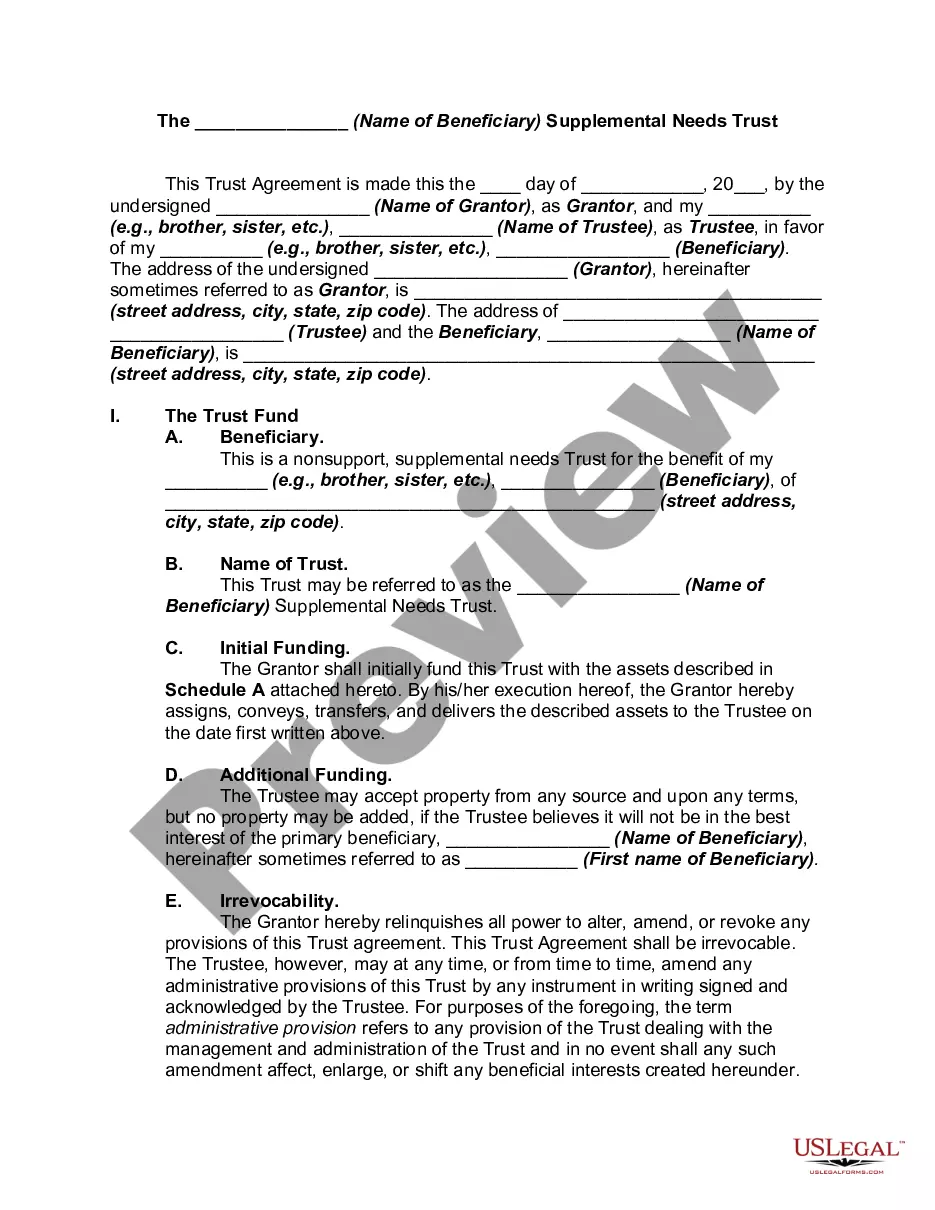

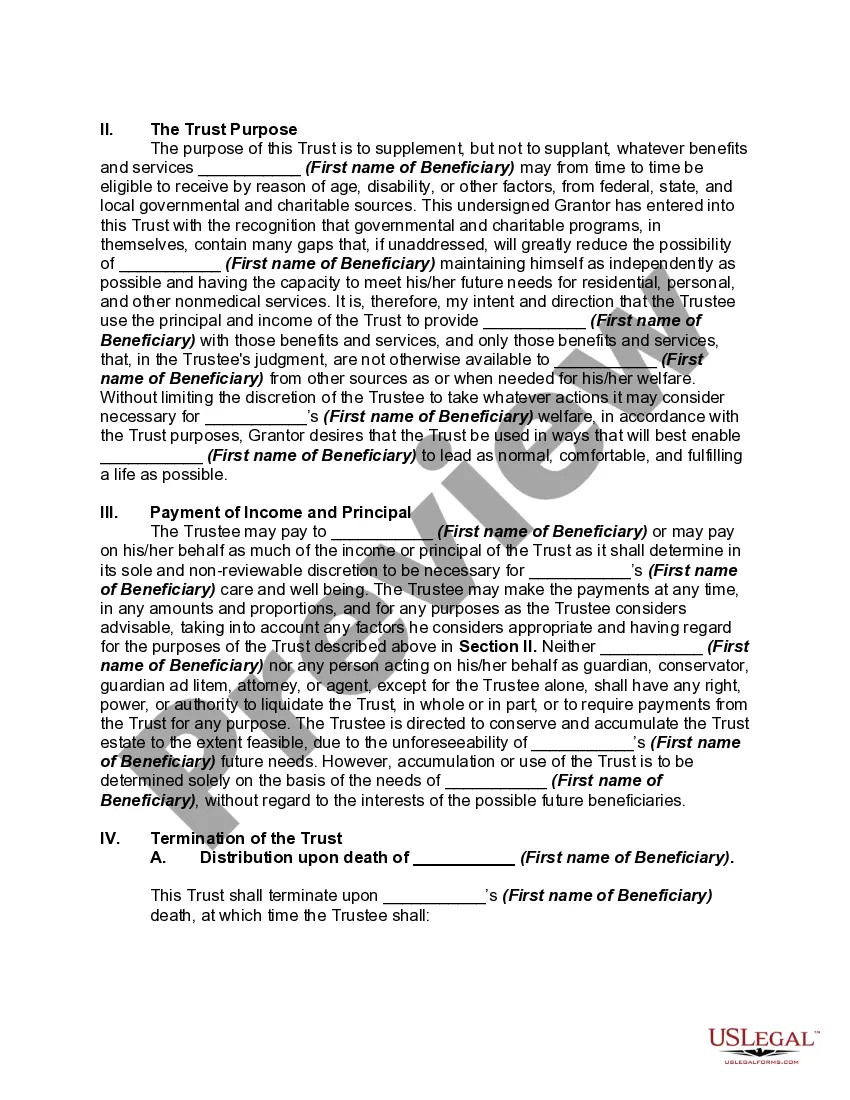

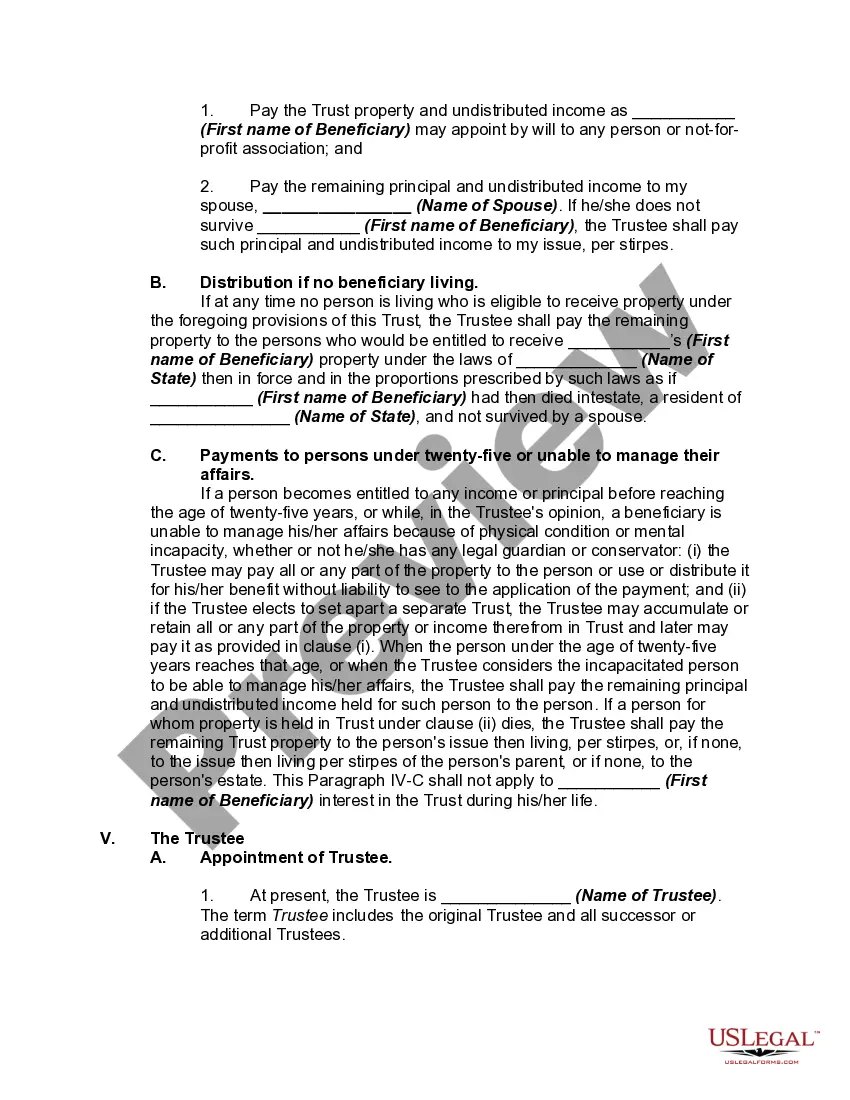

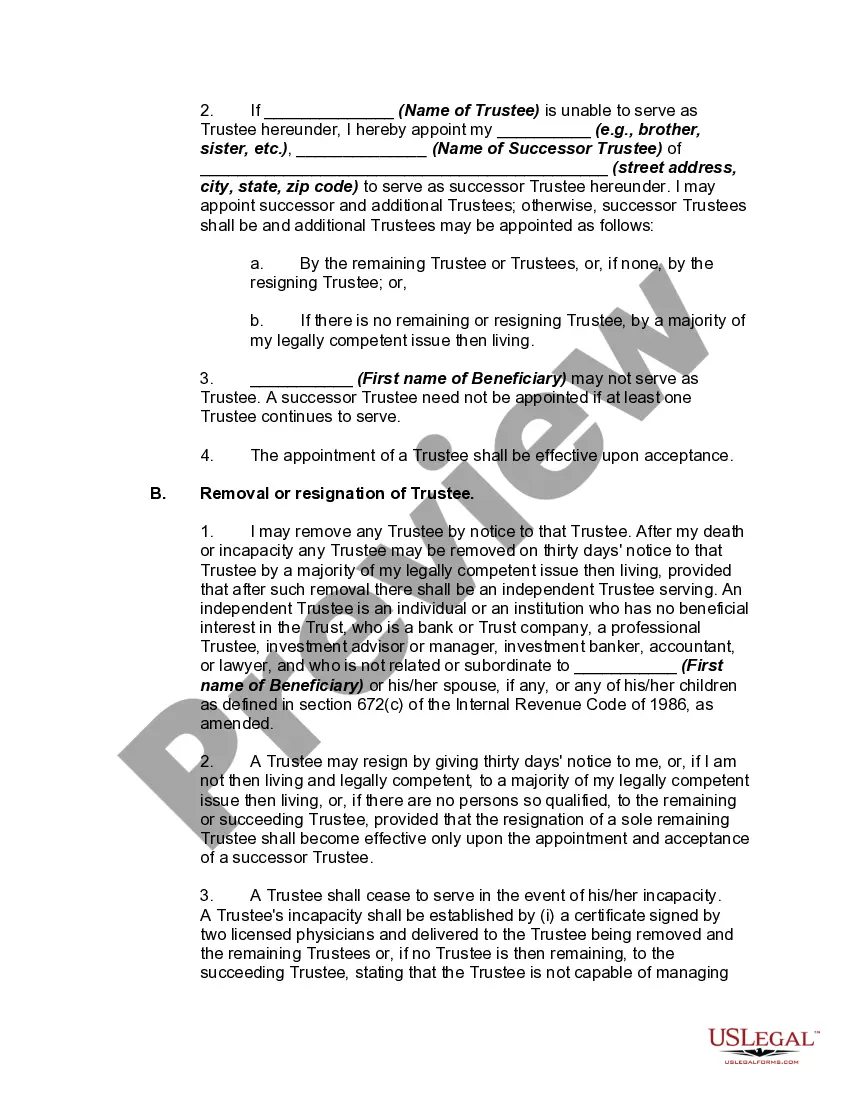

This form is a trust used to provide supplemental support for a disabled beneficiary without loss of government benefits. It may be revocable or irrevocable, as the funds are contributed by a third party, and not the beneficiary. The Omnibus Budget Reconciliation Act of 1993 established the supplemental needs trusts.

Title: Understanding Trust Funds for Disabilities: Types and Detailed Explanations Introduction: Trust funds for disability are crucial financial tools that aim to safeguard the long-term financial well-being of individuals with disabilities. These specialized funds are designed to manage and protect the assets on behalf of individuals with disabilities, ensuring they receive consistent support, even after the death of a parent or guardian. In this article, we will delve into the details of trust funds for disabilities, explain their purpose, and highlight the different types available. 1. Special Needs Trust (SET): A Special Needs Trust, also known as a Supplemental Needs Trust, is a common type of trust fund for disability. It allows individuals with disabilities to maintain their eligibility for government benefits such as Medicaid, while still benefiting from the funds and assets held within the trust. The SET is generally managed by a trustee, who can use the funds to provide extra assistance for various expenses not covered by public benefits. 2. Pooled Trusts: Pooled Trusts are collective trust funds designed for individuals with disabilities who do not have a parent, guardian, or grandparent to create a trust for them. These trusts pool funds from various sources and manage them collectively, making it an excellent option for those with limited assets or resources. Each beneficiary has a separate account, and a professional trustee oversees the management and distribution of funds. 3. Third-Party Trusts: Third-Party Trusts, also known as Family Trusts, are established by family members or friends to benefit an individual with a disability. The trust assets can be used to provide additional financial support without affecting the beneficiary's eligibility for government assistance programs. Inheritance, life insurance proceeds, or direct contributions from family members can fund third-party trusts. 4. Self-Settled or First-Party Trusts: Self-Settled Trusts, often referred to as "payback trusts," are typically funded with the assets owned by an individual with a disability. These trusts are primarily used when a person with a disability receives a settlement, inheritance, or accumulation of assets directly and wants to preserve their eligibility for public benefits. Upon the beneficiary's death, any remaining funds are typically used to reimburse the state for Medicaid benefits received during their lifetime. Benefits and Key Considerations: — Trust funds for disability provide financial security, ensuring a lifetime of care and support for individuals with disabilities. — They safeguard eligibility for governmental programs while allowing beneficiaries to access additional resources. — Trust funds can cover various expenses, including housing, education, transportation, therapies, travel, and more. — Proper estate planning and establishing a trust early can protect assets and avoid potential legal issues in the future. — Appointing a trustee is essential to ensure responsible management and adherence to the trust's terms. In conclusion, trust funds for disability play a critical role in providing financial stability and support for individuals with disabilities. Understanding the different types of trust funds available, including Special Needs Trusts, Pooled Trusts, Third-Party Trusts, and Self-Settled Trusts, empowers families to plan ahead and secure the future for their loved ones. Seeking professional guidance from an attorney or financial advisor experienced in disability planning is highly recommended ensuring the best outcomes for the beneficiaries.