Lifetime Benefits Trust With Customers

Description

Form popularity

FAQ

Yes, you can set up a trust fund by yourself, especially with the help of user-friendly services like US Legal Forms, which simplifies the process. However, it is essential to understand the legal requirements and implications involved in creating a lifetime benefits trust with customers. Doing proper research ensures that your trust meets your needs and adheres to state laws. Therefore, while DIY is doable, seeking legal advice may provide peace of mind.

While a spousal lifetime access trust (SLAT) can provide lifetime benefits trust with customers, it does come with some drawbacks. One key disadvantage is that assets placed in a SLAT are irrevocable, meaning you cannot easily withdraw them once you've transferred them. Additionally, both spouses must agree on the trust's terms, which can lead to complications if circumstances change. Finally, if not properly structured, a SLAT might have tax implications that could affect your overall financial strategy.

To fill out a trust fund, you first need to gather all necessary information about your assets, beneficiaries, and your intentions regarding the trust. Next, you can use a reliable platform like US Legal Forms to access templates and guidance tailored to lifetime benefits trust with customers. Follow the instructions to complete the forms carefully, ensuring all details are accurate. Finally, have the document reviewed by a professional if needed, then sign it in front of a notary.

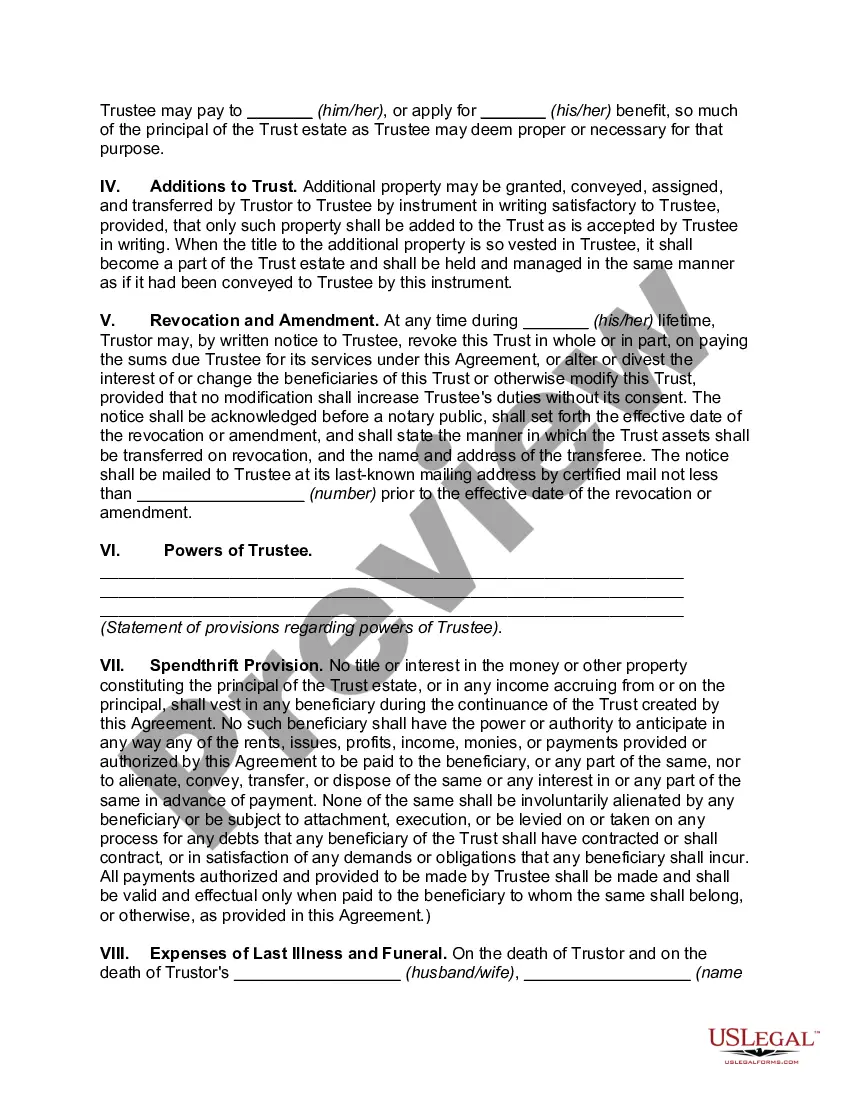

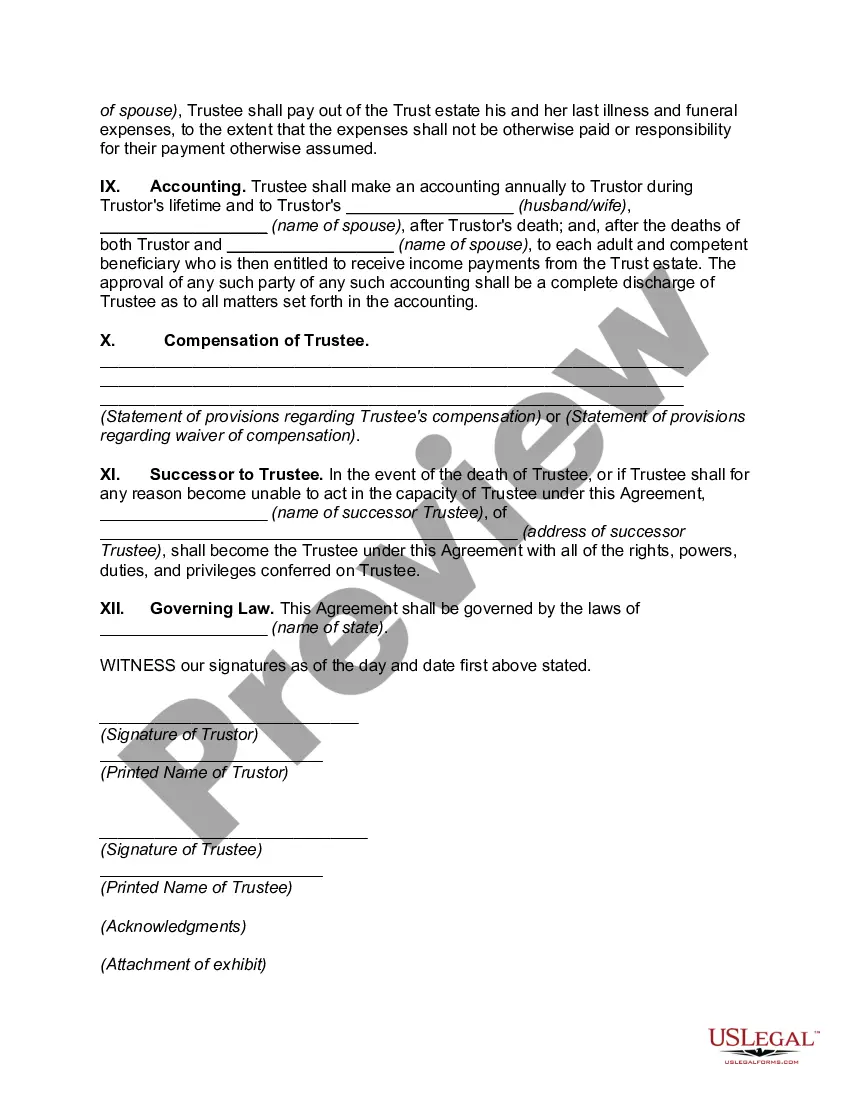

A lifetime benefits trust is designed to hold and manage your assets during your lifetime and can distribute them according to your wishes after your passing. Essentially, you place your assets in the trust, and a trustee handles them, ensuring they are used for your intended purposes. This structure provides financial security for you and your beneficiaries, giving you peace of mind. To understand the specifics of how a lifetime benefits trust works, our platform offers comprehensive resources tailored to guide you through the process efficiently.

At US Legal Forms, we build trust with our customers by prioritizing transparency and communication. We provide clear information about our lifetime benefits trust services, ensuring you understand the process every step of the way. Our customer testimonials showcase real experiences, reinforcing our commitment to satisfaction. Ultimately, we strive to create lasting relationships based on reliability and integrity, particularly when it comes to managing your lifetime benefits trust.

A lifetime beneficiary of a trust is someone who benefits from the trust's assets during their lifetime. The lifetime beneficiary receives income or distributions from the trust according to the terms set by the trust creator. This arrangement ensures that the benefits are provided for a person's life, offering financial security and support. By establishing a lifetime benefits trust with customers, you can tailor the trust to meet specific needs and goals for all involved parties.

Establishing trust with customers involves consistent communication, transparency, and delivering on promises. Building strong relationships creates loyalty and encourages customers to engage further. By leveraging tools like a lifetime benefits trust with customers, businesses can enhance their credibility and ensure lasting partnerships.

The primary purpose of a lifetime trust is to manage and protect assets for beneficiaries during the grantor's lifetime. This type of trust can provide financial support while maintaining control over how and when assets are distributed. When creating a lifetime benefits trust with customers, it is essential to consider how it aligns with your overall financial goals.

Lifetime trusts can have disadvantages, including limited flexibility in changing terms or beneficiaries once established. Additionally, some types of trusts may be subject to higher taxes or fees. Understanding these factors is critical when forming a lifetime benefits trust with customers, which US Legal Forms can help clarify and manage efficiently.

Deciding whether to gift a house or place it in a trust depends on individual circumstances and goals. Gifting may expose the house to tax implications, while placing it in a trust can help protect it and manage its distribution. Consulting professionals can guide you in establishing a lifetime benefits trust with customers, ensuring you make the right choice for your situation.