Accounting For Convertible Preferred Stock

State:

Multi-State

Control #:

US-EG-9013

Format:

Word;

Rich Text

Instant download

Description Sample Stock Purchase Agreement

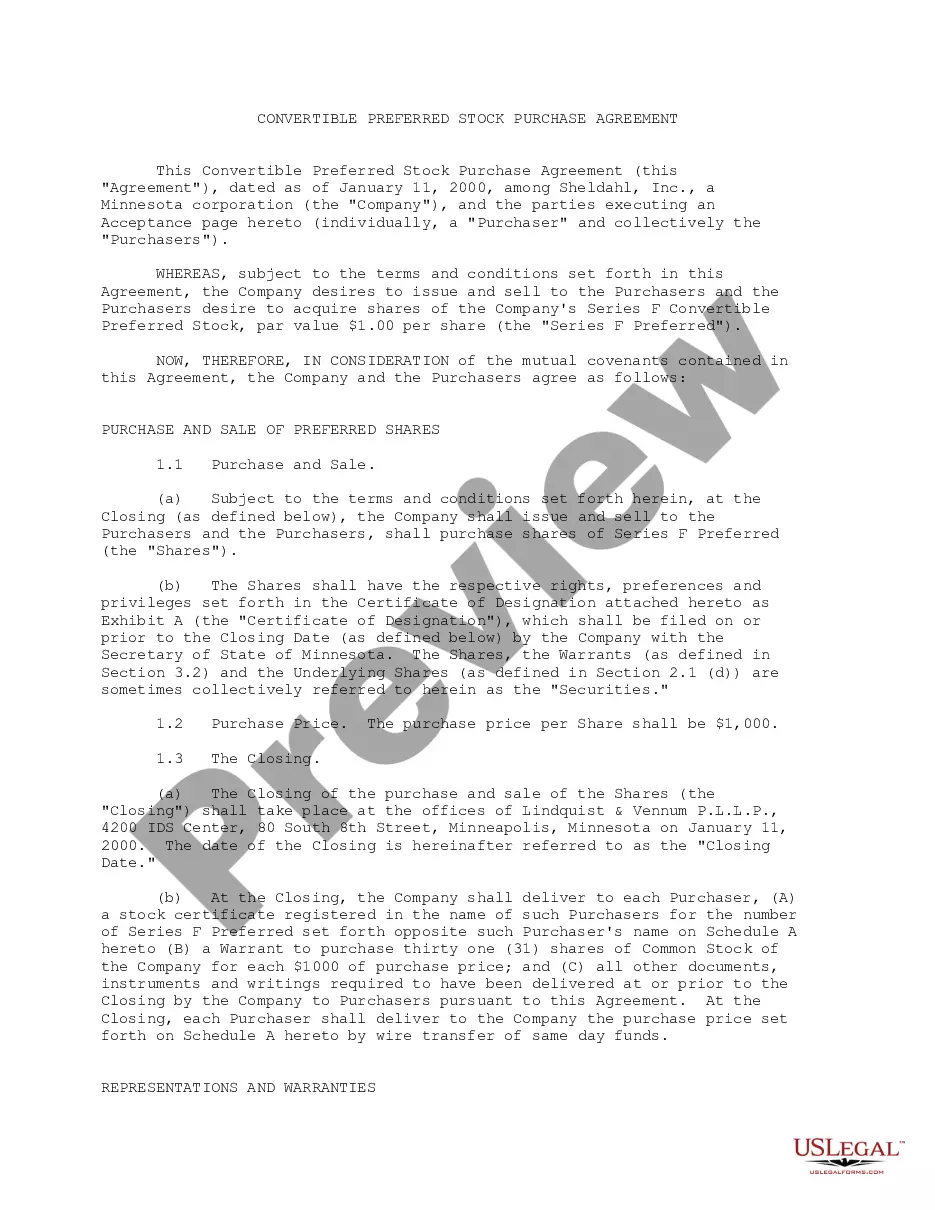

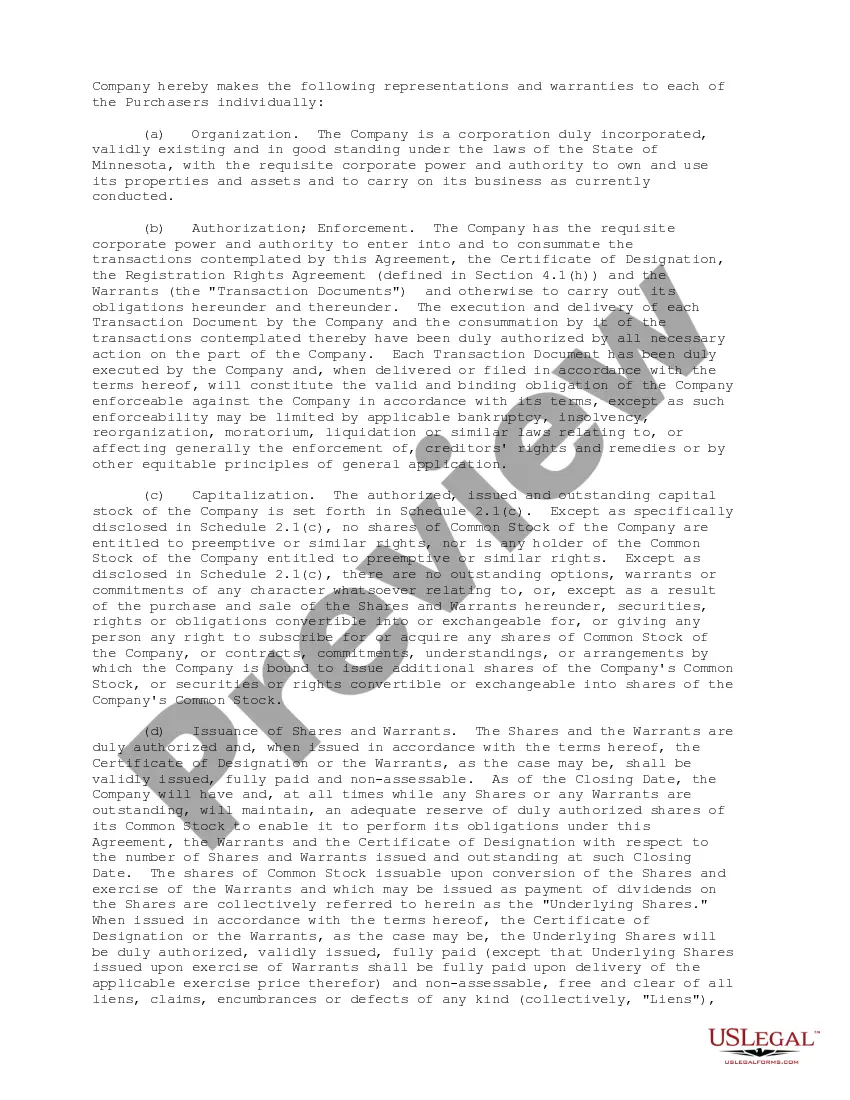

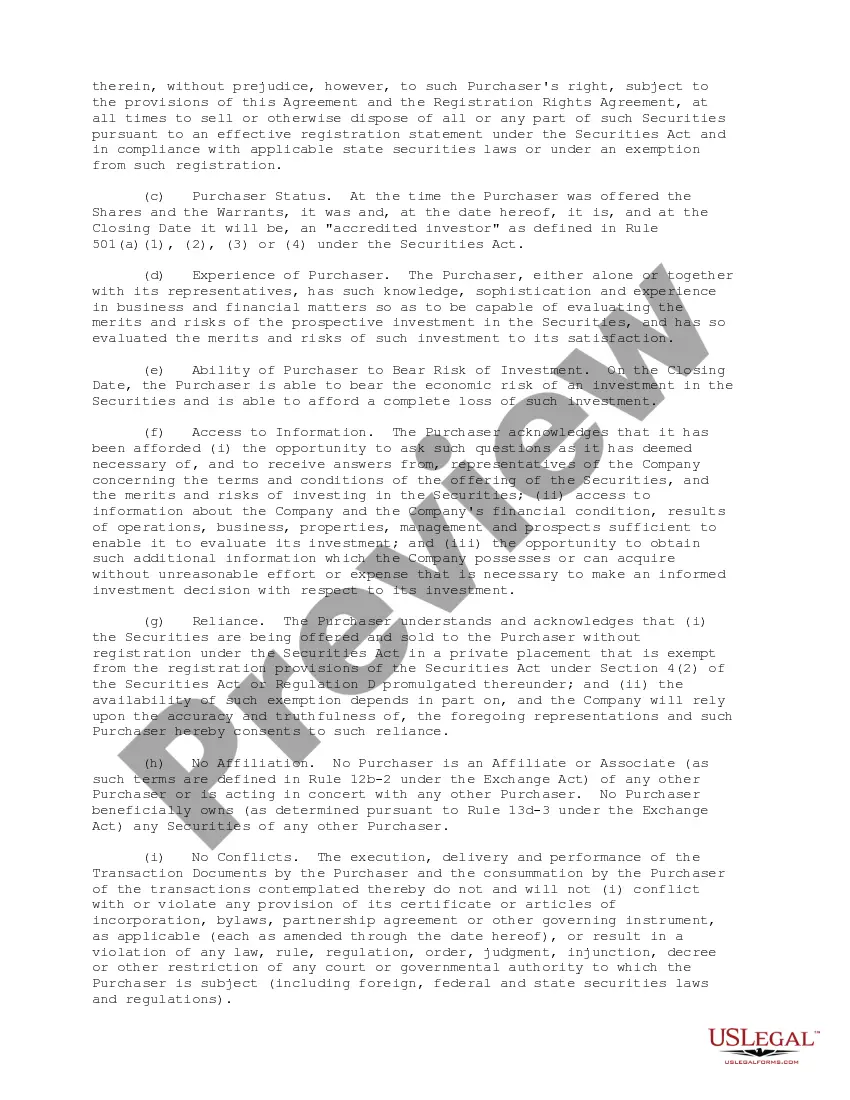

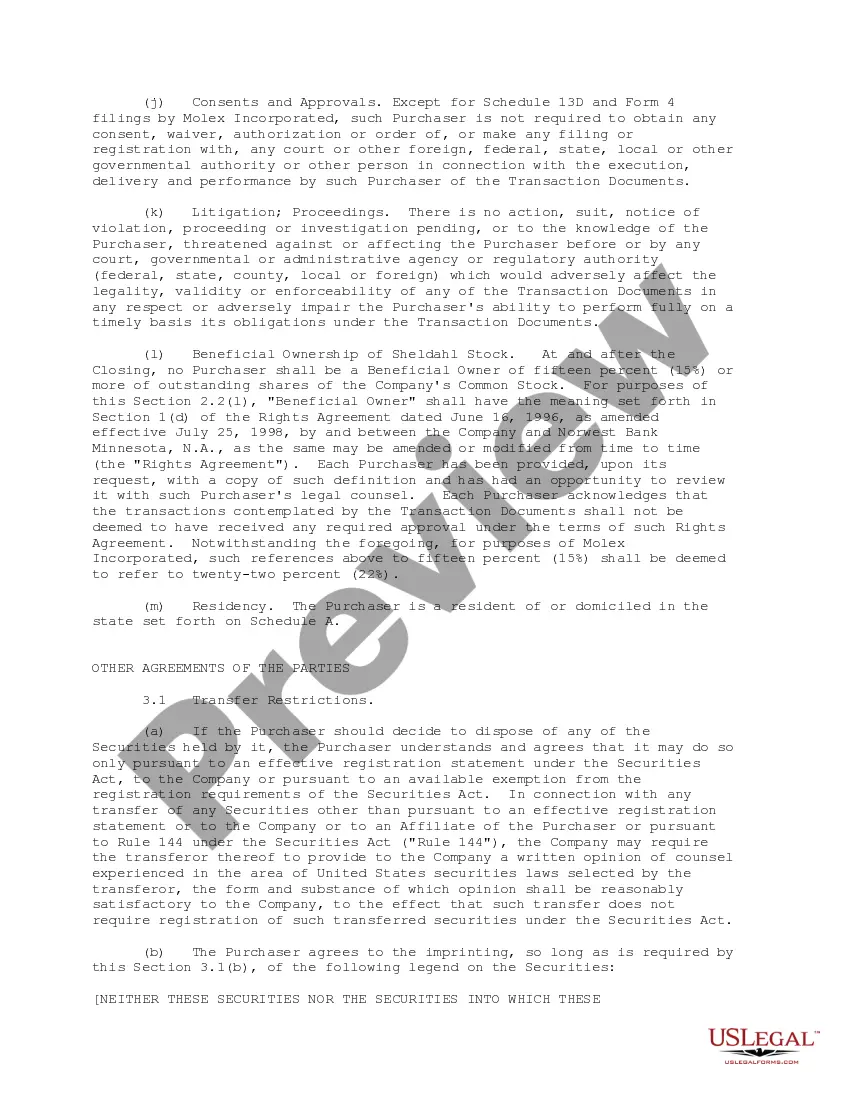

Convertible Preferred Stock Purchase Agreement between Sheldahl, Inc., Molex Incorporated and Richard C. Wilcox, Jr. dated January 11, 2000. 12 pages

Free preview Convertible Preferred Stock