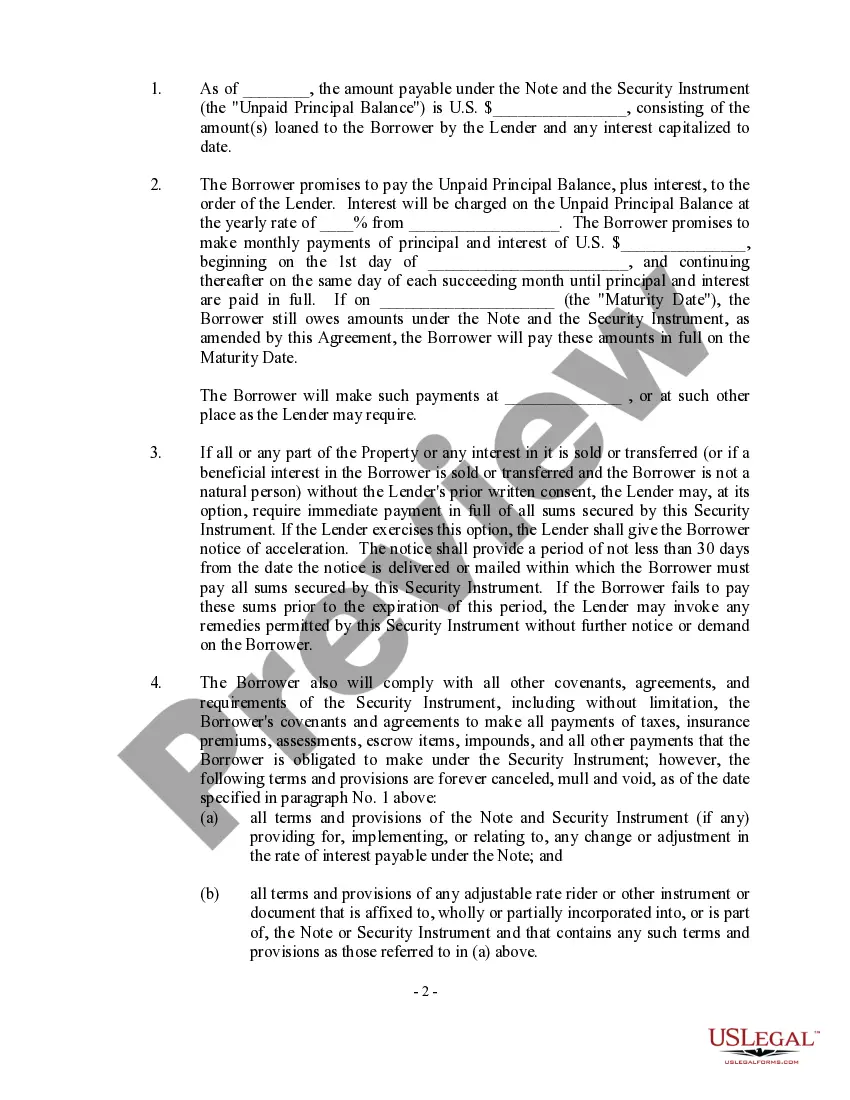

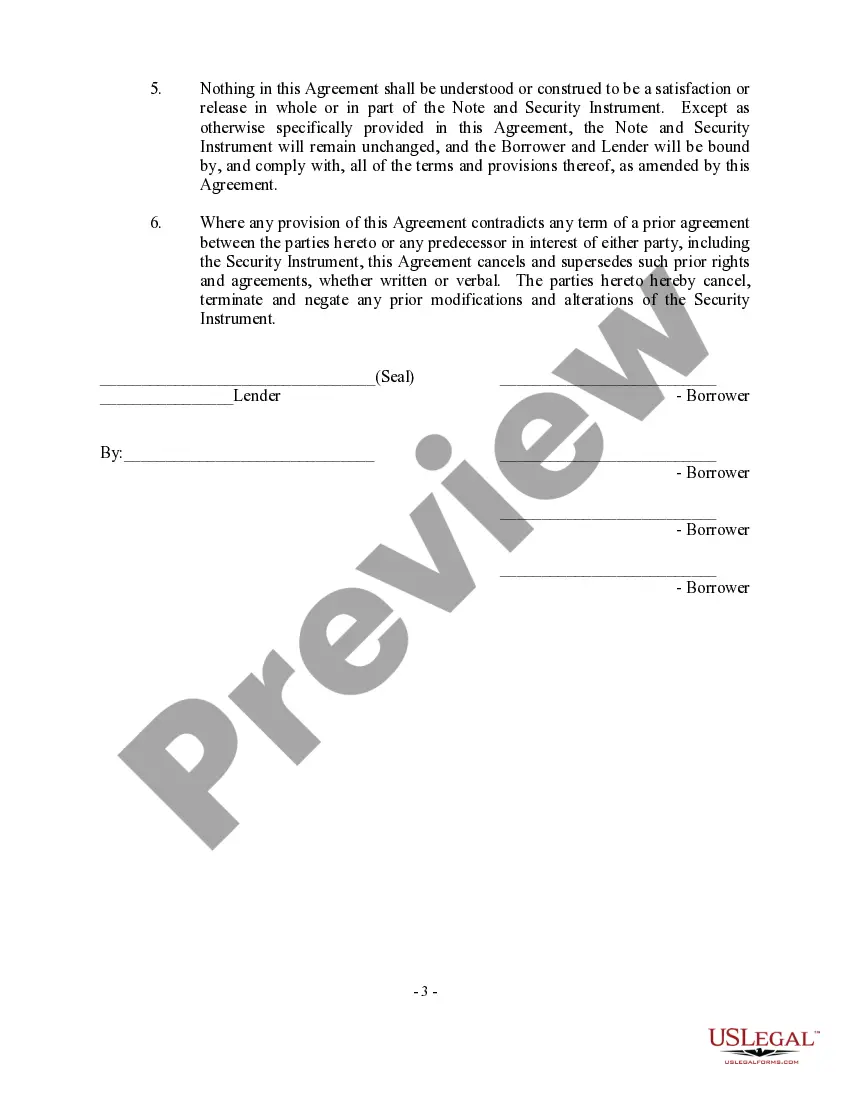

Loan modification for HELOT stands for "Home Equity Line of Credit" modification, which is a process that aims to modify the terms and conditions of the existing HELOT loan agreement. This modification is typically sought by homeowners who are experiencing financial hardship and are unable to make their regular loan payments. Helots are revolving lines of credit that allow homeowners to borrow against the equity they have built up in their homes. These lines of credit are secured by the property itself, and the available credit limit is determined by the appraised value of the home and the outstanding mortgage balance. When homeowners face financial difficulties, they may struggle with their HELOT payments, leading to potential default or foreclosure. In such cases, a loan modification for HELOT can provide some relief by making the loan more affordable and manageable for the borrowers. The primary goal of loan modification is to prevent foreclosure and help homeowners maintain ownership of their homes. Loan modification for HELOT can involve several changes to the terms of the existing loan agreement, including: 1. Interest Rate Reduction: One option is to negotiate a lower interest rate on the outstanding balance, which can significantly reduce monthly payments and make the loan more affordable. 2. Loan Term Extension: Another modification possibility is to extend the repayment term, spreading out the existing debt over a longer period. This approach results in smaller monthly payments, enabling homeowners to stay current on their obligations. 3. Principal Forbearance: Sometimes, lenders may temporarily reduce or suspend a portion of the loan principal. This reduces the immediate burden on homeowners and provides some breathing room until the situation improves. 4. Conversion to Fixed-Rate Loan: In some cases, a modification can involve converting a variable-rate HELOT to a fixed-rate loan, providing borrowers with stability and predictability in their monthly payments. 5. Balloon Payment Deferral: If the HELOT has a large balloon payment due at the end of the term, a modification may allow for the deferral of this payment until a later date or its integration into the modified monthly payments. 6. Waiving of Fees and Penalties: To ease the financial burden, lenders may consider waiving or reducing late payment fees, prepayment penalties, or other charges associated with the HELOT. It's important to note that the eligibility and availability of these loan modification options for HELOT may vary depending on the specific circumstances, the policies of the lender, and the borrower's ability to demonstrate financial hardship. In conclusion, loan modification for HELOT is a viable solution for homeowners facing financial difficulties and offers various options to make the loan more manageable. This process aims to prevent foreclosure, provide relief, and help homeowners regain financial stability.

Loan Modification For Heloc

Description

How to fill out Loan Modification For Heloc?

Creating legal documents from the ground up can frequently be daunting.

Certain situations may require extensive research and significant financial investment.

If you’re looking for a simpler and more budget-friendly method of preparing Loan Modification For Heloc or other forms without unnecessary complications, US Legal Forms is always accessible to you.

Our online repository of more than 85,000 current legal forms encompasses nearly every aspect of your financial, legal, and personal needs. With just a few clicks, you can promptly acquire state- and county-specific templates meticulously prepared by our legal experts.

Review the form previews and descriptions to ensure you have located the document you need. Confirm that the template you select adheres to the criteria of your state and county. Choose the most appropriate subscription option to obtain the Loan Modification For Heloc. Download the form, then complete, sign, and print it. US Legal Forms has an immaculate reputation backed by over 25 years of experience. Join us today and make document execution simple and efficient!

- Utilize our website whenever you require reliable services to swiftly find and download the Loan Modification For Heloc.

- If you’re already familiar with our services and have set up an account with us previously, simply Log In to your account, locate the template, and download it or re-download it anytime from the My documents section.

- Don’t have an account? No problem. Registration takes just a few minutes and allows you to browse the catalog.

- But before proceeding to download Loan Modification For Heloc, remember to follow these guidelines.

Form popularity

FAQ

The Federal National Mortgage Association (FNMA), commonly known as Fannie Mae, is a United States government-sponsored enterprise (GSE) and, since 1968, a publicly traded company.

The National Mortgage Database (NMDB®) [1] program is jointly funded and managed by the Federal Housing Finance Agency (FHFA) and the Consumer Financial Protection Bureau (CFPB). This program is designed to provide a rich source of information about the U.S. mortgage market.

Mortgage Data is information about properties that are refinanced by banks and lending institutions. Banks, lenders, and real estate businesses use mortgage data to analyze the creditworthiness of an individual before granting them a mortgage.

The National Mortgage Database (NMDB) is the first component of the National Mortgage Database program. NMDB is updated quarterly for a nationally representative five percent sample of closed-end first-lien residential mortgages in the United States.

Government National Mortgage Association (Ginnie Mae) is a self-financing, wholly owned U.S. Government corporation within the Department of Housing and Urban Development. It is the primary financing mechanism for all government-insured or government-guaranteed mortgage loans.

Public Use Database - Fannie Mae and Freddie Mac The datasets supply mortgage lenders, planners, researchers, policymakers, and housing advocates with information concerning the flow of mortgage credit in America's neighborhoods.

A promissory note provides the financial details of the loan's repayment, such as the interest rate and method of payment. A mortgage specifies the procedure that will be followed if the borrower doesn't repay the loan. If you live in a deed of trust state, you will not get a mortgage note.

HMDA data are the most comprehensive source of publicly available information on the U.S. mortgage market. Learn more about mortgage activity from these data or download the data for your own analysis.