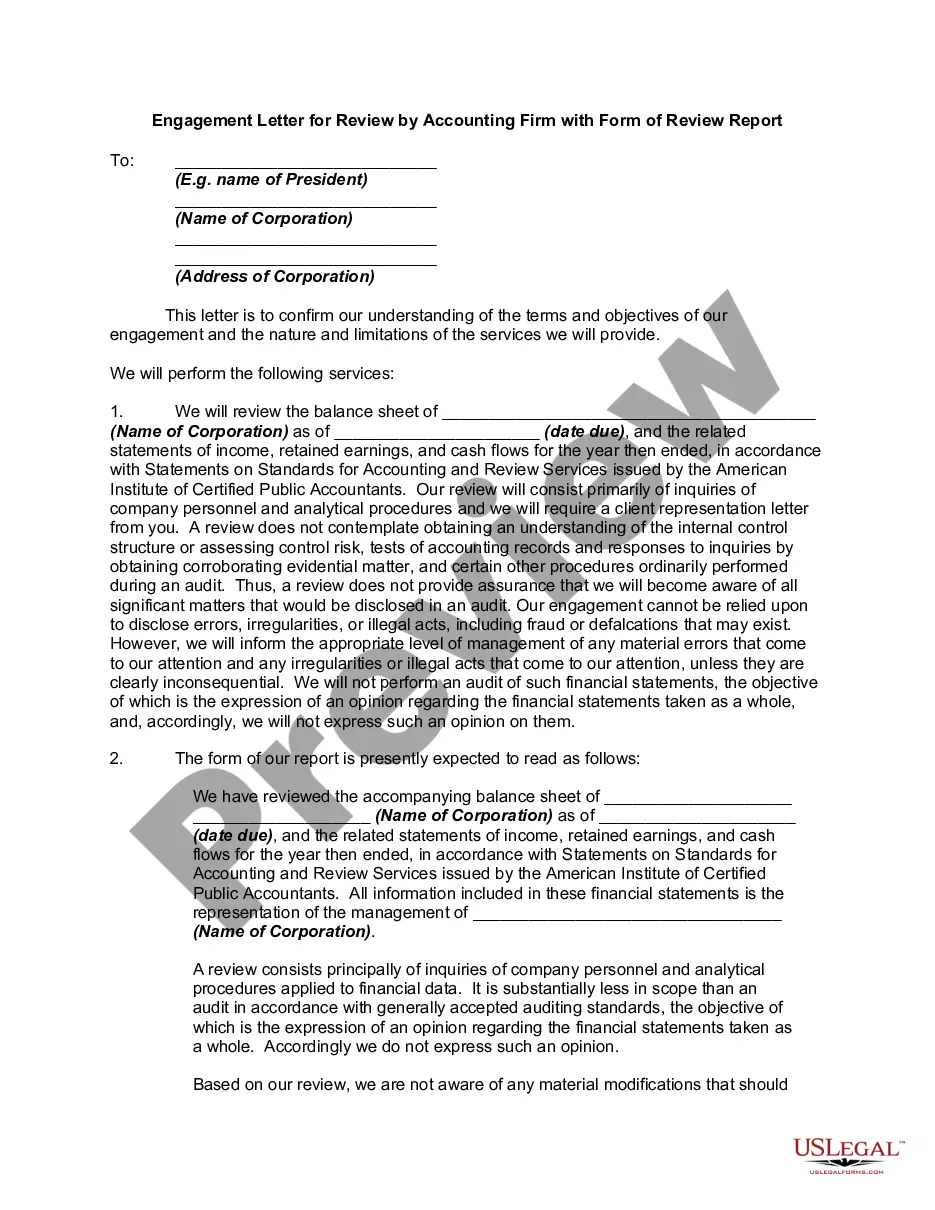

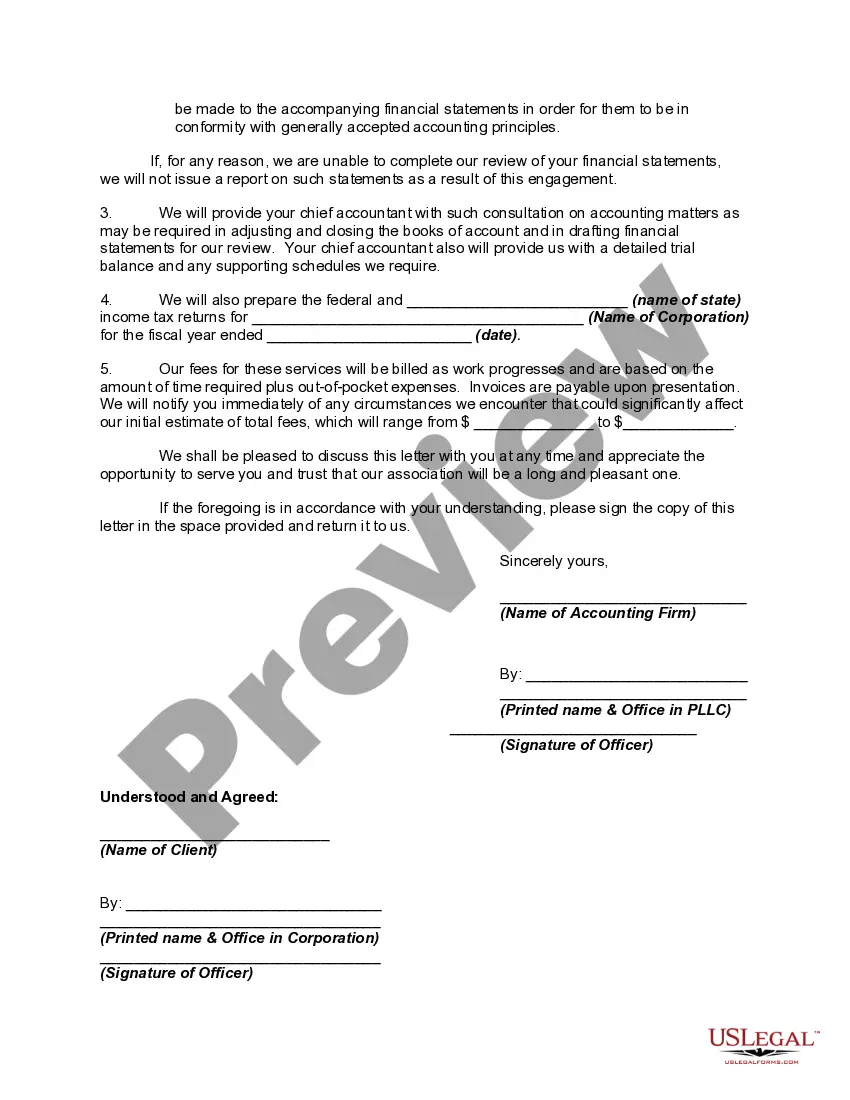

Generally, a contract to employ a certified public accountant need not be in writing. However, such contracts often call for services of a highly complex and technical nature, and hence they should be explicit in their terms, and they should be in writing. In particular, a written employment contract is necessary in order to avoid misunderstanding with the employer regarding the amount of the accountant's fee or compensation and the nature of its computation. This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

Audit Engagement Letter Example with Internal An audit engagement letter is a formal document that outlines the terms and conditions of an audit engagement between an auditor or an auditing firm and their client. It serves as a legal contract that establishes the responsibilities, objectives, and scope of the audit. In the case of an internal audit engagement, the auditor is an employee or a representative of the company conducting the audit. This type of audit is focused on evaluating and improving internal controls, risk management processes, and compliance with company policies and procedures. An example of an audit engagement letter with internal responsibilities may include the following key elements: 1. Introduction: The letter should start with a formal introduction stating the purpose and objectives of the audit engagement. It should clearly state that the audit is an internal one, conducted by an independent internal auditor. 2. Scope of Work: The engagement letter should clearly define the scope of the audit, specifying the areas to be reviewed, such as financial statements, internal controls, and risk management processes. It should also mention any limitations, such as restricted access to certain documents or departments. 3. Timelines: The letter should specify the timeline for the audit, including the start and end dates, as well as key milestones and deliverables. This ensures that both the auditor and the client are aware of the time commitments required for the engagement. 4. Audit Procedures: The engagement letter should outline the specific audit procedures to be performed, such as interviews, document reviews, observation of processes, and testing of controls. It should also mention the use of any specialized software or tools to facilitate the audit process. 5. Confidentiality and Independence: The letter should highlight the auditor's commitment to maintaining confidentiality and independence throughout the engagement. It should state that the auditor will not disclose any sensitive or proprietary information without proper authorization. 6. Reporting: The engagement letter should specify the format and content of the audit report to be produced at the conclusion of the engagement. It should also mention any interim reporting requirements and the audience to whom the report will be shared. Types of internal audit engagement letters may vary depending on the nature and objectives of the audit. Some common types include: 1. Financial Statement Audit Engagement Letter: Focuses on the audit of financial statements to ensure their accuracy, completeness, and compliance with accounting standards. 2. Compliance Audit Engagement Letter: Concentrates on evaluating the company's adherence to legal, regulatory, and internal policy requirements. 3. Operational Audit Engagement Letter: Aims to assess the efficiency and effectiveness of operational processes, including risk management, internal controls, and performance metrics. 4. Information Systems Audit Engagement Letter: Targets the evaluation of IT systems, data security measures, and the effectiveness of internal controls related to information technology. In conclusion, an audit engagement letter with internal responsibilities is a crucial document that establishes the scope, objectives, and terms of an internal audit engagement. It ensures clarity and understanding between the auditor and the client, setting the stage for a successful and productive audit.