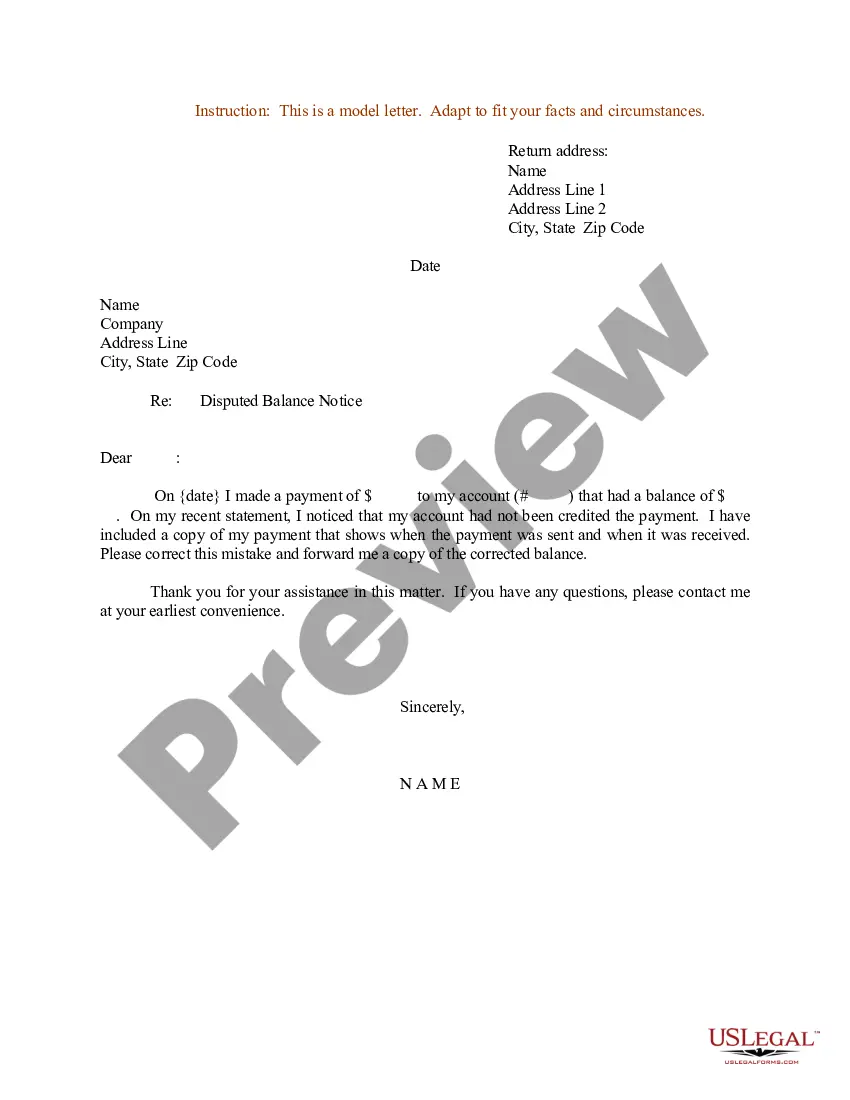

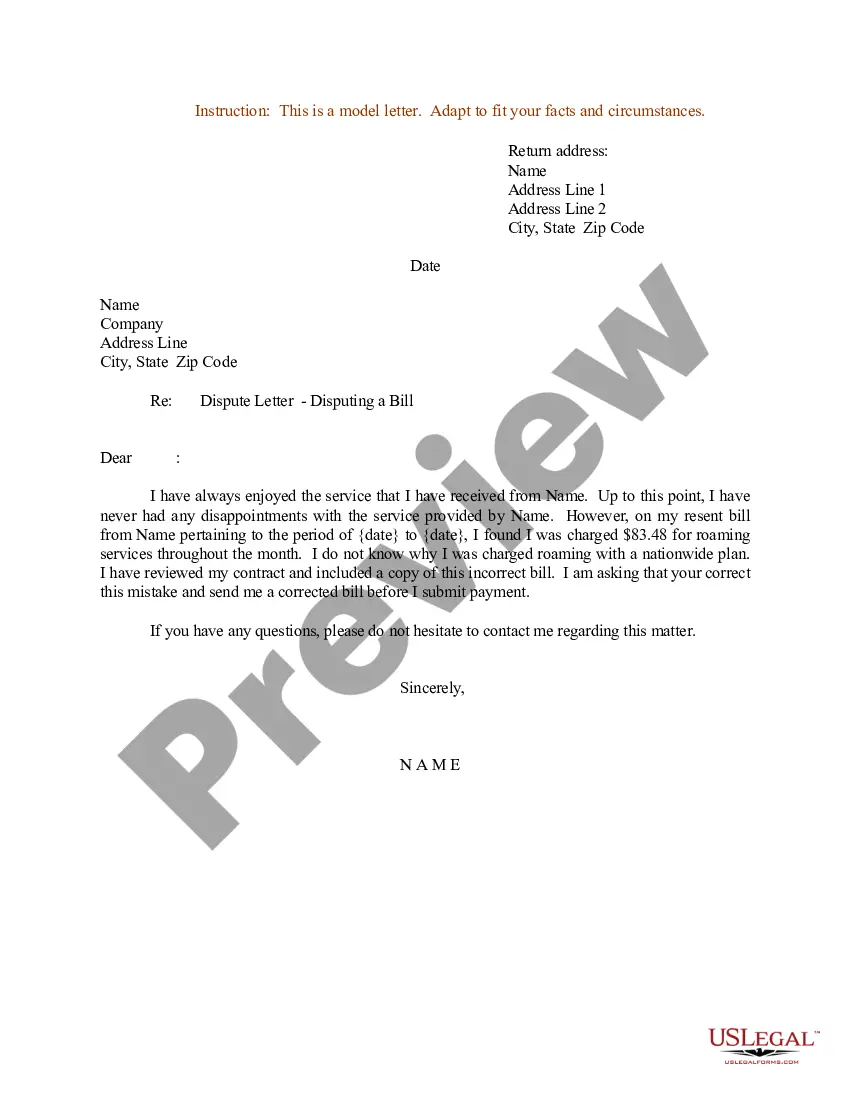

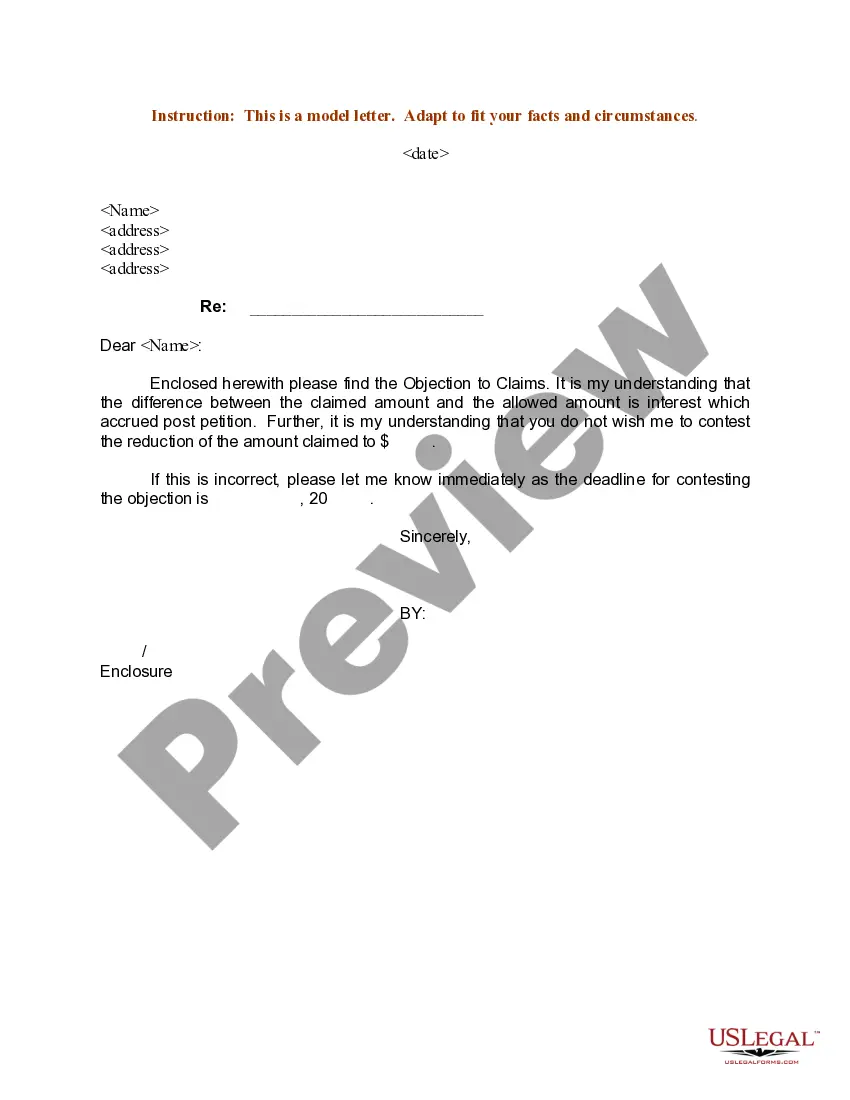

Section 604 Dispute Letter With Credit Report

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Letter Of Dispute - Complete Balance?

It’s well known that you cannot transform into a legal specialist instantly, nor can you quickly learn how to prepare the Section 604 Dispute Letter With Credit Report without possessing a specialized skill set.

Compiling legal documents is a lengthy endeavor that necessitates particular training and expertise. So why not entrust the development of the Section 604 Dispute Letter With Credit Report to the professionals.

With US Legal Forms, one of the most extensive legal template collections, you can find everything from court documents to templates for internal corporate communications. We recognize the significance of compliance and adherence to federal and local laws and regulations.

Select Buy now. Once the payment is completed, you can download the Section 604 Dispute Letter With Credit Report, fill it out, print it, and send it to the necessary individuals or organizations.

You can regain access to your documents from the My documents tab at any time. If you are a current customer, you can simply Log In and find and download the template from the same tab.

- Here’s how to get started with our platform and obtain the document you need in just a few minutes.

- Locate the form you seek using the search bar at the top of the page.

- Preview it (if this feature is available) and examine the accompanying description to see if the Section 604 Dispute Letter With Credit Report is what you are looking for.

- If you require any additional template, restart your search.

- Create a free account and choose a subscription plan to buy the form.

Form popularity

FAQ

Examples of these documents include birth certificates, contracts, deeds, leases, titles, wills, etc. During a trial or in preparation of a trial, documents such as a complaint or a summons can also be referred to as legal papers.

Important points to include in a legal document. Party details. List the names, numbers, addresses (email or physical), and any other relevant information of all parties involved. ... Background information. ... Motion. ... Roles and responsibilities. ... Breaches or contingencies. ... Dates and signatures.

Legal documents, such as contracts and agreements, are mutual promises between two or more parties. They can be seen everywhere ? from business deals and employee contracts to residential leases and settlement agreements.

There are many types of legal documents, but here, we will focus on some of the most common ones, including contracts, wills, deeds, power of attorney, affidavits, and deposition.

1. Will. A will is a legal document that designates who should receive your assets after death.

The 4 legal documents every adult should have A will. Also known as: a last will and testament. ... A living will. Also known as: an advance directive. ... Durable health care power of attorney. It appoints: a health care proxy. ... Durable financial power of attorney. It appoints: an attorney-in-fact or agent.

Free Online Legal Form & Document Creator.

Defining a Legal Document A legal document is typically characterized by its structure, content, and language. It's meticulously crafted, often by legal professionals, to ensure precision and accuracy. The language used is formal and specific, adhering to legal terminologies and protocols to avoid ambiguity.