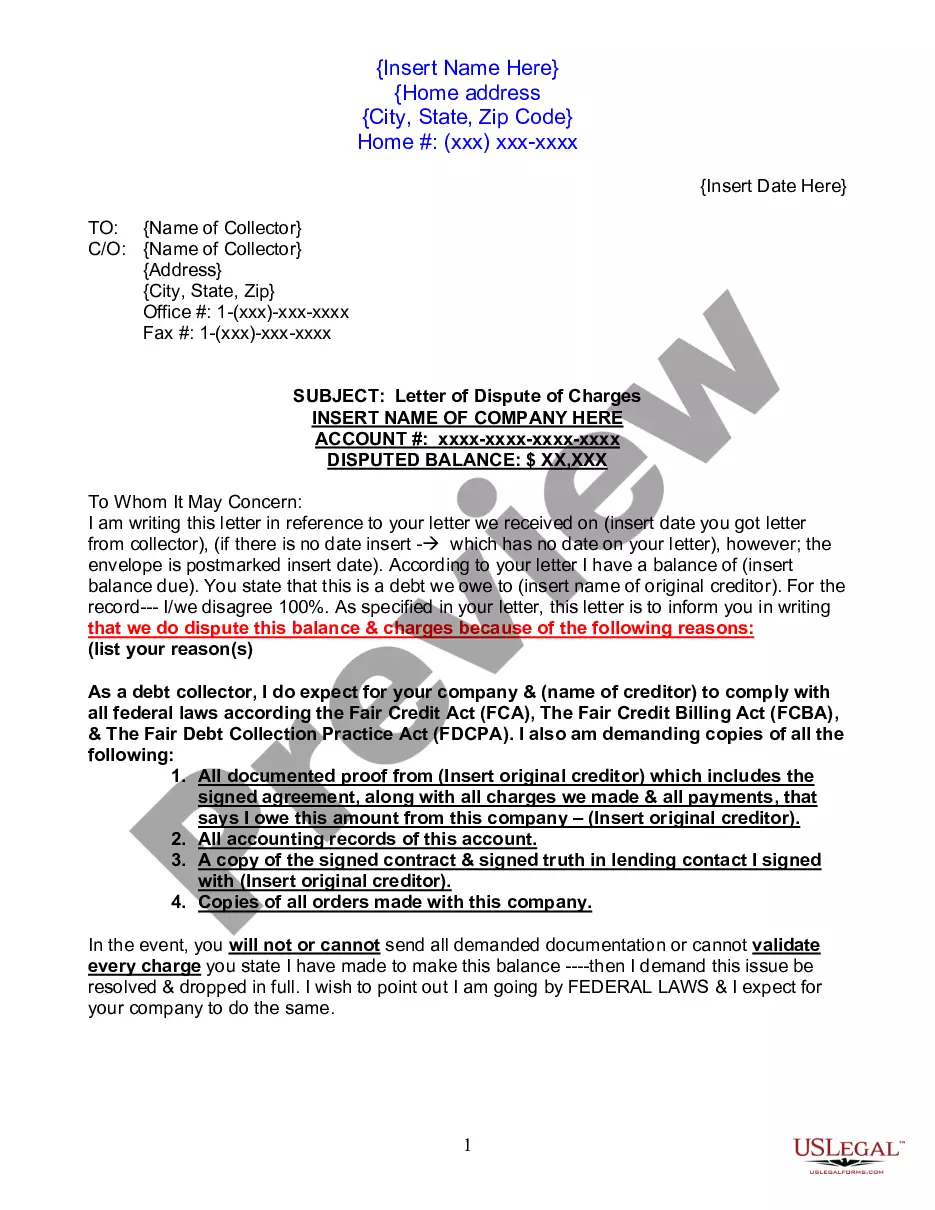

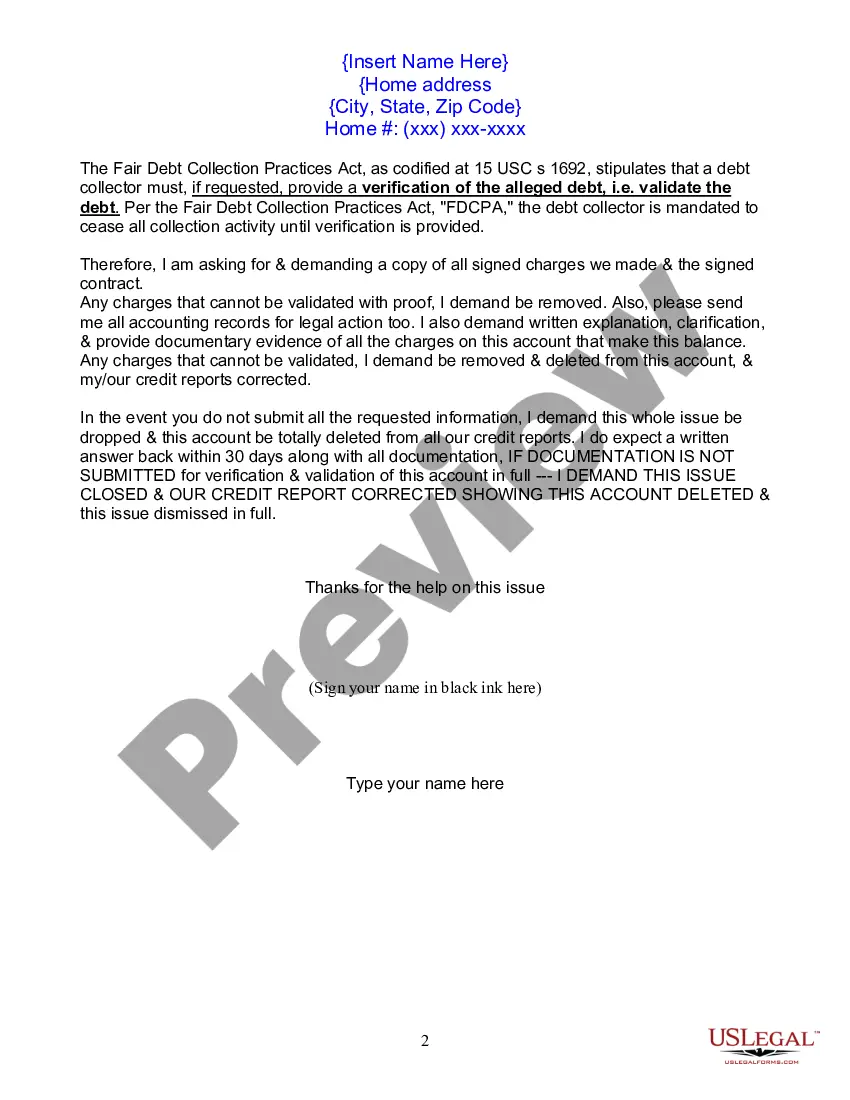

This form is to be used when a collection company is demanding full payment from you and you disagree with the balance. Use this form as your first letter of dispute.

Section 604 dispute letter for credit refers to a specific type of communication that consumers can initiate with credit reporting agencies or credit bureaus to challenge inaccurate or incomplete information on their credit reports. This letter, as mandated by the Fair Credit Reporting Act (FCRA), empowers individuals to rectify any discrepancies and maintain accurate credit profiles. By highlighting relevant keywords, the description can be optimized for better visibility and search engine rankings. Keywords: Section 604 dispute letter for credit, credit reporting agencies, credit bureaus, inaccurate information, incomplete information, credit reports, Fair Credit Reporting Act, FCRA, discrepancies, accurate credit profiles. There are two primary types of Section 604 dispute letters for credit: 1. General Section 604 Dispute Letter: This type of letter is used to address any inaccuracies, errors, or incomplete information found on a credit report. It includes details such as personal information (name, address, social security number), disputed account specifics (account name, account number), and a clear explanation of the error or dispute. Supporting documents, such as payment receipts or correspondence, can also be included to strengthen the case. The letter must be sent via certified mail with a return receipt requested to ensure delivery and have a record for potential legal purposes. 2. Identity Theft Section 604 Dispute Letter: In cases where an individual's identity has been stolen or used fraudulently, an identity theft dispute letter should be utilized. This letter should explain the suspected identity theft incident, provide relevant details (such as police report numbers or other supporting evidence), and request the removal of any fraudulent accounts or activities from the credit report. Additionally, including a copy of the Identity Theft Report filed with the Federal Trade Commission (FTC) is advisable to establish the seriousness of the situation and further strengthen the claim. Irrespective of the type, it is crucial to maintain a professional tone throughout the letter and clearly articulate the desired outcome — typically the removal or correction of the disputed information. Timely submission of the dispute letter is crucial since credit bureaus are legally mandated to investigate and respond within 30 days of receiving the letter.Section 604 dispute letter for credit refers to a specific type of communication that consumers can initiate with credit reporting agencies or credit bureaus to challenge inaccurate or incomplete information on their credit reports. This letter, as mandated by the Fair Credit Reporting Act (FCRA), empowers individuals to rectify any discrepancies and maintain accurate credit profiles. By highlighting relevant keywords, the description can be optimized for better visibility and search engine rankings. Keywords: Section 604 dispute letter for credit, credit reporting agencies, credit bureaus, inaccurate information, incomplete information, credit reports, Fair Credit Reporting Act, FCRA, discrepancies, accurate credit profiles. There are two primary types of Section 604 dispute letters for credit: 1. General Section 604 Dispute Letter: This type of letter is used to address any inaccuracies, errors, or incomplete information found on a credit report. It includes details such as personal information (name, address, social security number), disputed account specifics (account name, account number), and a clear explanation of the error or dispute. Supporting documents, such as payment receipts or correspondence, can also be included to strengthen the case. The letter must be sent via certified mail with a return receipt requested to ensure delivery and have a record for potential legal purposes. 2. Identity Theft Section 604 Dispute Letter: In cases where an individual's identity has been stolen or used fraudulently, an identity theft dispute letter should be utilized. This letter should explain the suspected identity theft incident, provide relevant details (such as police report numbers or other supporting evidence), and request the removal of any fraudulent accounts or activities from the credit report. Additionally, including a copy of the Identity Theft Report filed with the Federal Trade Commission (FTC) is advisable to establish the seriousness of the situation and further strengthen the claim. Irrespective of the type, it is crucial to maintain a professional tone throughout the letter and clearly articulate the desired outcome — typically the removal or correction of the disputed information. Timely submission of the dispute letter is crucial since credit bureaus are legally mandated to investigate and respond within 30 days of receiving the letter.