Debt Validation Letter With No Name

Description

How to fill out Letter Requesting A Collection Agency To Validate A Debt That You Allegedly Owe A Creditor?

Navigating through the red tape of official documents and forms can be challenging, particularly when one does not engage in such tasks professionally.

Even locating the correct template for a Debt Validation Letter With No Name can be laborious, as it needs to be authentic and accurate down to the last detail.

However, you will find significantly less time spent searching for an appropriate template from a resource you can rely on.

Acquire the appropriate form in just a few straightforward steps.

- US Legal Forms is a platform that streamlines the process of finding the right forms online.

- US Legal Forms is a single source you need to obtain the latest examples of documents, verify their use, and download these examples to complete them.

- It is a repository with over 85K forms that apply in multiple areas.

- When looking for a Debt Validation Letter With No Name, you can trust its reliability as all of the forms are verified.

- An account at US Legal Forms will ensure you have all the essential examples at your fingertips.

- Store them in your history or add them to the My documents collection.

- You have access to your saved forms from any device by clicking Log In at the library site.

- If you do not have an account yet, you can always search for the template you require.

Form popularity

FAQ

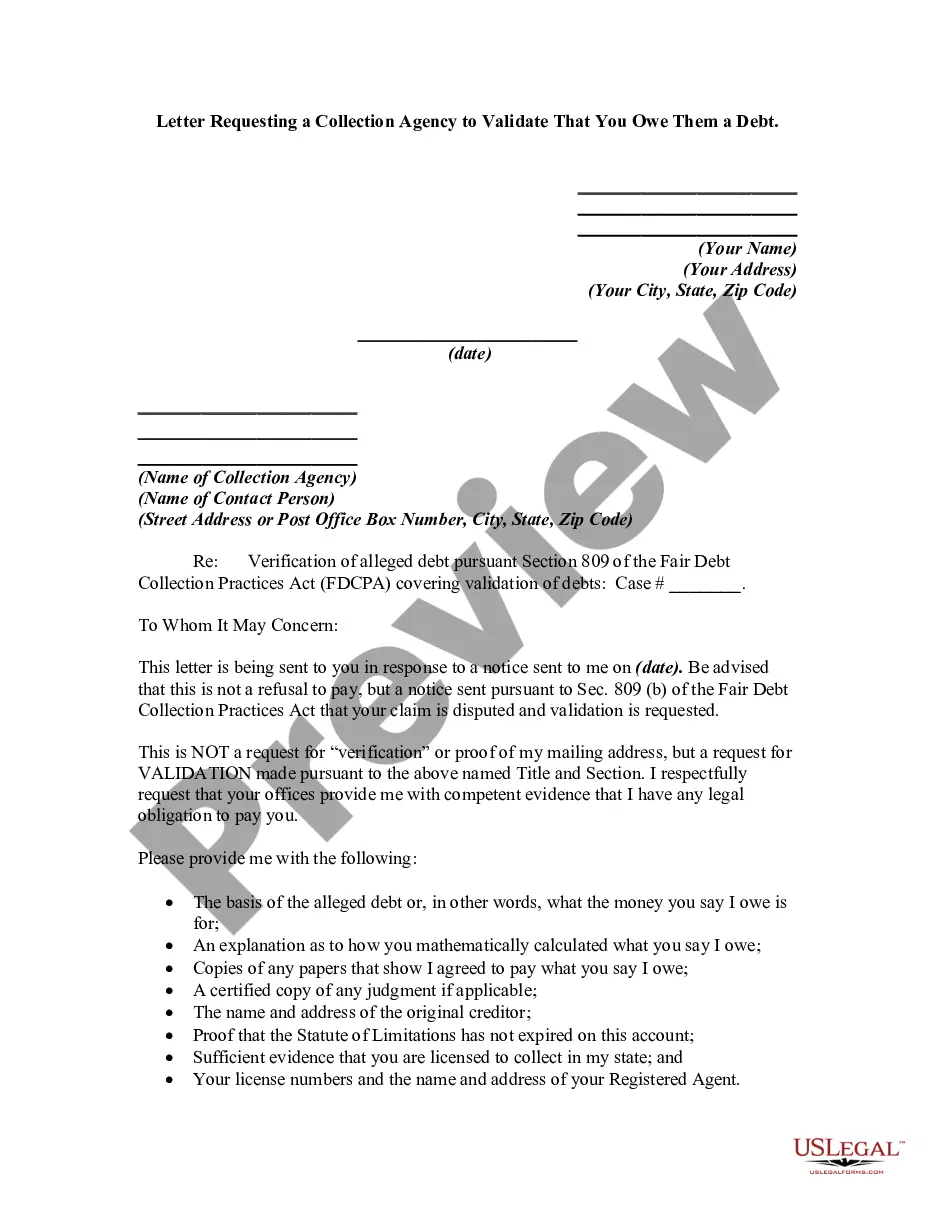

Yes, you can request a debt validation letter with no name if you receive notices about a debt you believe might not be valid. This request serves as a tool to verify the amount owed and the original creditor. Contacting the debt collector or creditor directly allows you to ask for this information. Using a platform like US Legal Forms simplifies the process of creating the necessary request.

To ask for a debt validation letter with no name, you should start by contacting the creditor or debt collector. Clearly state that you need a validation letter regarding the debt. You can send a written request via mail or email, ensuring to include any relevant account details. This formal request will help you confirm the legitimacy of the debt.

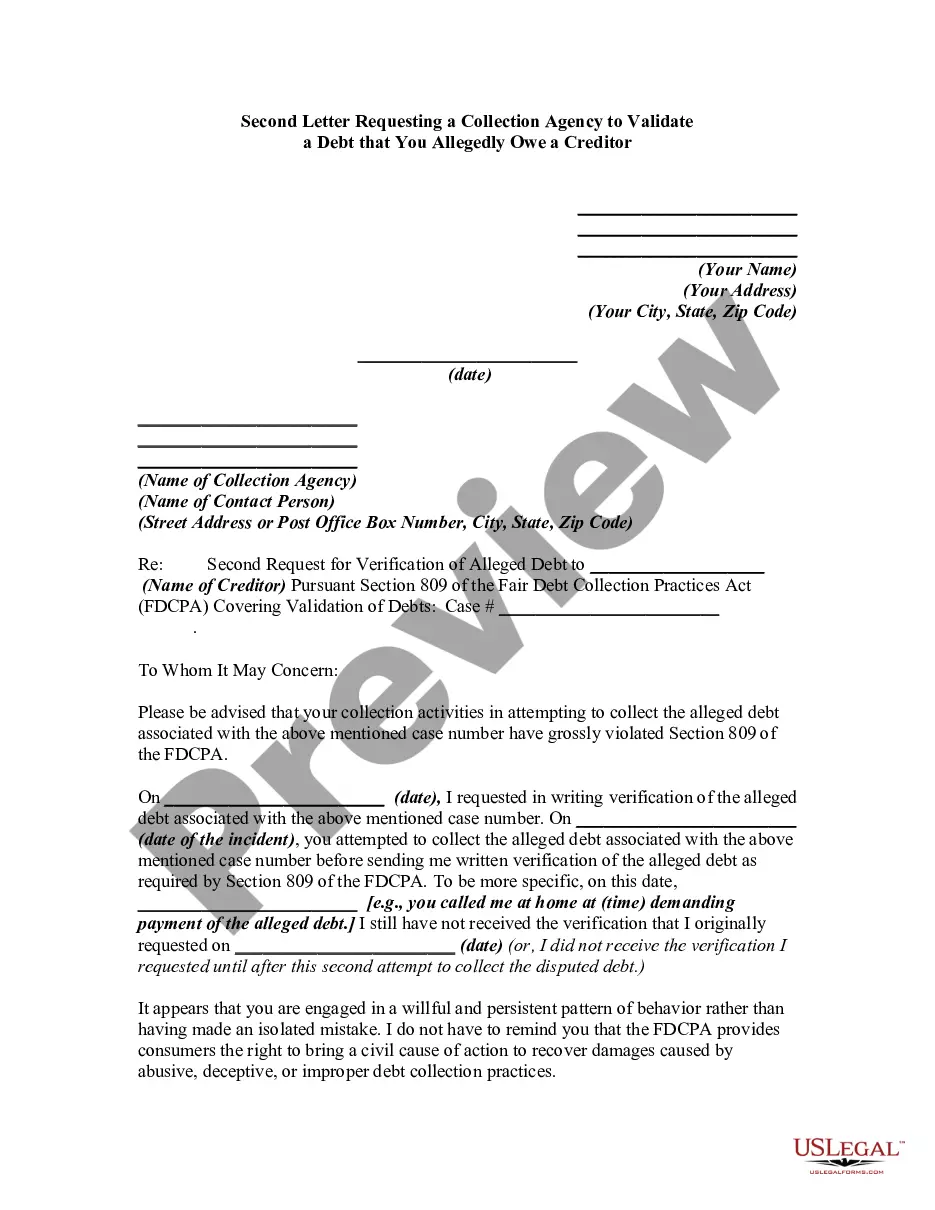

The 777 rule refers to a strategy that allows consumers to respond to debt collectors effectively. Under this rule, if you receive a debt validation letter with no name, you can respond within seven days, asserting your rights. This time frame can help you gather relevant evidence and prepare your case, ensuring that you're equipped to handle the conversation with the collector.

Proof of debt typically includes documentation that clearly outlines the borrowing agreement, payment history, and details about the creditor. A debt validation letter with no name may be a valuable tool in this regard, as it helps clarify roles and responsibilities. Additionally, financial statements or contracts can also serve as strong evidence of debt.

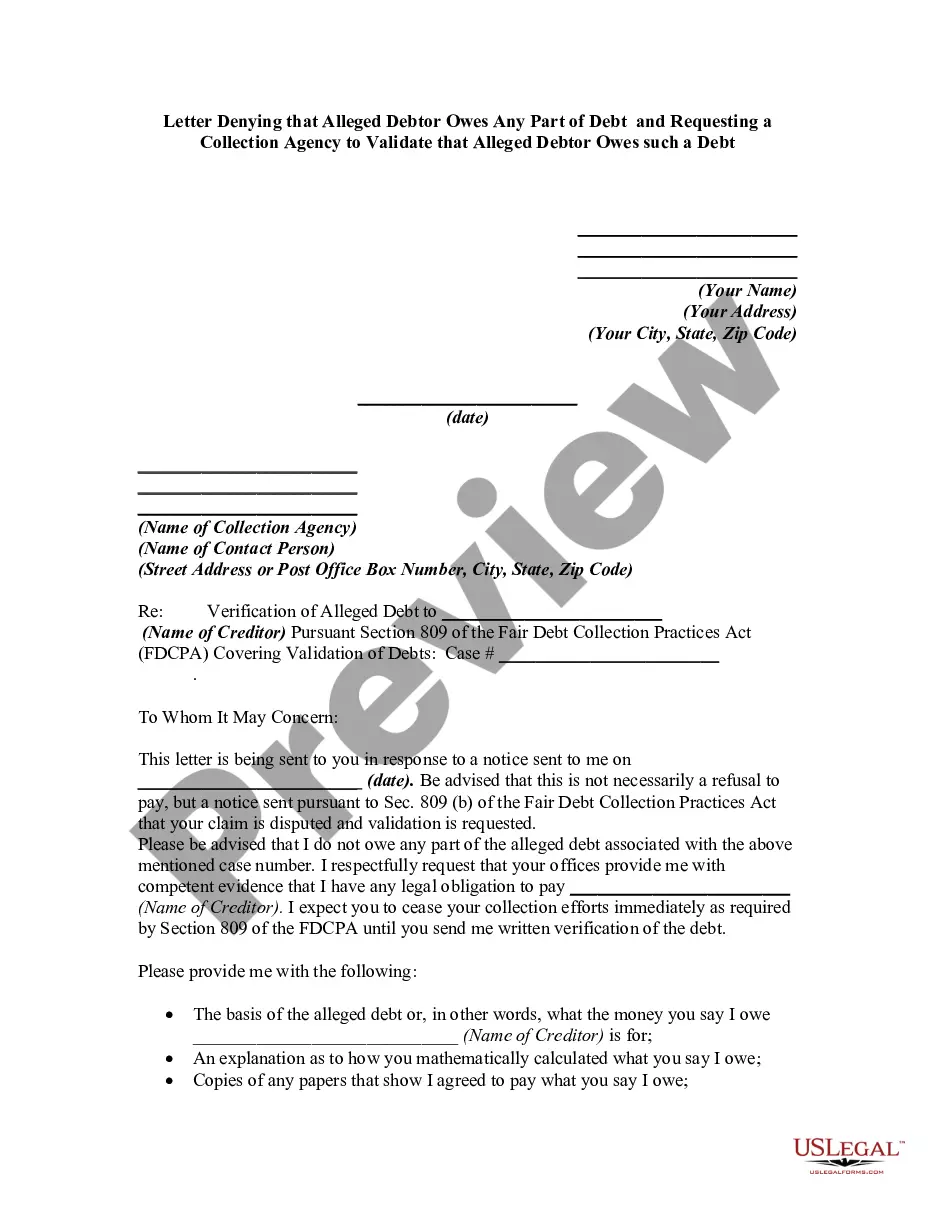

To prove a debt is not yours, request a debt validation letter with no name from the creditor or collection agency. This document should detail the original creditor and account information. Along with this, you can provide proof of your identity and financial history to demonstrate that the debts do not match your records.

Proving a debt isn't yours often involves gathering correspondence and documentation that indicates the debt belongs to someone else. You may consider obtaining a debt validation letter with no name, which can clarify your situation. Additionally, keep records of your financial transactions and communications to support your case.

To dispute a debt that isn't yours, start by requesting a debt validation letter with no name from the collector. This letter will provide details about the debt and the creditor. After obtaining this information, you can formally contest the debt by writing to the collector, clearly stating that you believe the debt is not yours and providing any evidence to support your claim.

Debt collectors need to prove that you owe the debt, that they have the right to collect it, and that they have provided proper validation. This includes showing documentation related to the debt and your agreement to it. If you receive a debt validation letter with no name, ask for detailed evidence to satisfy these three points.

To prove that a debt is not yours, gather documentation that supports your claim, such as payment records and account statements. You can also submit a debt validation letter with no name, making sure to highlight inconsistencies or discrepancies. It's crucial to communicate clearly with the creditor and maintain records of all correspondences.

Yes, debt validation letters can be effective in disputing debts that you believe are inaccurate or illegitimate. By formally requesting validation, you compel the creditor to provide proof of the debt's validity and its details. However, a debt validation letter with no name may require extra diligence on your part to ensure the information aligns with your records.