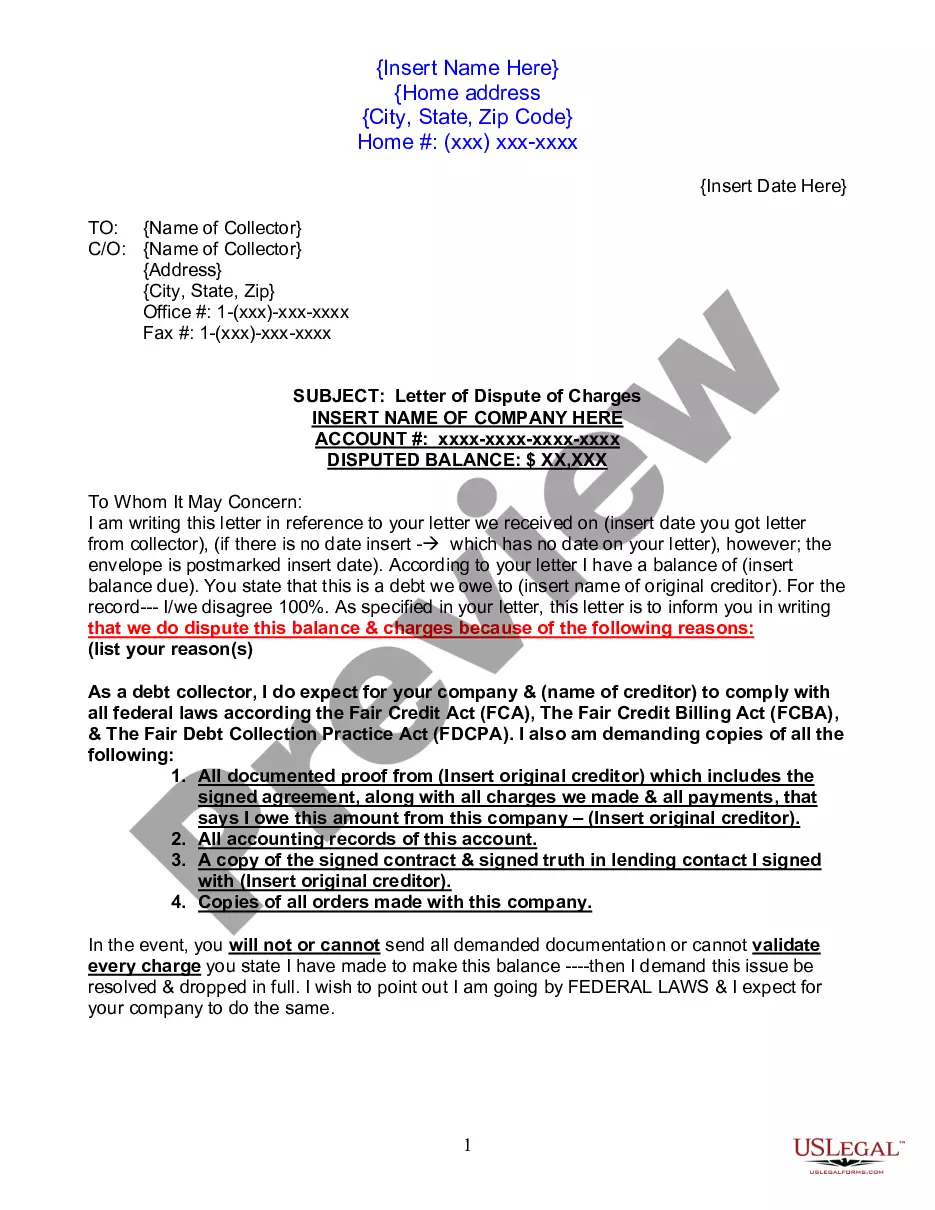

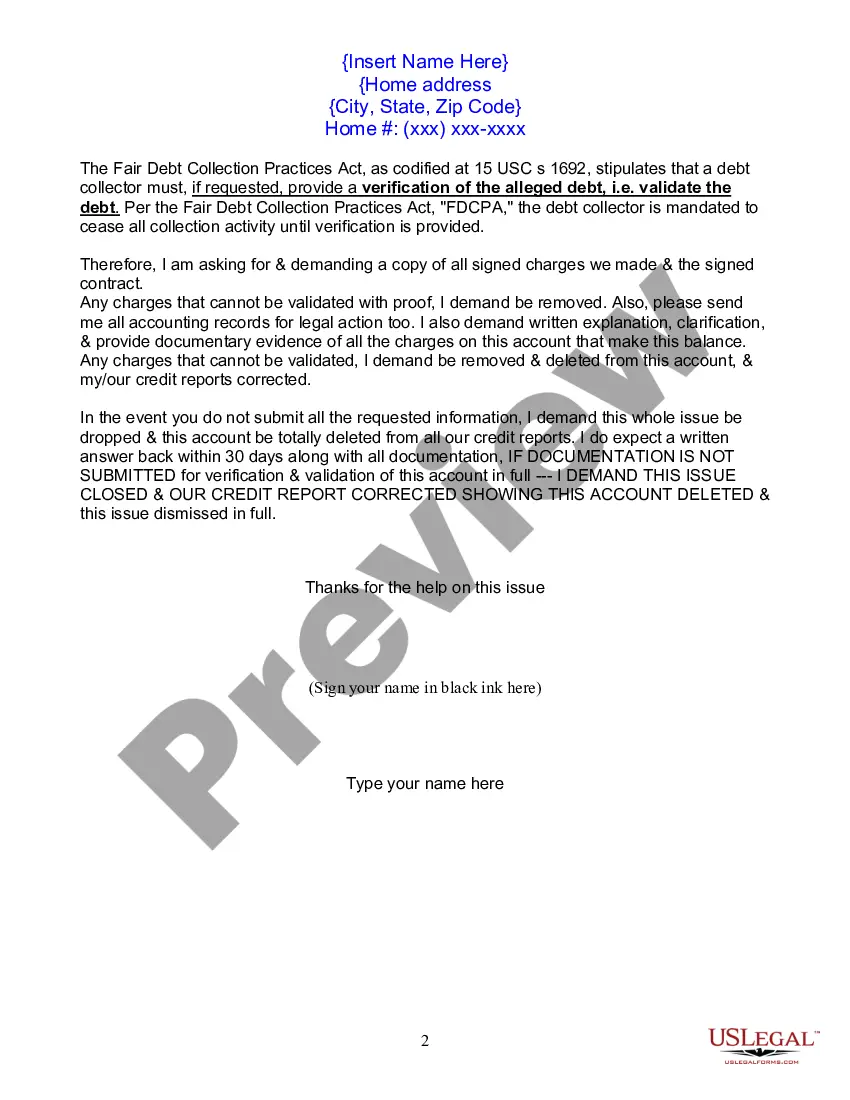

This form is to be used when a collection company is demanding full payment from you and you disagree with the balance. Use this form as your first letter of dispute.

A 609 letter is a powerful tool used by consumers to remove late payments from their credit reports. It is based on a specific section of the Fair Credit Reporting Act (FCRA) and can be an effective way to restore one's credit score. This detailed description will shed light on what a 609 letter is, how it works, and the different types of 609 letters to remove late payments. What is a 609 letter to remove late payments? A 609 letter is a written request to dispute and remove late payments from your credit report. It derives its name from the section 609 of the FCRA, which grants consumers the right to request information and challenge any inaccurate or unverifiable data on their credit reports. When it comes to late payments, this type of letter can be instrumental in rectifying errors or unfair reporting. How does a 609 letter work? To launch the 609 letter process, you must write a formal letter to the credit bureaus — Experian, Equifax, and TransUnion. In this letter, you request detailed information about the late payments reported on your credit report. This includes the original creditor's name, account number, dates, and any supporting documentation they can provide to validate their claim. The credit bureaus then have a legal obligation to investigate your request and respond within a specific timeframe. Different types of 609 letters to remove late payments: 1. Standard 609 Letter: This is the most common type of 609 letters used to dispute late payments associated with various accounts on your credit report. It can be sent to each of the three major credit bureaus simultaneously or individually. 2. Advanced 609 Letter: This type of letter goes beyond the standard format by providing additional arguments, evidence, or legal references to support your dispute. It could be useful if you have unique circumstances or if the standard 609 letters didn't yield the desired results initially. 3. Section 609© Sample Letter: Under section 609(c) of the FCRA, there is a provision that allows you to request a reinvestigation after receiving incomplete or inaccurate information from the credit bureaus. This sample letter helps you exercise this right and challenge the late payments after inadequate investigation from the bureaus. 4. Cease and Desist Letter: If late payments continue to be reported inaccurately even after the 609 letter process, a cease and desist letter may be necessary. This letter advises the creditor to stop reporting incorrect information, warning of potential legal action if they persist. In summary, a 609 letter is a strategic tool for consumers to remove late payments from their credit reports. By leveraging the FCRA, individuals can exercise their rights to request and challenge the accuracy of reported late payments. These letters come in different types based on specific purposes, from the standard to the advanced, section 609(c) sample, and even cease and desist letters. Remember to carefully craft your letter, provide supporting evidence, and follow up with the credit bureaus to maximize your chances of success in rectifying any inaccurate late payment entries on your credit report.