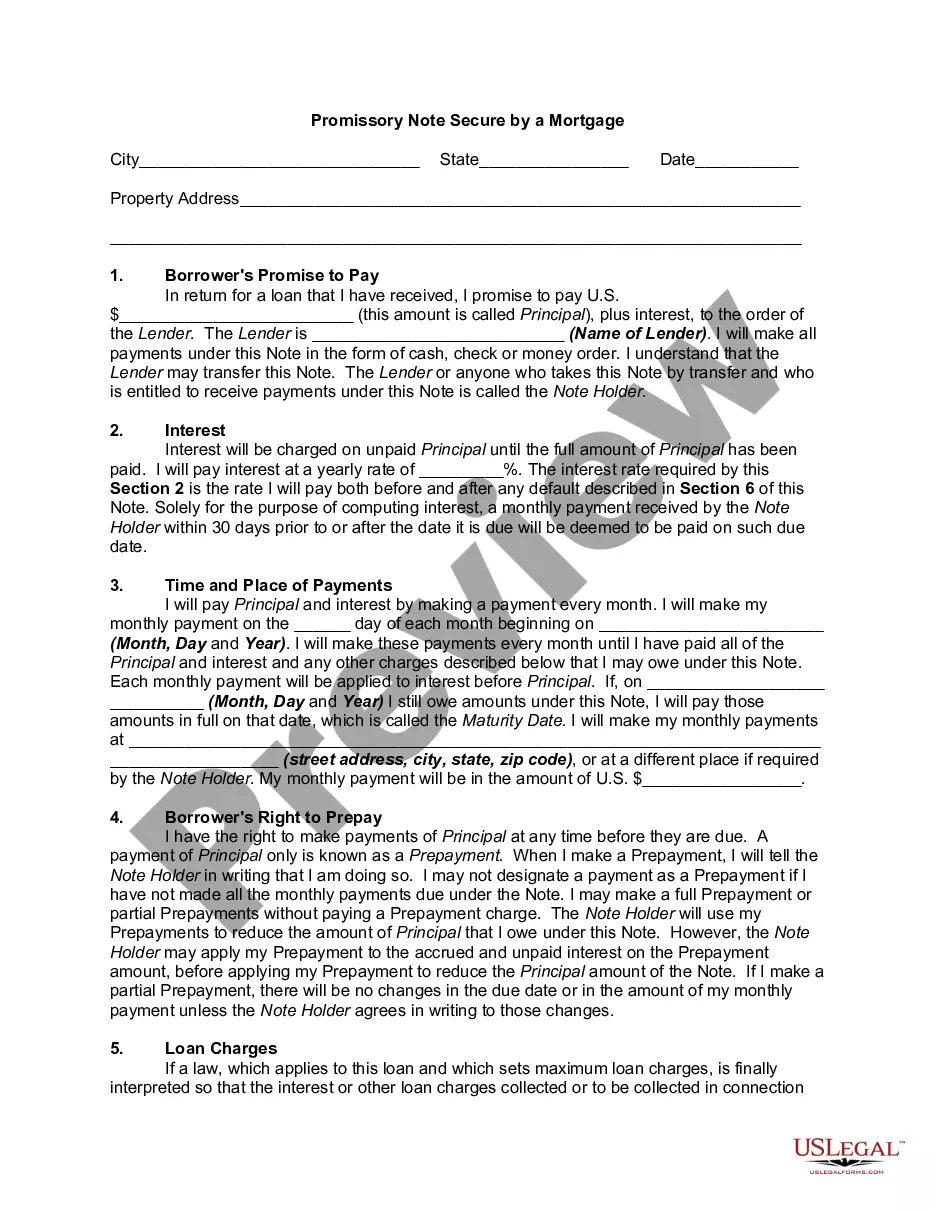

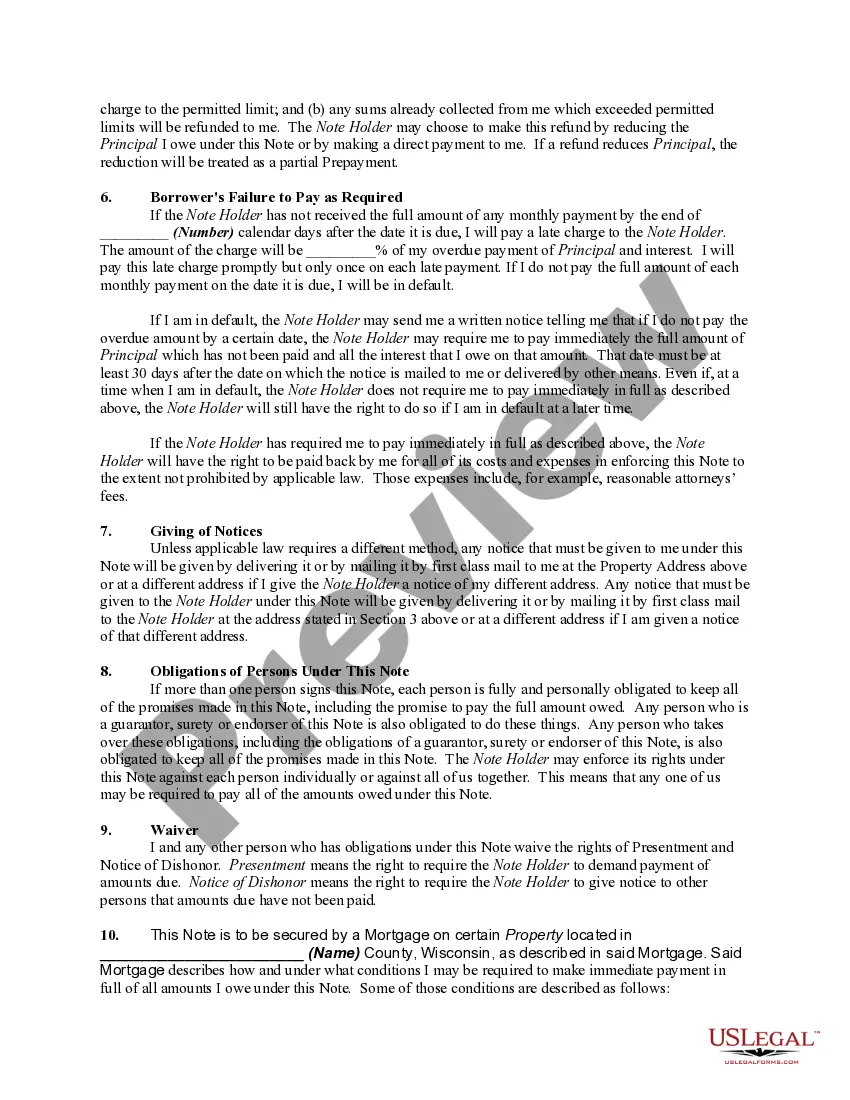

This promissory is a form that can be used in a transaction between one individual and another as opposed to an individual and lender bank.

Are you new to the world of mortgages and finding it hard to understand the concept of a mortgage note? Fear not, for in this article, we will provide you with a detailed description of what a mortgage note is, utilizing keywords relevant to your query. A mortgage note, sometimes called a promissory note or a loan agreement, is a legal document that outlines the terms and conditions of a mortgage loan. This document is essential in real estate transactions, as it serves as evidence of the borrower's promise to repay the lender the borrowed amount, typically used to finance the purchase of a property. Keywords: mortgage note, dummies, detailed description, types. There are different types of mortgage notes that one might come across, tailored for specific needs and situations. Let's dive into a few examples: 1. Fixed-Rate Mortgage Note: This type of mortgage note is the most common. It stipulates that the interest rate remains fixed throughout the loan term, providing borrowers with a predictable repayment structure. This is ideal for individuals seeking stability and wanting to budget their finances efficiently. 2. Adjustable-Rate Mortgage (ARM) Note: Unlike fixed-rate mortgage notes, ARM notes have an interest rate that can fluctuate over time. Typically, the interest rate is fixed for an initial period, commonly five or seven years, and then adjusts periodically based on market conditions. ARM notes are suitable for borrowers who expect interest rates to decrease or individuals who plan to sell or refinance their property before the rate adjustments occur. 3. Balloon Mortgage Note: This type of mortgage note offers lower initial monthly payments, followed by a large lump sum payment, also called the balloon payment at the end of the loan term. Balloon mortgage notes are best suited for individuals who anticipate a significant influx of funds in the future, such as from the sale of an asset or an inheritance. 4. Interest-Only Mortgage Note: With an interest-only mortgage note, the borrower is only required to pay the interest accrued on the loan for a specified period. This allows borrowers to have lower initial monthly payments. However, after the interest-only period ends, the borrower must start making principal and interest payments, which are typically higher. Interest-only mortgage notes are often chosen by individuals who expect their income to increase or those who plan to sell or refinance their property before the principal payments start. Understanding different types of mortgage notes is crucial as it allows borrowers to select the option that aligns with their financial goals and circumstances. Remember, before signing any mortgage note, it is essential to review the terms with a loan officer or mortgage professional to ensure you comprehend the obligations and responsibilities associated with the loan. In conclusion, a mortgage note is a legal document that outlines the terms and conditions of a mortgage loan. It establishes the borrower's promise to repay the lender and serves as evidence of the loan agreement. By familiarizing yourself with different types of mortgage notes, such as fixed-rate, adjustable-rate, balloon, and interest-only, you can make an informed decision that suits your financial needs.