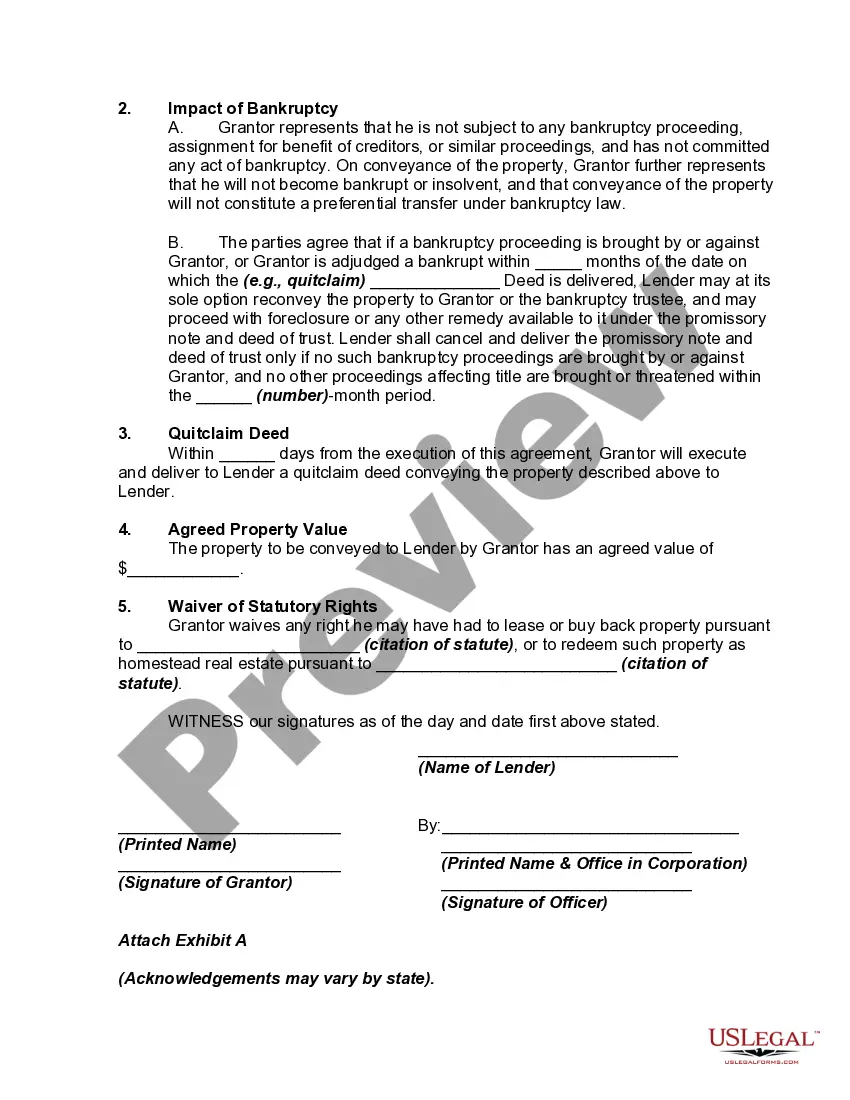

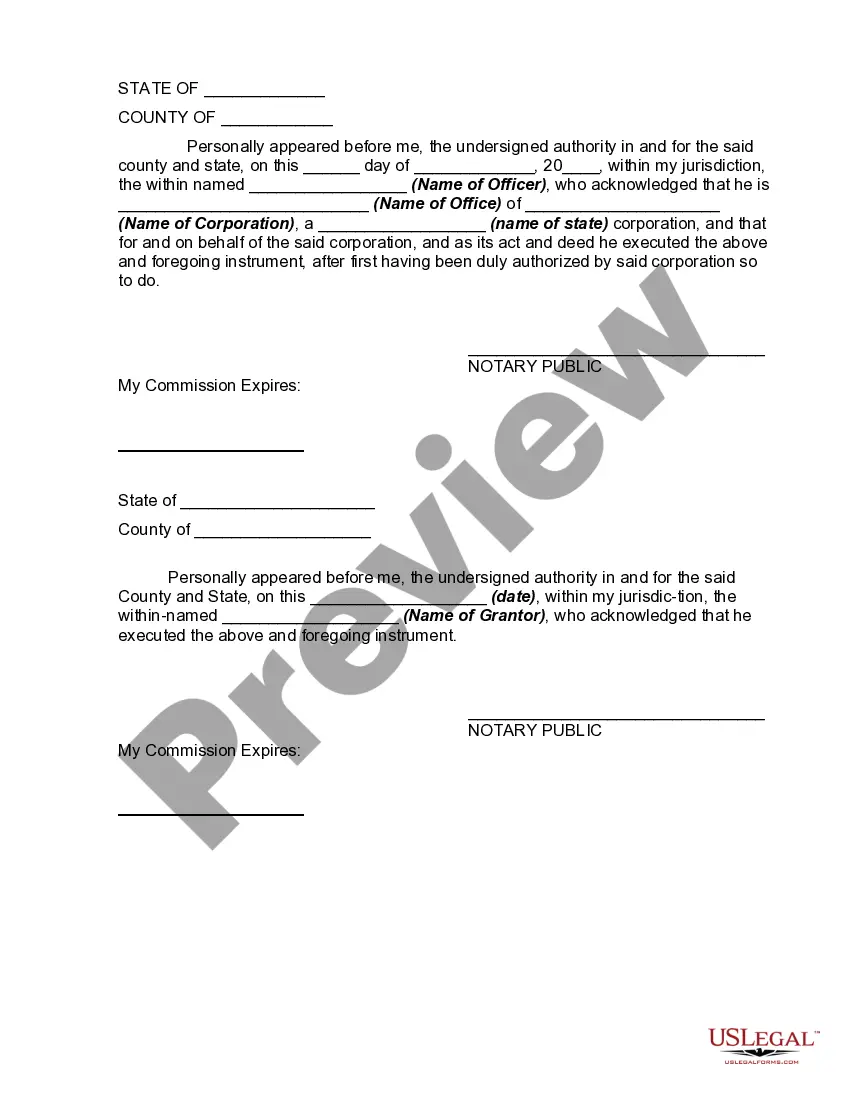

Deed in lieu of foreclosure is a legal agreement that occurs between a homeowner and their mortgage lender. It is typically used as an alternative to foreclosure when the borrower is unable to make their mortgage payments and decides to voluntarily transfer the ownership of the property to the lender in exchange for the cancellation of the remaining debt. In regard to a Deed in lieu of foreclosure sample for individuals with no experience in this process, it is crucial to understand the key elements involved. Firstly, it is important to note that while many foreclosures may vary in terms of their specific requirements, the general purpose remains consistent — to avoid the lengthy and costly foreclosure process. Although there aren't multiple types of Deed in lieu of foreclosure based on experience levels, it is essential to comprehend the critical steps involved in such a process. Here is a detailed walkthrough of a Deed in lieu of foreclosure sample for those with no experience: 1. Open Communication: Initiate open and honest communication with your mortgage lender. Inform them of your financial hardship and inability to make mortgage payments. This transparency is crucial for lenders to assess your situation and evaluate eligibility for a Deed in lieu of foreclosure. 2. Documentation: Prepare and gather necessary documentation, such as financial statements, bank statements, pay stubs, proof of income, and any supporting documents that reflect your current financial hardship. These documents will help authenticate your claim and support your eligibility for a Deed in lieu of foreclosure. 3. Consultation: Seek advice from a real estate attorney, housing counselor, or financial advisor who specializes in foreclosure prevention. They can guide you through the process, be your legal representative, review the Deed in lieu of foreclosure agreement, and protect your interests. 4. Application Submission: Complete the necessary paperwork provided by your lender. This typically includes a Deed in lieu of foreclosure application form, financial statements, hardship letter, and any additional documents mandated by the lender. Ensure that all information is accurate and correctly documented. 5. Lender Evaluation: The lender will review your application, assess the documentation provided, and determine your eligibility for a Deed in lieu of foreclosure. They will verify your financial hardship and evaluate the market value of the property to ascertain its worth. 6. Negotiations: Once your application is approved, negotiations will commence between you and the lender. These negotiations will involve aspects such as the release of liability for any remaining debt, potential financial assistance to help with relocation costs, and any other terms and conditions pertaining to the transfer of property ownership. 7. Settlement Agreement: If both parties reach a mutual agreement, a settlement agreement will be drafted, outlining the terms and conditions of the Deed in lieu of foreclosure. Ensure the agreement is thoroughly reviewed and understood before signing to prevent any potential legal ramifications in the future. By following this Deed in lieu of foreclosure sample with no experience, individuals facing financial hardship and foreclosure can explore alternatives that might alleviate their situation. Remember, consulting with professionals in this field is essential to navigate the complex legalities involved.

Deed In Lieu Of Foreclosure Sample With No Experience

Description Foreclosure

How to fill out Deed In Lieu Of Foreclosure Example?

It’s obvious that you can’t become a law expert immediately, nor can you grasp how to quickly draft Deed In Lieu Of Foreclosure Sample With No Experience without the need of a specialized background. Putting together legal forms is a time-consuming venture requiring a certain education and skills. So why not leave the creation of the Deed In Lieu Of Foreclosure Sample With No Experience to the professionals?

With US Legal Forms, one of the most comprehensive legal template libraries, you can access anything from court documents to templates for internal corporate communication. We know how important compliance and adherence to federal and state laws are. That’s why, on our platform, all forms are location specific and up to date.

Here’s start off with our platform and obtain the document you require in mere minutes:

- Find the document you need by using the search bar at the top of the page.

- Preview it (if this option available) and read the supporting description to figure out whether Deed In Lieu Of Foreclosure Sample With No Experience is what you’re searching for.

- Begin your search again if you need any other form.

- Set up a free account and choose a subscription plan to purchase the template.

- Pick Buy now. As soon as the transaction is through, you can download the Deed In Lieu Of Foreclosure Sample With No Experience, complete it, print it, and send or send it by post to the necessary individuals or organizations.

You can re-access your forms from the My Forms tab at any time. If you’re an existing client, you can simply log in, and find and download the template from the same tab.

No matter the purpose of your forms-be it financial and legal, or personal-our platform has you covered. Try US Legal Forms now!