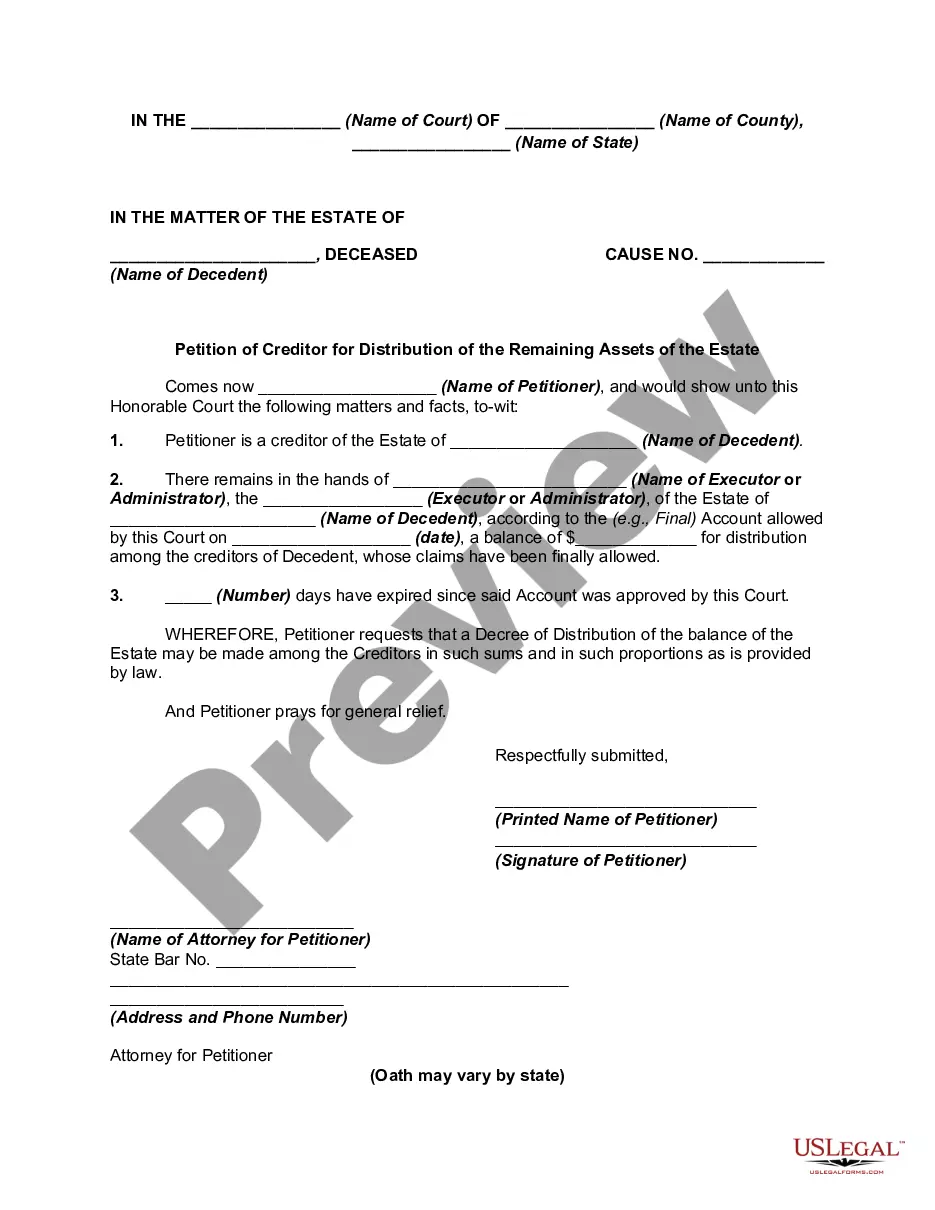

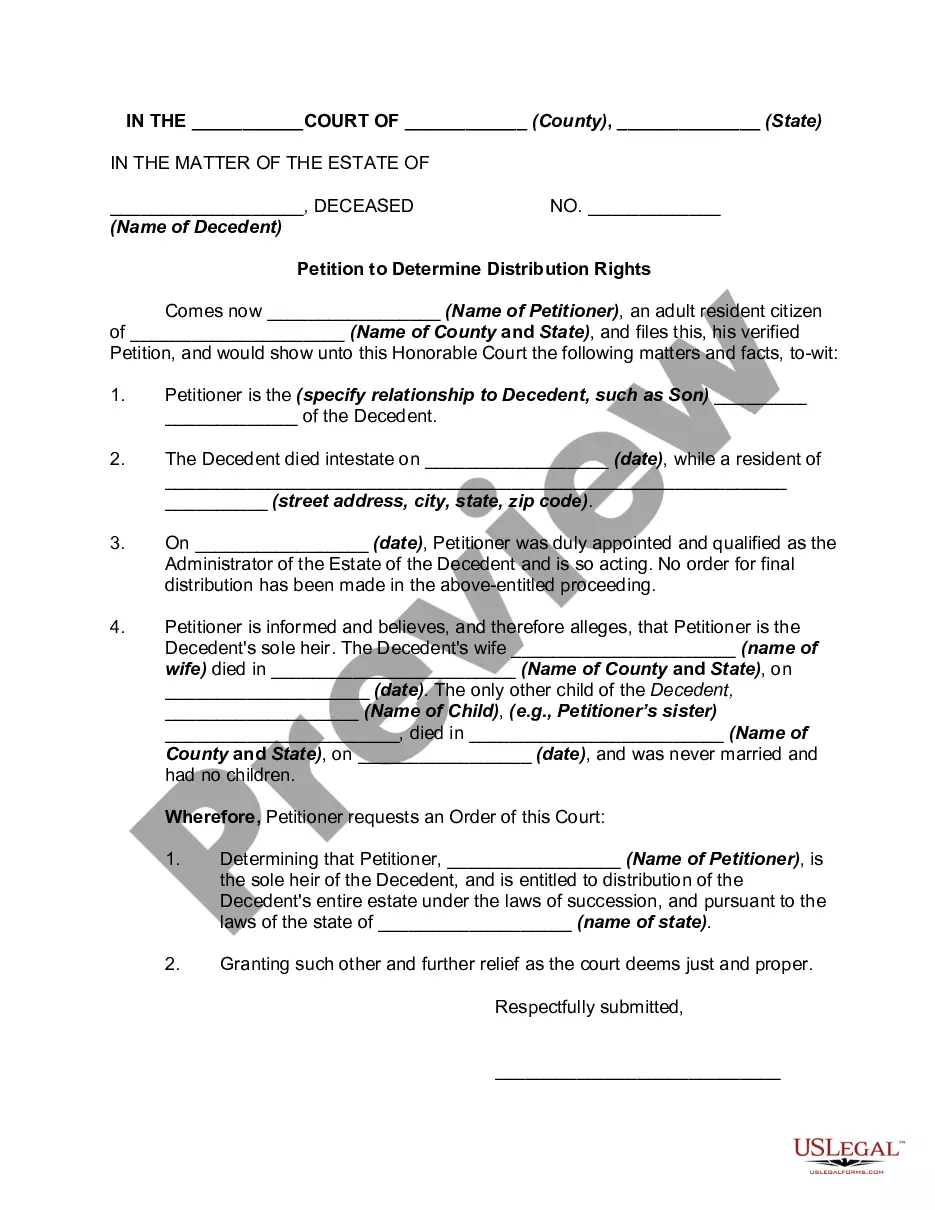

Estate Distribution Account With Irs

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Petition For Partial And Early Distribution Of Estate?

Locating a reliable resource to acquire the latest and most pertinent legal templates is a significant part of managing administrative tasks.

Selecting the appropriate legal documents demands precision and careful consideration, which is why it's essential to obtain Estate Distribution Account With Irs samples solely from reputable providers, such as US Legal Forms. An incorrect form can squander your time and prolong your situation.

Once you have the document on your device, you can edit it with the editor or print it out to complete it manually. Eliminate the complications that come with your legal documentation. Browse through the comprehensive US Legal Forms library to locate legal samples, assess their applicability to your situation, and download them instantly.

- Utilize the library navigation or search feature to locate your template.

- Examine the form's description to determine if it aligns with the regulations of your state and county.

- Check the form preview, if available, to confirm the template is of interest to you.

- Return to the search if the Estate Distribution Account With Irs does not fulfill your requirements.

- If you are confident about the form's suitability, proceed to download it.

- If you are a registered user, click Log in to verify your identity and access your chosen documents in My documents.

- If you lack an account, click Buy now to acquire the template.

- Select the payment plan that meets your preferences.

- Continue to the registration process to complete your transaction.

- Finalize your purchase by selecting a payment option (credit card or PayPal).

- Choose the document format for downloading the Estate Distribution Account With Irs.

Form popularity

FAQ

Yes, all estates are required to obtain a Tax ID number, also known as an ?employer id number? or EIN if they generate more than $600 in annual gross revenue. Since an estate and the decedent are separate taxable entities, a tax ID is required to file IRS form 1041.

More In Forms and Instructions The fiduciary of a domestic decedent's estate, trust, or bankruptcy estate files Form 1041 to report: The income, deductions, gains, losses, etc. of the estate or trust. The income that is either accumulated or held for future distribution or distributed currently to the beneficiaries.

Report income distributions to beneficiaries and to the IRS on Schedule K-1 (Form 1041). For calendar year estates and trusts, file Form 1041 and Schedule(s) K-1 on or before April 15 of the following year.

Once the executor of the estate has divided up the assets and distributed them to the beneficiaries, the inheritance tax can come into play. The amount of tax is calculated separately for each individual beneficiary, and the beneficiary has to pay the tax.

Form 1099-DIV is used by banks and other financial institutions to report dividends and other distributions to taxpayers and to the IRS.