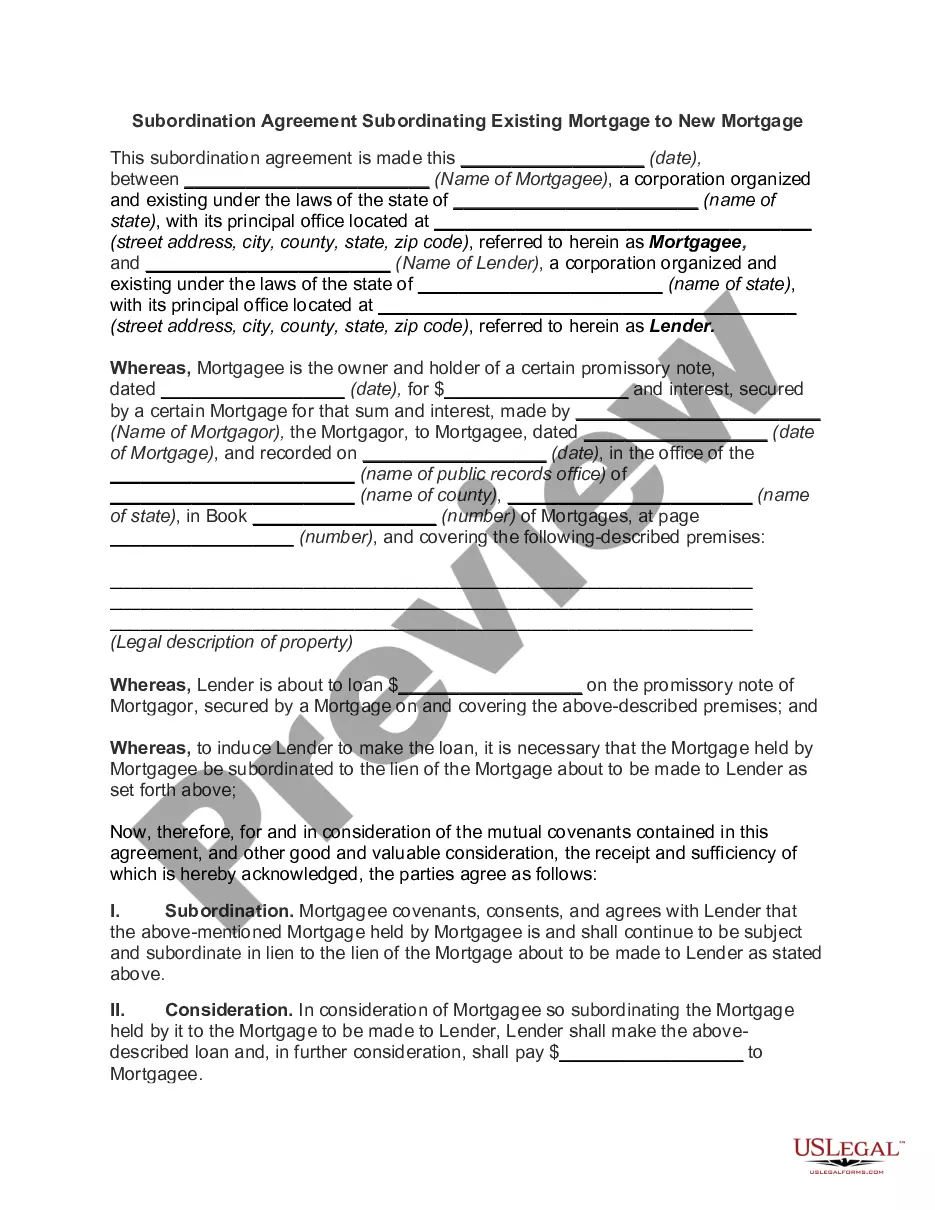

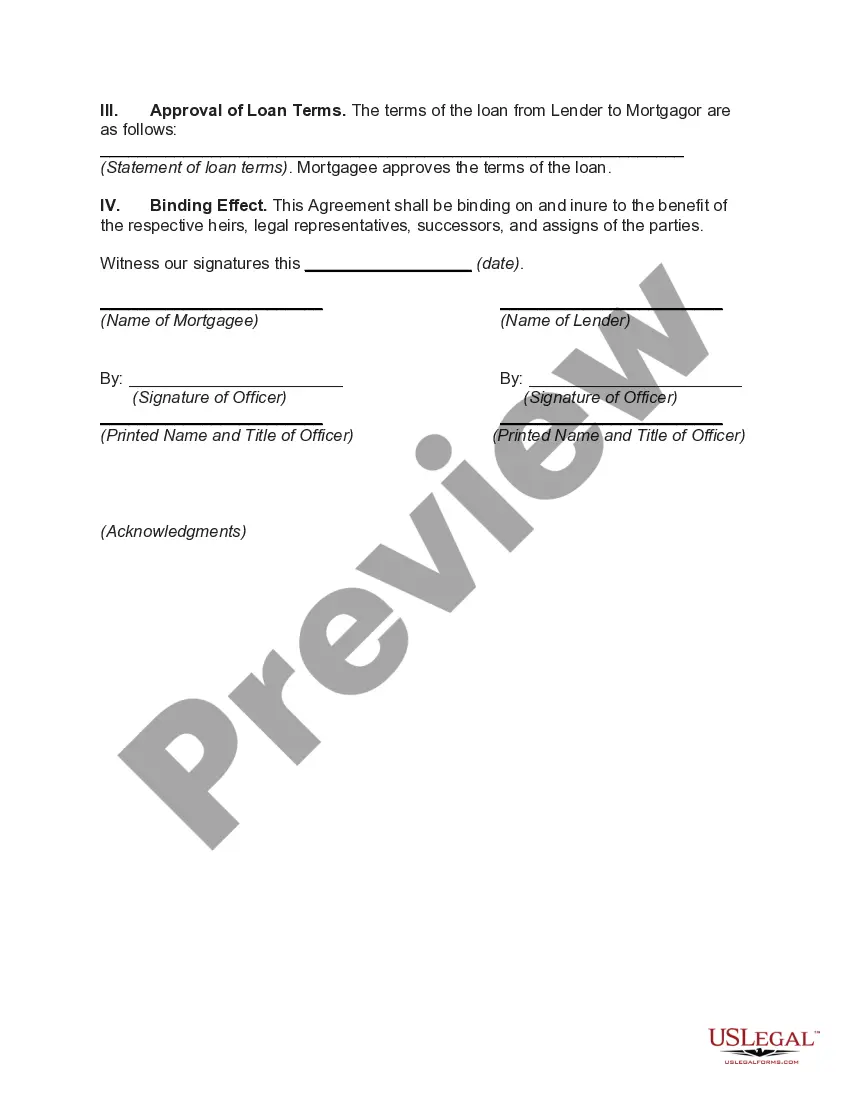

Subordination Of Mortgage Agreement

Description

How to fill out Subordination Of Mortgage Agreement?

Individuals frequently link legal documentation with intricate matters that only an expert can handle.

In some respects, this is accurate, as creating a Subordination Of Mortgage Agreement requires a significant grasp of subject matter norms, including state and local statutes.

Nonetheless, with US Legal Forms, everything has become more available: pre-prepared legal templates for any personal and business event tailored to state regulations are aggregated in a singular online directory and are now accessible to everyone.

All templates in our catalog are reusable: once obtained, they are kept in your profile. You can access them whenever necessary through the My documents tab. Explore all the benefits of utilizing the US Legal Forms platform. Subscribe today!

- Examine the content of the page carefully to ensure it aligns with your requirements.

- Review the form description or examine it through the Preview feature.

- If the previous option does not meet your needs, search for another sample using the Search field at the top.

- Select Buy Now once you identify the appropriate Subordination Of Mortgage Agreement.

- Choose the subscription plan that matches your needs and financial situation.

- Create an account or Log In to move to the payment section.

- Complete your subscription payment using PayPal or a credit card.

- Select your desired file format and click Download.

- Print your document or upload it to an online editor for faster completion.

Form popularity

FAQ

Purpose of a Subordination Agreement A subordination agreement is generally used when there are two mortgages and the mortgagor needs to refinance the first mortgage. It acknowledges that one party's interest or claim is superior to another in case the borrower's assets need to be liquidated to repay debts.

To compensate an investor for the risk, subordinated debt has a higher interest rate than senior debt.

A subordination agreement is a legal document that establishes one debt as ranking behind another in priority for collecting repayment from a debtor. The priority of debts can become extremely important when a debtor defaults on payments or declares bankruptcy.

What Is Mortgage Subordination? Subordination itself is the act of placing something in a lower-ranking position. Mortgage subordination boils down to a ranking system on the liens secured by your home. A lien is a legal agreement that grants the lender a right to repossess the property if you default on the loan.

Subordination is the process of ranking home loans (mortgage, HELOC or home equity loan) by order of importance. When you have a home equity line of credit, for example, you actually have two loans your mortgage and HELOC. Both are secured by the collateral in your home at the same time.