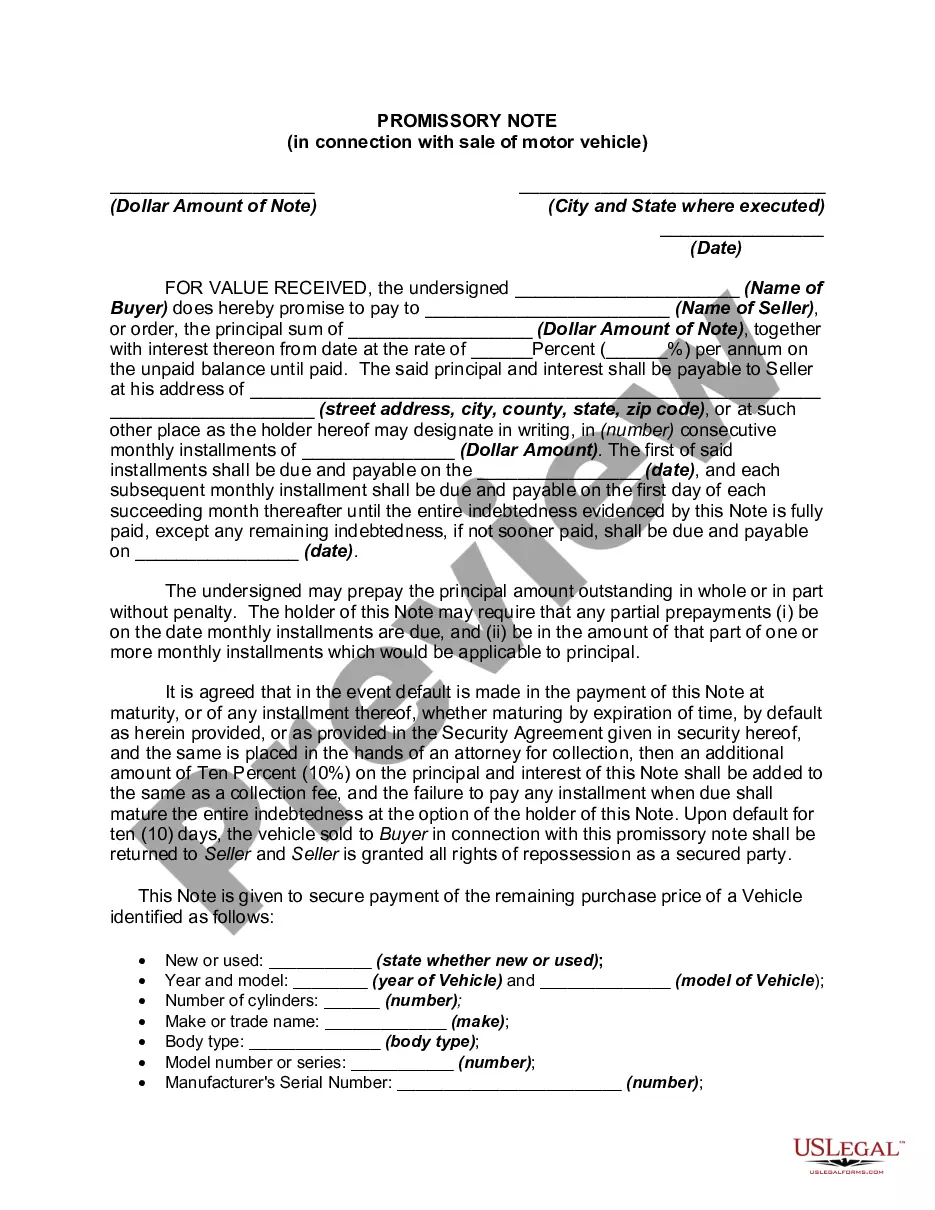

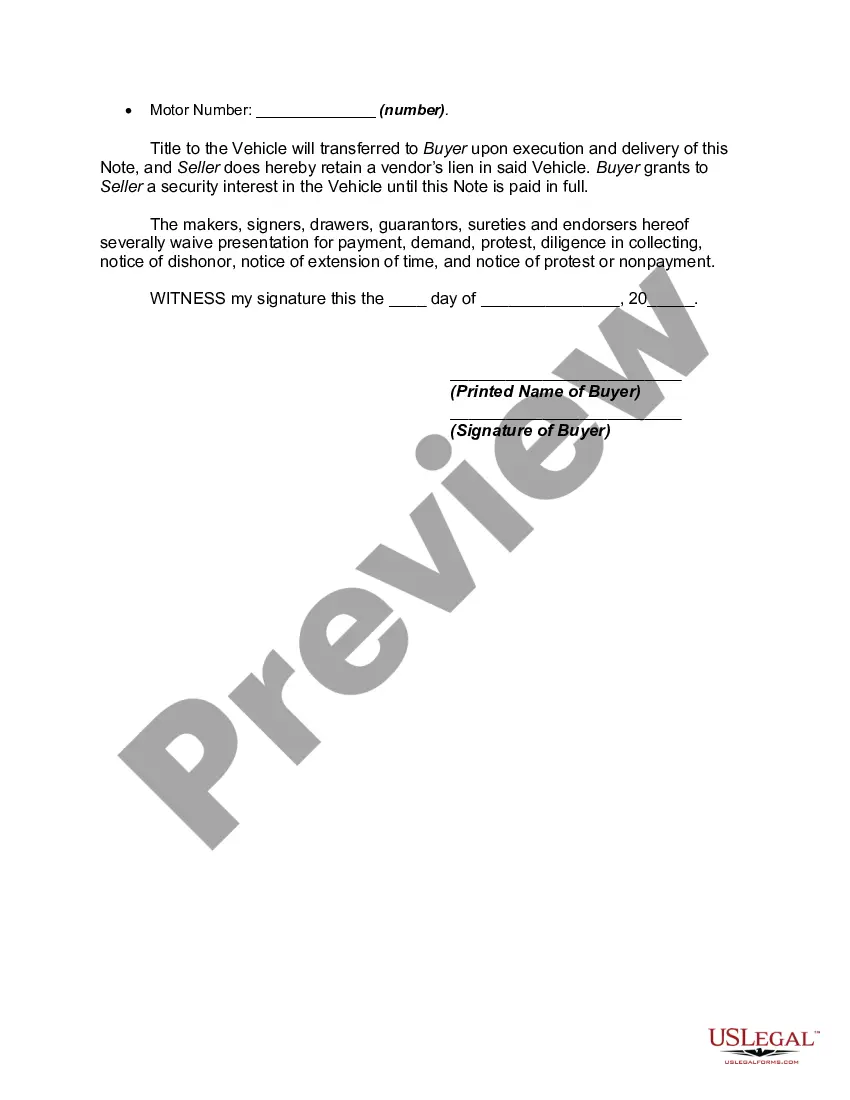

A promissory note should have several essential elements, including the amount of the loan, the date by which it is to be paid back, the interest rate, and a record of any collateral that is being used to secure the loan. Default terms (what happens if a payment is missed or the loan is not paid off by its due date) should also be spelled out in the promissory note.

Note pay vehicle with loan is a financial arrangement where an individual or a business obtains a loan to purchase a vehicle. The loan is secured by the vehicle, and the borrower agrees to make regular payments, including principal plus interest, until the loan is fully repaid. This type of vehicle financing is commonly used by individuals who are purchasing a new or used car, truck, motorcycle, or any other motor vehicle. Note pay vehicle with loan offers a convenient way for individuals to acquire a vehicle without paying the full purchase price upfront. Instead, they can spread out the cost over a specified period, usually ranging from a few months to several years, depending on the loan terms. The loan agreement typically outlines the interest rate, repayment schedule, and the consequences of defaulting on the loan. There are several types of note pay vehicle loans available in the market, each catering to different financing needs: 1. Auto loans: These loans are specifically designed for individuals purchasing cars, trucks, SUVs, or any other type of automobile. 2. Motorcycle loans: For those interested in financing the purchase of a motorcycle, this type of loan provides the necessary funds. 3. RV loans: Recreational Vehicle (RV) loans are intended for individuals looking to purchase motor homes, campers, or travel trailers. 4. Boat loans: These loans cater to individuals wanting to finance the purchase of boats, yachts, or any other type of watercraft. 5. Commercial vehicle loans: Designed for businesses, these loans help finance the purchase of commercial vehicles like delivery trucks, vans, or heavy-duty vehicles. Note pay vehicle loans provide individuals and businesses with flexibility and affordability in acquiring their desired vehicles. However, it's important to carefully consider the interest rates, loan terms, and the overall cost of borrowing before making a decision. Comparing loan offers from different lenders can help borrowers secure the best terms and ensure a smooth repayment experience.