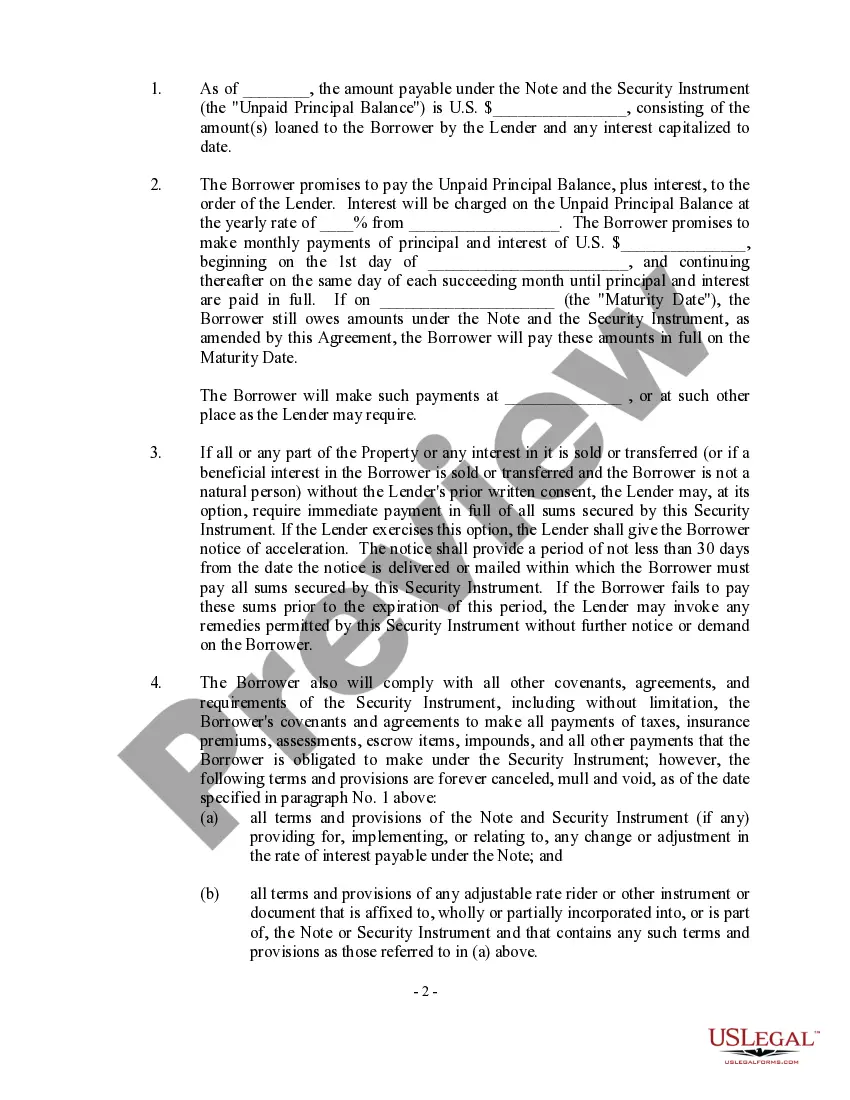

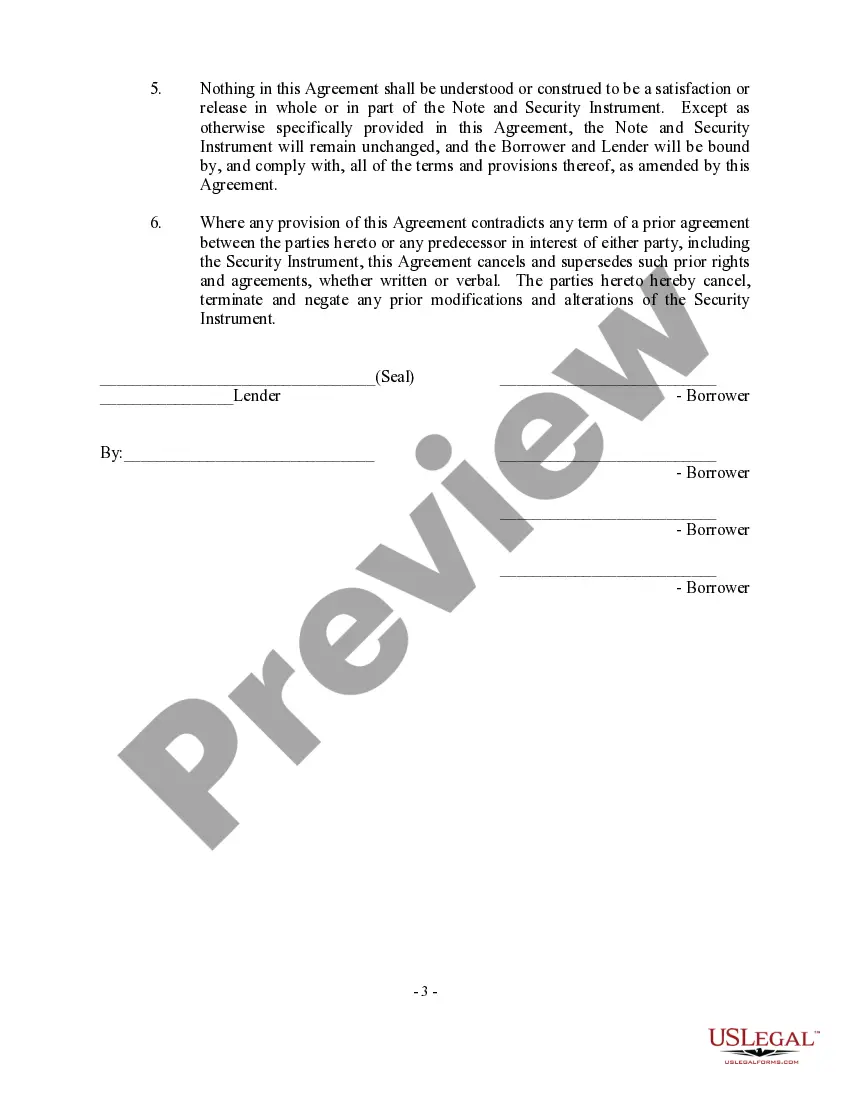

Loan modification form with balloon payment is a legal document that borrowers utilize to modify the terms of their existing loan, specifically regarding the repayment structure. This type of modification is often sought by individuals who wish to temporarily reduce their monthly mortgage payments, with the intention of making a larger, lump-sum payment (balloon payment) at the end of the modified loan term. One of the primary reasons borrowers opt for a loan modification form with balloon payment is to alleviate financial burdens during a specific time period, such as a job loss, career transition, or unforeseen medical expenses. By reducing the monthly payments, borrowers can better manage their finances while navigating through a challenging phase. Loan modification forms with balloon payments can vary slightly based on the borrower's specific needs and the lender's guidelines. Different types of loan modification forms with balloon payment include: 1. Temporary Interest-Only Modification: This type of modification allows borrowers to only pay the interest portion of their mortgage for a predefined period, typically ranging from 6 months to 2 years. At the end of this term, a balloon payment is required to settle the remaining principal balance. 2. Principle Reduction Modification: In this form of modification, borrowers negotiate with the lender to reduce the outstanding principal amount owed. This helps in lowering the monthly payments, but a balloon payment is still required to cover the reduced principal balance. 3. Graduated Payment Modification: This modification structure allows borrowers to gradually increase their monthly payments over a fixed timeframe. This approach allows borrowers with lower initial affordability to gradually adjust their budget until they reach a point where they can afford the full payment, which includes a balloon payment. It's crucial for borrowers considering a loan modification form with a balloon payment to thoroughly assess their financial situation and ensure they can make the necessary balloon payment when it becomes due. Failure to do so may result in foreclosure or other legal consequences. Consulting with a financial advisor or attorney specializing in loan modifications is always recommended to fully understand the implications and to ensure the best outcome for the borrower.

Loan Modification Form With Balloon Payment

Description

How to fill out Loan Modification Form With Balloon Payment?

Drafting legal paperwork from scratch can sometimes be intimidating. Certain scenarios might involve hours of research and hundreds of dollars invested. If you’re searching for a more straightforward and more cost-effective way of creating Loan Modification Form With Balloon Payment or any other forms without jumping through hoops, US Legal Forms is always at your disposal.

Our online catalog of more than 85,000 up-to-date legal forms covers almost every element of your financial, legal, and personal matters. With just a few clicks, you can quickly access state- and county-compliant templates carefully put together for you by our legal professionals.

Use our website whenever you need a trusted and reliable services through which you can quickly locate and download the Loan Modification Form With Balloon Payment. If you’re not new to our website and have previously set up an account with us, simply log in to your account, locate the template and download it away or re-download it anytime later in the My Forms tab.

Not registered yet? No worries. It takes minutes to set it up and navigate the library. But before jumping directly to downloading Loan Modification Form With Balloon Payment, follow these tips:

- Check the form preview and descriptions to make sure you are on the the form you are looking for.

- Make sure the template you choose complies with the requirements of your state and county.

- Pick the best-suited subscription option to get the Loan Modification Form With Balloon Payment.

- Download the file. Then complete, certify, and print it out.

US Legal Forms has a good reputation and over 25 years of experience. Join us now and transform form execution into something easy and streamlined!

Form popularity

FAQ

EForms | The #1 website for free legal forms and documents.

With Rocket Lawyer, you can ask a lawyer a question and access legal forms at no cost to you with its seven-day free trial. If you want help filing your LLC formation paperwork, or you need the company's services for longer than a week, you'll pay $39.99 per month.

You can write your own contracts. There is no requirement that they must be written by a lawyer. There is no requirement that they have to be a certain form or font. In fact, contracts can be written on the back of a napkin!

Legal Templates headquartered in Greensboro, North Carolina equips businesses with tools to be their own legal advocates, using technology to create free legal documents simply and quickly. At LegalTemplates.net users find the form they need, choose their state, and can then customize the requested document.

Our forms are available for FREE, as blank templates, without registering for an account or submitting billing information. Step 1 ? If you do not have a subscription and would like to download a free blank template, visit our Homepage (.eforms.com) to find your form, utilizing the ?Search? bar.

Will. A will is a legal document that designates who should receive your assets after death. ... Advanced Directive. ... Healthcare Power of Attorney. ... Durable Power of Attorney. ... Revocable Trust.

Important points to include in a legal document. Party details. List the names, numbers, addresses (email or physical), and any other relevant information of all parties involved. ... Background information. ... Motion. ... Roles and responsibilities. ... Breaches or contingencies. ... Dates and signatures.