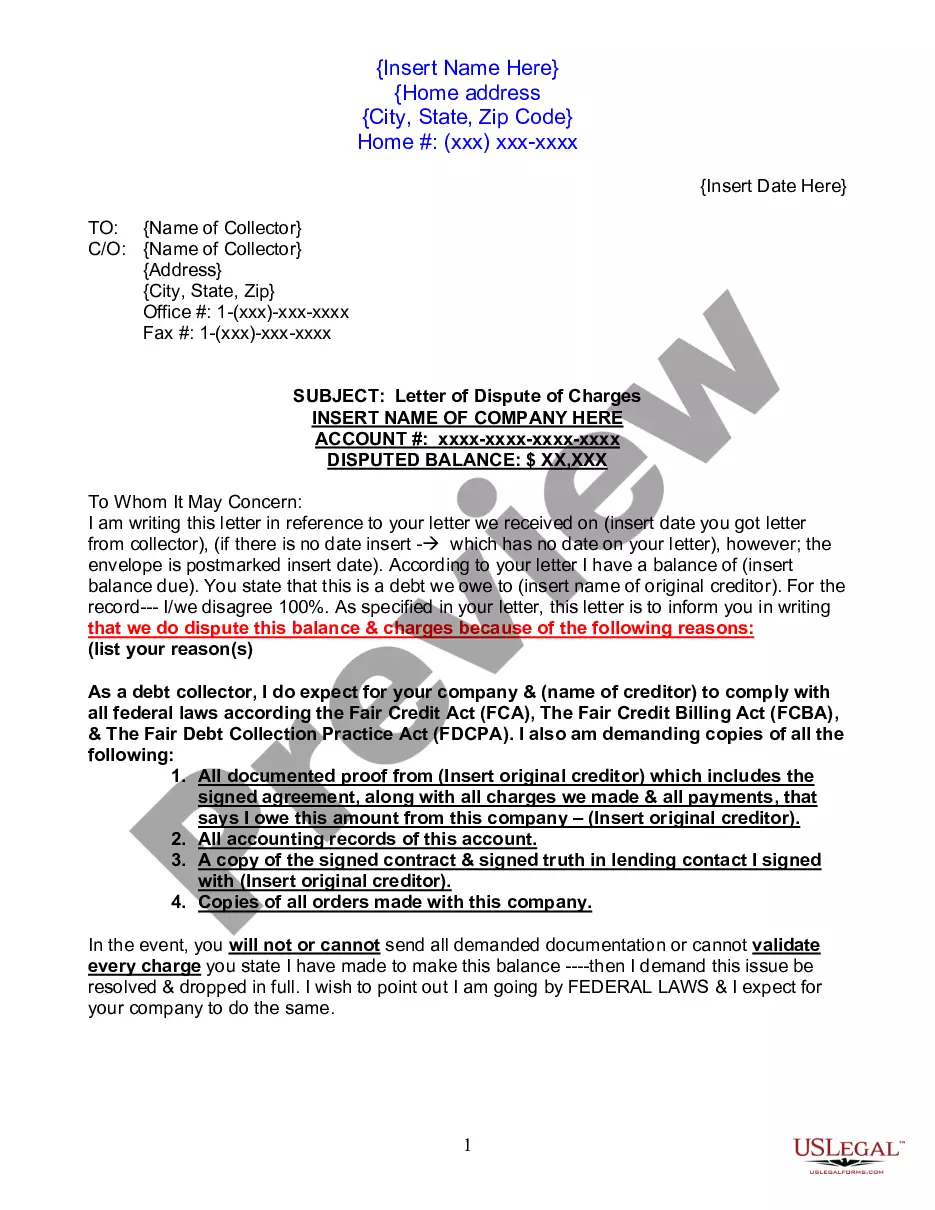

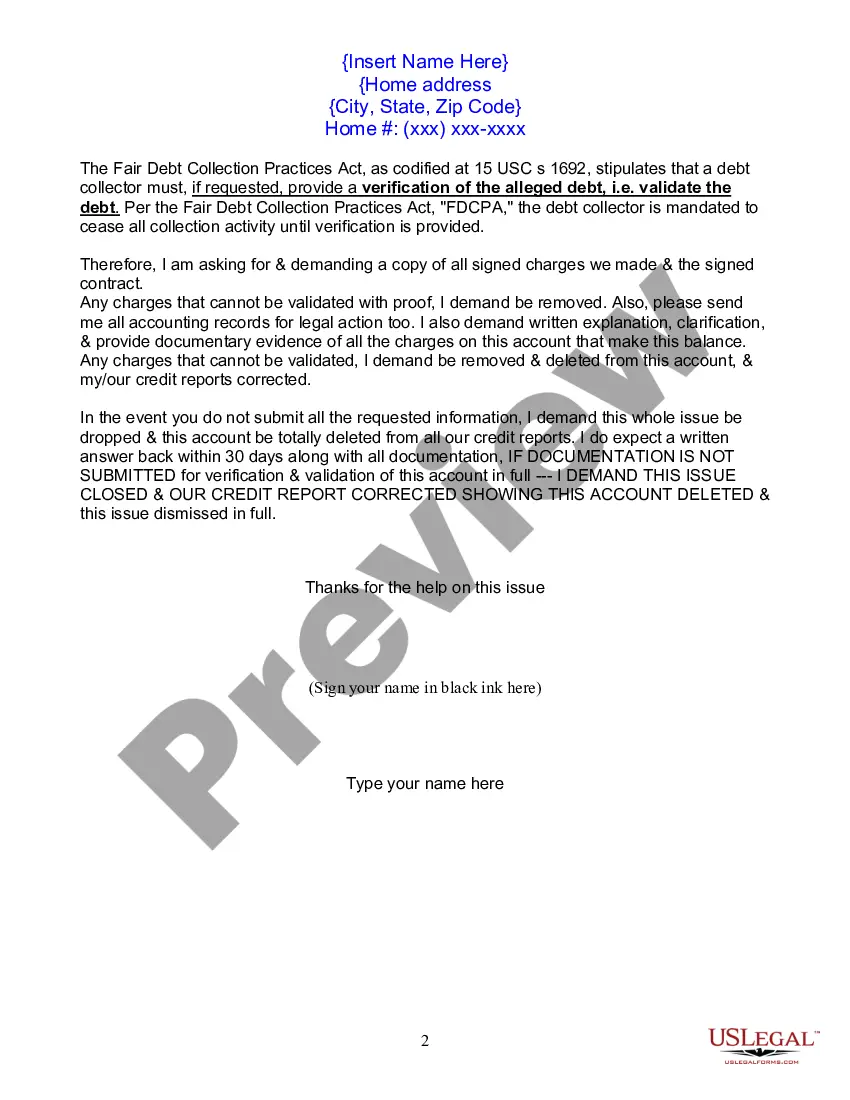

This form is to be used when a collection company is demanding full payment from you and you disagree with the balance. Use this form as your first letter of dispute.

Dispute letters for late payments are written correspondence to address issues pertaining to unpaid or late payments. These letters serve as a formal means of communication to rectify payment discrepancies and resolve disputes between the creditor and the debtor. They can be sent to various parties such as creditors, collection agencies, or credit bureaus, depending on the specific situation. The primary objective of a dispute letter for late payments is to rectify any inaccuracies or errors in payment records, credit reports, or billing statements. The letter outlines the specific payment discrepancies while providing supporting documentation to substantiate the claim. By doing so, the debtor seeks to have the late payment(s) removed from their credit report, avoid negative consequences on their credit score, and ensure accurate financial records. These dispute letters typically include key elements such as: 1. Contact Information: The sender's and recipient's contact details, including full names, addresses, phone numbers, and email addresses. 2. Date: The date on which the letter is being written and sent. 3. Account Information: Details about the account in question, such as account numbers, billing statements, payment dates, and amounts. 4. Explanation of Discrepancies: A clear and concise description of the specific payment discrepancies, including dates and amounts, highlighting why they are considered errors or inaccuracies. 5. Supporting Documentation: Attachments or copies of relevant documents, such as payment receipts, bank statements, canceled checks, or any other proof that supports the claim of an incorrect late payment. 6. Request for Resolution: A statement requesting the recipient to investigate the matter, correct any errors, and provide written confirmation of the resolution within a reasonable time frame. 7. Professional Tone: The letter should be written in a polite, professional, and assertive manner, avoiding any emotional language or confrontational tone. Additionally, different types of dispute letters for late payments can be categorized based on the recipient they are intended for: 1. Creditors: Letters addressed directly to the original creditor, such as a bank, utility company, or service provider, to resolve payment discrepancies before they get reported to credit bureaus. 2. Collection Agencies: Letters sent to third-party collection agencies, requesting validation of the debt, clarification of payment history, or disputing the accuracy of late payment records. 3. Credit Bureaus: Letters forwarded to credit reporting agencies, like Equifax, Experian, or TransUnion, to dispute the inclusion of late or incorrect payment information in credit reports. By effectively utilizing dispute letters for late payments, individuals can ensure accurate credit reporting and maintain a favorable credit standing, which is crucial for securing future loans, mortgages, or credit card applications.Dispute letters for late payments are written correspondence to address issues pertaining to unpaid or late payments. These letters serve as a formal means of communication to rectify payment discrepancies and resolve disputes between the creditor and the debtor. They can be sent to various parties such as creditors, collection agencies, or credit bureaus, depending on the specific situation. The primary objective of a dispute letter for late payments is to rectify any inaccuracies or errors in payment records, credit reports, or billing statements. The letter outlines the specific payment discrepancies while providing supporting documentation to substantiate the claim. By doing so, the debtor seeks to have the late payment(s) removed from their credit report, avoid negative consequences on their credit score, and ensure accurate financial records. These dispute letters typically include key elements such as: 1. Contact Information: The sender's and recipient's contact details, including full names, addresses, phone numbers, and email addresses. 2. Date: The date on which the letter is being written and sent. 3. Account Information: Details about the account in question, such as account numbers, billing statements, payment dates, and amounts. 4. Explanation of Discrepancies: A clear and concise description of the specific payment discrepancies, including dates and amounts, highlighting why they are considered errors or inaccuracies. 5. Supporting Documentation: Attachments or copies of relevant documents, such as payment receipts, bank statements, canceled checks, or any other proof that supports the claim of an incorrect late payment. 6. Request for Resolution: A statement requesting the recipient to investigate the matter, correct any errors, and provide written confirmation of the resolution within a reasonable time frame. 7. Professional Tone: The letter should be written in a polite, professional, and assertive manner, avoiding any emotional language or confrontational tone. Additionally, different types of dispute letters for late payments can be categorized based on the recipient they are intended for: 1. Creditors: Letters addressed directly to the original creditor, such as a bank, utility company, or service provider, to resolve payment discrepancies before they get reported to credit bureaus. 2. Collection Agencies: Letters sent to third-party collection agencies, requesting validation of the debt, clarification of payment history, or disputing the accuracy of late payment records. 3. Credit Bureaus: Letters forwarded to credit reporting agencies, like Equifax, Experian, or TransUnion, to dispute the inclusion of late or incorrect payment information in credit reports. By effectively utilizing dispute letters for late payments, individuals can ensure accurate credit reporting and maintain a favorable credit standing, which is crucial for securing future loans, mortgages, or credit card applications.