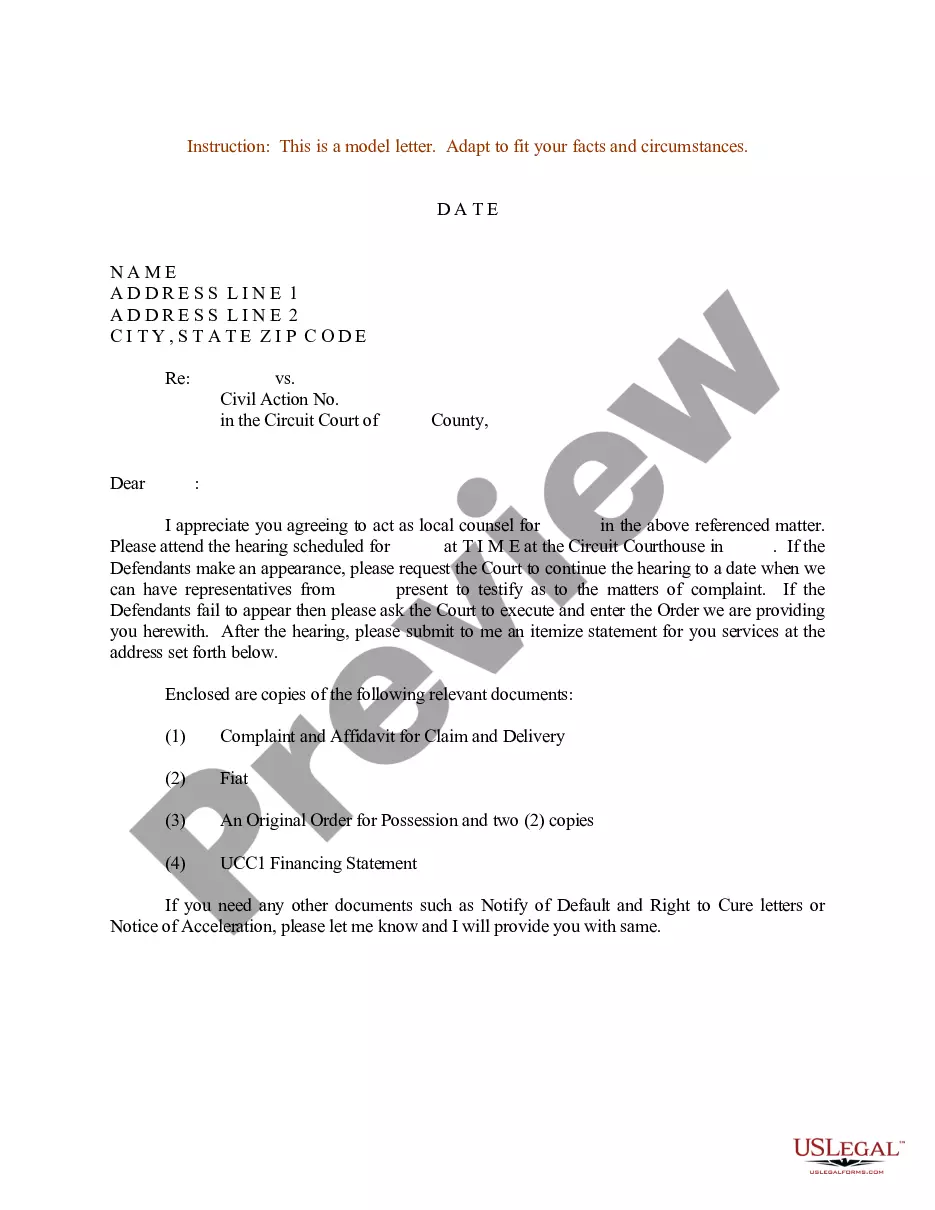

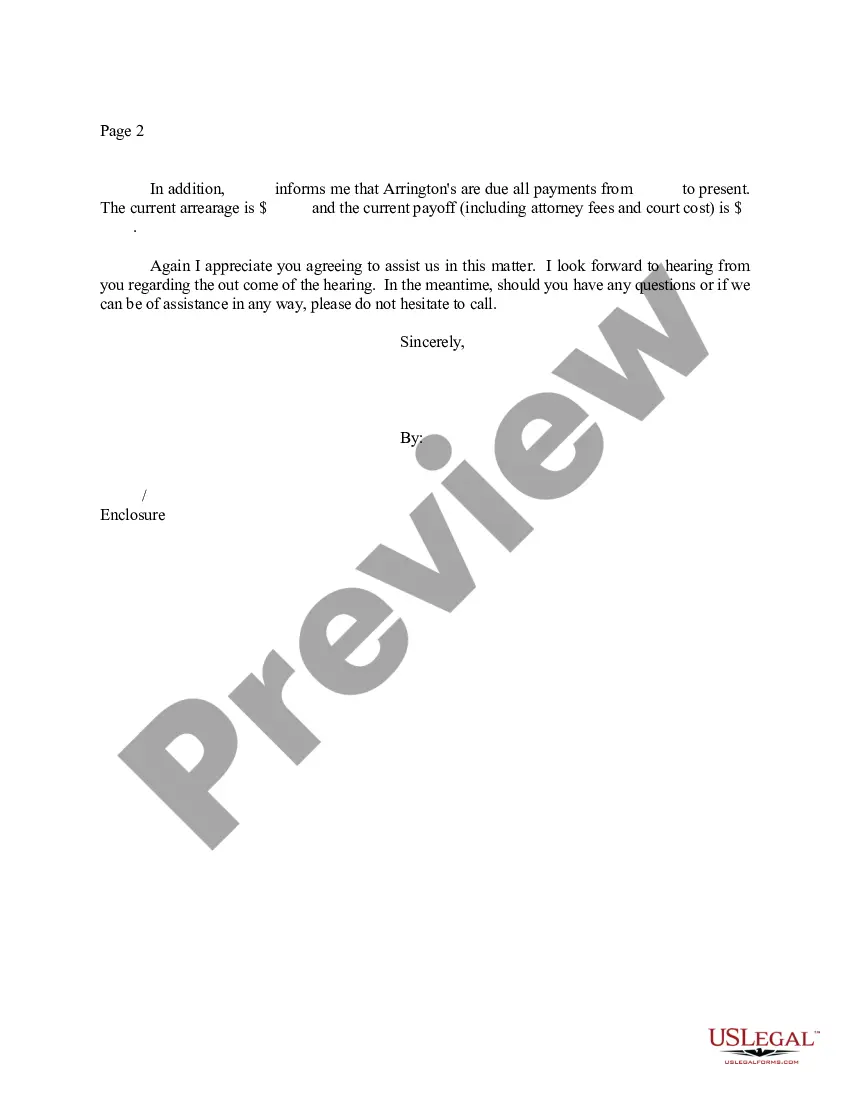

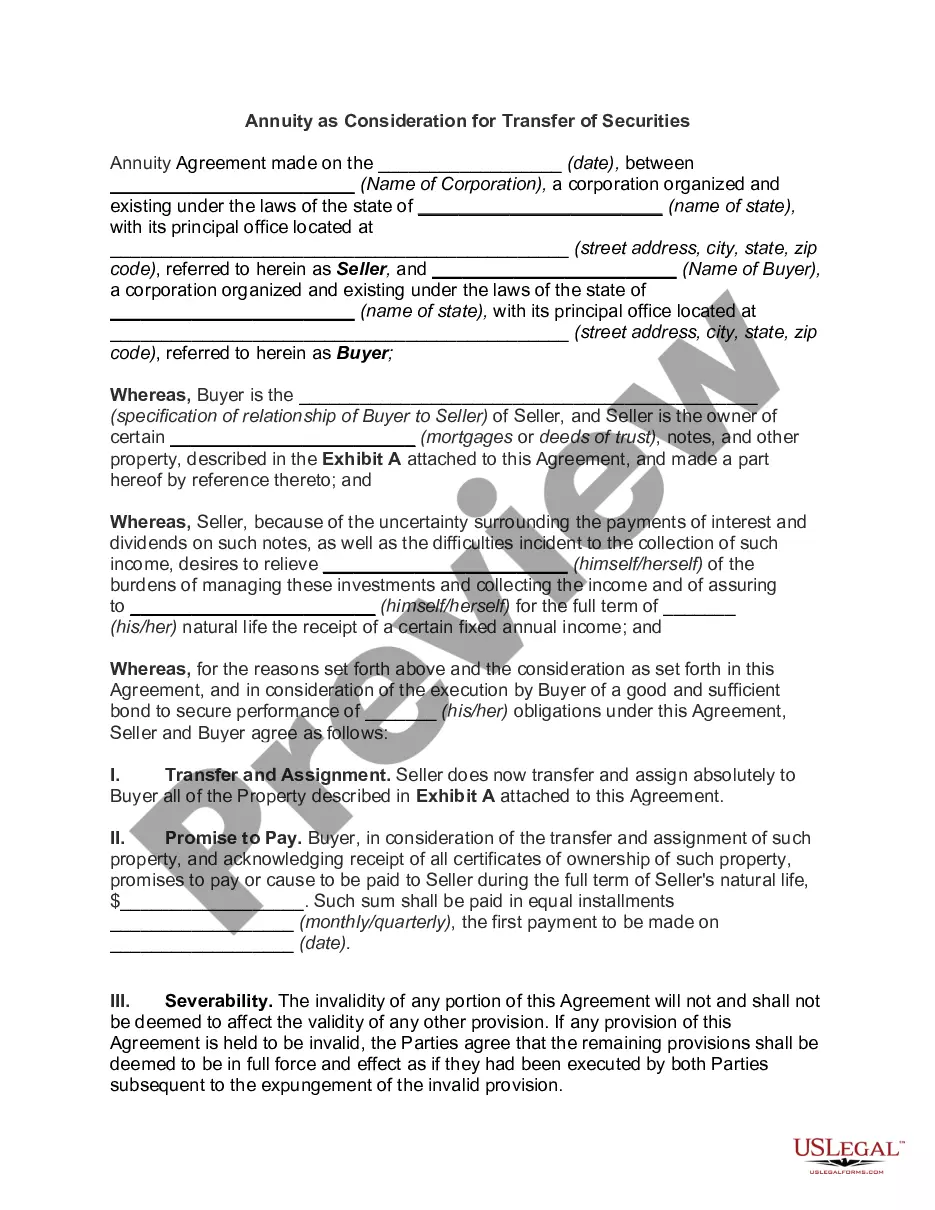

A Letter of Instruction to a financial institution is a written document that provides clear and specific instructions to guide the actions of the institution regarding a customer's financial affairs. This letter serves as a formal communication tool between the account holder and the financial institution, ensuring efficient and accurate execution of tasks. The primary purpose of a Letter of Instruction is to outline the account holder's desires and preferences, especially when it comes to financial transactions or account management. It clarifies the account holder's intentions and acts as a reference for the financial institution to follow in case of any uncertainties or conflicting instructions. There are different types of Letters of Instruction to financial institutions, depending on their specific purpose and scope. Let's explore a few common variations: 1. Account Management Letter of Instruction: This type of letter provides instructions related to day-to-day account management activities. It might include guidance on account preferences, such as selecting a primary contact person, updating contact information, or subscribing/deactivating specific services like online banking or overdraft protection. 2. Payment Instructions Letter: This letter explicitly instructs the financial institution on how to handle and process various payment transactions. It may include stipulations on bill payments, transfers to other accounts, setting up recurring payments or direct deposits, or managing standing orders. 3. Investment Letter of Instruction: This type of letter focuses on providing directives for investment-related activities, typically for brokerage accounts or investment portfolios. It might include instructions on buying or selling securities, asset allocation changes, dividend reinvestment preferences, or tax-lot selection strategies. 4. Estate Planning Letter: A letter of instruction can be used to outline specific requests for estate planning purposes. It commonly includes information concerning the distribution of assets after the account holder's demise, designation of beneficiaries, and various details necessary for executing a trust or will. 5. Loan or Mortgage Instruction Letter: In the case of loans or mortgages, a letter of instruction might be employed to convey specifics related to repayments, loan modifications, or requesting adjustments to payment schedules. It provides a clear record of the borrower's intentions and expectations. When crafting a Letter of Instruction to a financial institution, it is crucial to ensure clarity, conciseness, and accuracy in the content. Additionally, legal and personalized financial advice should always be sought to tailor the letter to individual circumstances and to comply with any regulatory requirements imposed by the specific financial institution.

Letter Of Instruction To Financial Institution

Description beneficiary financial institution

How to fill out Letter Of Instruction To Financial Institution?

Whether for business purposes or for individual matters, everyone has to handle legal situations sooner or later in their life. Completing legal documents requires careful attention, starting with picking the proper form sample. For instance, when you choose a wrong edition of the Letter Of Instruction To Financial Institution, it will be rejected when you submit it. It is therefore important to get a dependable source of legal files like US Legal Forms.

If you have to get a Letter Of Instruction To Financial Institution sample, stick to these simple steps:

- Find the sample you need by utilizing the search field or catalog navigation.

- Check out the form’s description to make sure it matches your situation, state, and county.

- Click on the form’s preview to see it.

- If it is the wrong document, go back to the search function to find the Letter Of Instruction To Financial Institution sample you need.

- Download the file if it matches your requirements.

- If you have a US Legal Forms account, simply click Log in to gain access to previously saved templates in My Forms.

- In the event you do not have an account yet, you can obtain the form by clicking Buy now.

- Pick the proper pricing option.

- Finish the account registration form.

- Pick your transaction method: you can use a bank card or PayPal account.

- Pick the document format you want and download the Letter Of Instruction To Financial Institution.

- When it is downloaded, you are able to complete the form with the help of editing software or print it and finish it manually.

With a large US Legal Forms catalog at hand, you never need to spend time searching for the right sample across the internet. Make use of the library’s easy navigation to get the proper form for any occasion.

bank instruction letter Form popularity

institutional letter Other Form Names

FAQ

Florida Enforcement of Foreign Judgment Act was established to allow holders of uncollected foreign judgments to domesticate the judgment and have a writ of execution issued in the Florida county where the judgment is recorded without having to file suit or pay a filing fee.

Domestication is the process that allows a creditor to attach the judgment as a lien to the debtor's property, and otherwise enforce it.

For a non-reciprocating territory, a foreign judgment may be enforced by filing a new suit in an Indian court within a period of three years as specified under the Limitation Act, 1963, commencing from the date on which the judgment was passed by the foreign court.

Rule 25.1 - Withdrawal, Substitution, and Appearance of Counsel (a) Except as provided in Rule 10(c) of the Rules of the Circuit Courts, withdrawal and substitution of counsel in cases pending before the circuit courts shall be effective only upon the approval of the court and shall be subject to the guidelines of Rule ...

A foreign judgment, when conclusive under section 13 of the Code of Civil Procedure, 1908, may be pleaded as a defence as a bar to a suit in India1 provided it is given on the merits2 as prescribed by section 13. 1. Chockalingam v. Duraiswami, AIR 1928 Mad 327 (336).

Generally, US judgments cannot be enforced in a foreign country without first being recognized by a court in that foreign country. The recognition and enforcement of US judgments depends not only on the domestic law of the foreign country, but also on the principles of comity, reciprocity and res judicata.

On motion and upon such terms as are just, the court may relieve a party or a party's legal representative from a final judgment, order, or proceeding for the following reasons: (1) mistake, inadvertence, surprise, or excusable neglect; (2) newly discovered evidence which by due diligence could not have been discovered ...