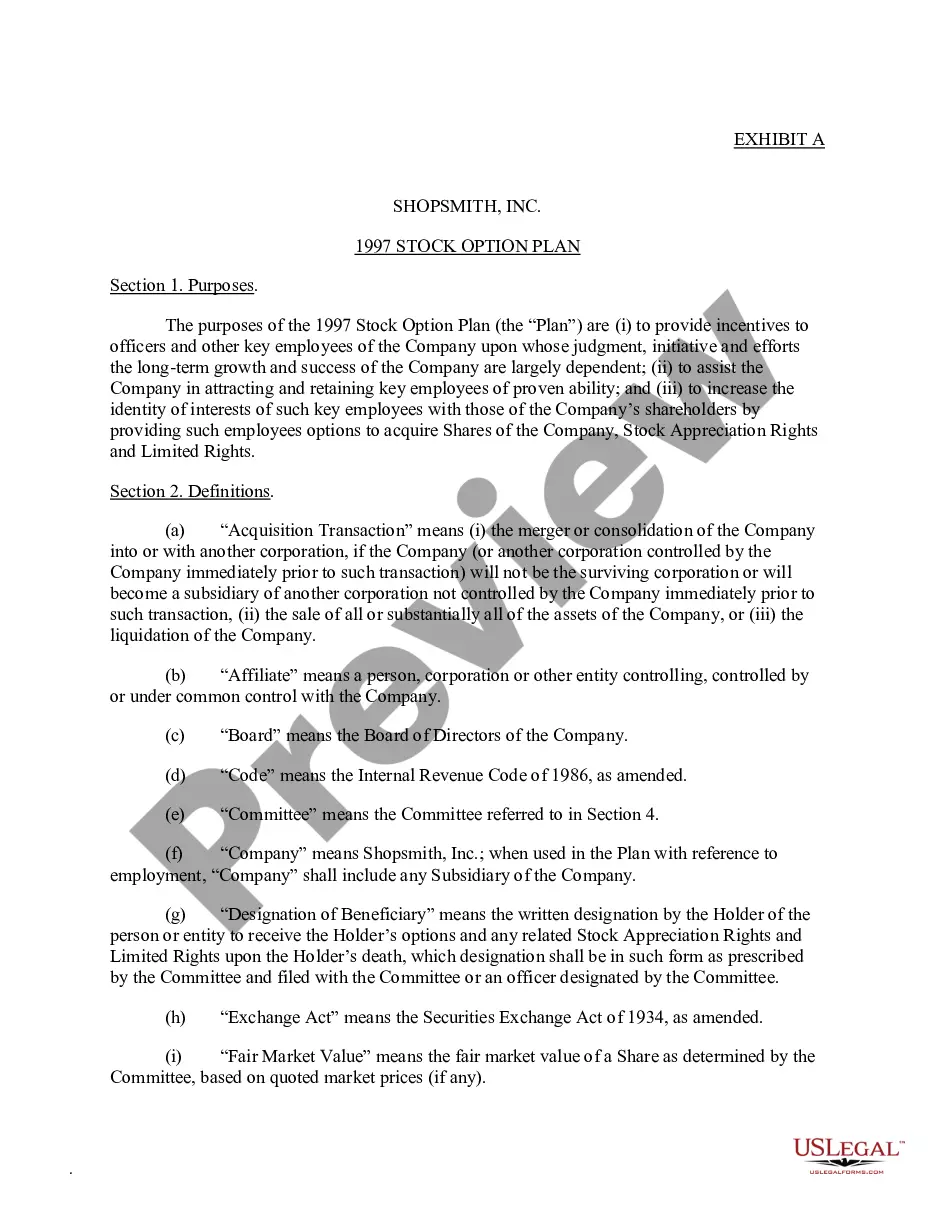

18-217D 18-217D . . . Stock Option Plan which provides for grant of Incentive Stock Options, (b) Non-qualified Stock Options (c) Stock Appreciation Rights, and (d) Limited Rights (which become exercisable upon (i) expiration of a tender offer, (ii) approval by stockholders of an Acquisition Transaction (as defined), (iii) date on which corporation is provided a copy of a Schedule 13D indicating that any person or group has become the holder of 25% or more of the outstanding shares of the corporation, or (iv) a change in composition of the Board of Directors such that individuals who served on the Board one year prior to such change no longer constitute a majority of the directors

Grant Exercise Stock For Employee

Category:

State:

Multi-State

Control #:

US-CC-18-217D

Format:

Word;

Rich Text

Instant download

Description

Free preview

Form popularity

FAQ

To report a stock option exercise, you will typically need to fill out the appropriate tax forms, noting the gain from the exercise. This gain is often subject to income tax, so it's crucial to keep accurate records. You may also want to consult with a tax professional for guidance. Remember, understanding how to grant exercise stock for employee purposes can simplify this reporting process.

Yes, you can grant exercise stock for employee stock options without the need to raise capital from an investor. Many companies choose to provide equity compensation as a way to attract and retain talent, and it does not always involve external funding. By leveraging your existing resources and utilizing platforms like US Legal Forms, you can efficiently set up stock option plans. This allows you to incentivize your employees while maintaining financial flexibility.

The $100,000 rule for stock options refers to a limit placed on the amount of incentive stock options (ISOs) that can be exercised in a calendar year. If an employee exceeds this limit, the excess options are typically treated as non-qualified stock options (NSOs). Understanding this rule is crucial when planning to grant exercise stock for employee options to ensure compliance and effective tax planning.

To give stock options to employees, first evaluate your company's goals and the desired outcomes of your equity compensation strategy. Then, prepare the necessary legal documents, specifying the option details and any restrictions. Finally, hold discussions with employees to explain how they can benefit from these options and ensure transparency regarding the process.

To grant stock options to employees, start by defining the terms and structure of your stock option plan. Consult legal and financial advisors to develop a plan that aligns with your company goals. Once the plan is established, communicate its benefits clearly to employees and ensure all considerations regarding taxes and ownership are managed effectively.

An employee stock grant plan is a program that allows employees to receive shares of the company’s stock as part of their compensation package. This plan often includes specific terms and conditions regarding vesting and eligibility, which can motivate and retain talent. By implementing such a plan, companies can grant exercise stock for employee equity, aligning employee interests with organizational success.

Yes, you can grant stock options to entities as well as individuals. In this context, an entity can include corporations, partnerships, or limited liability companies. However, when you grant exercise stock for employee options, you must ensure compliance with relevant regulations and company policies regarding ownership and taxation.