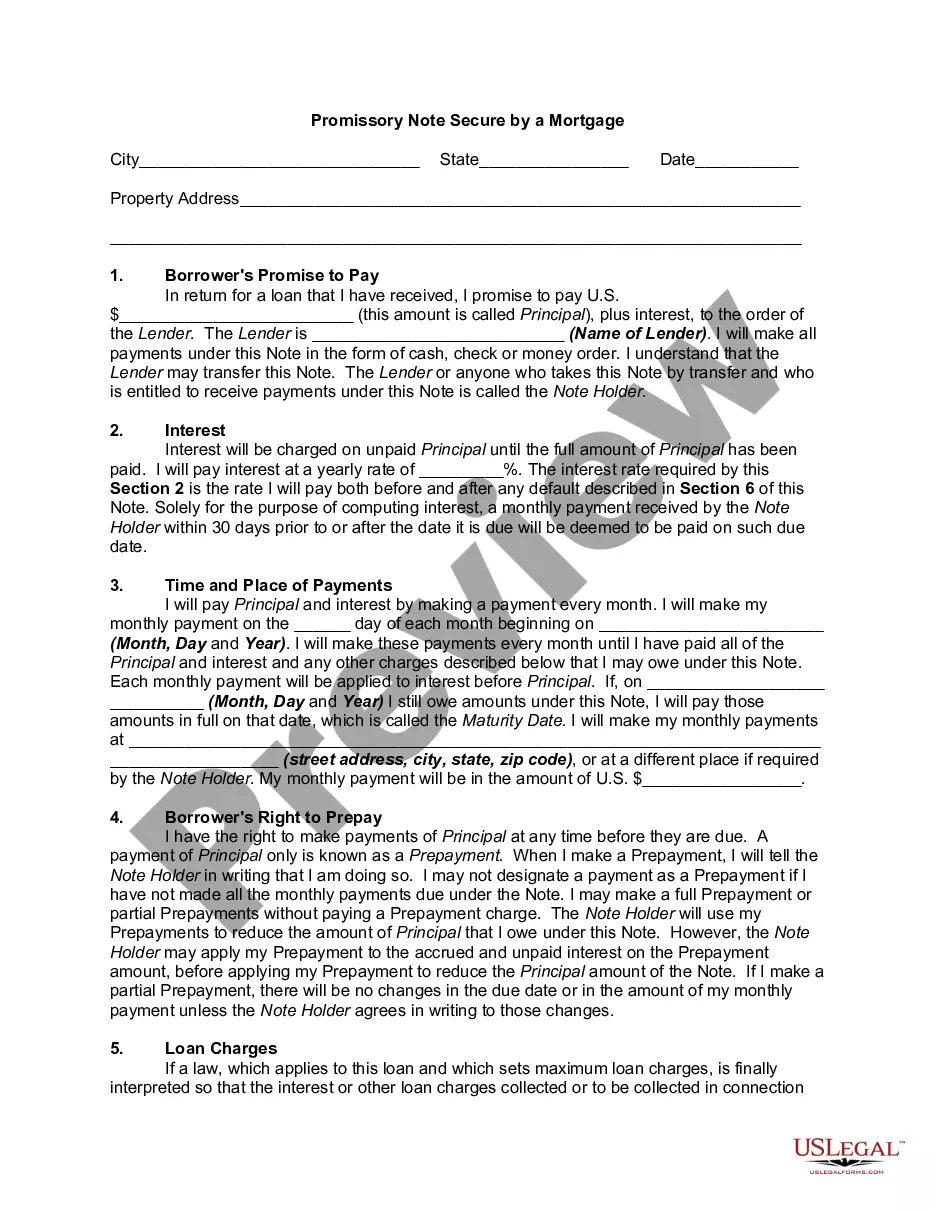

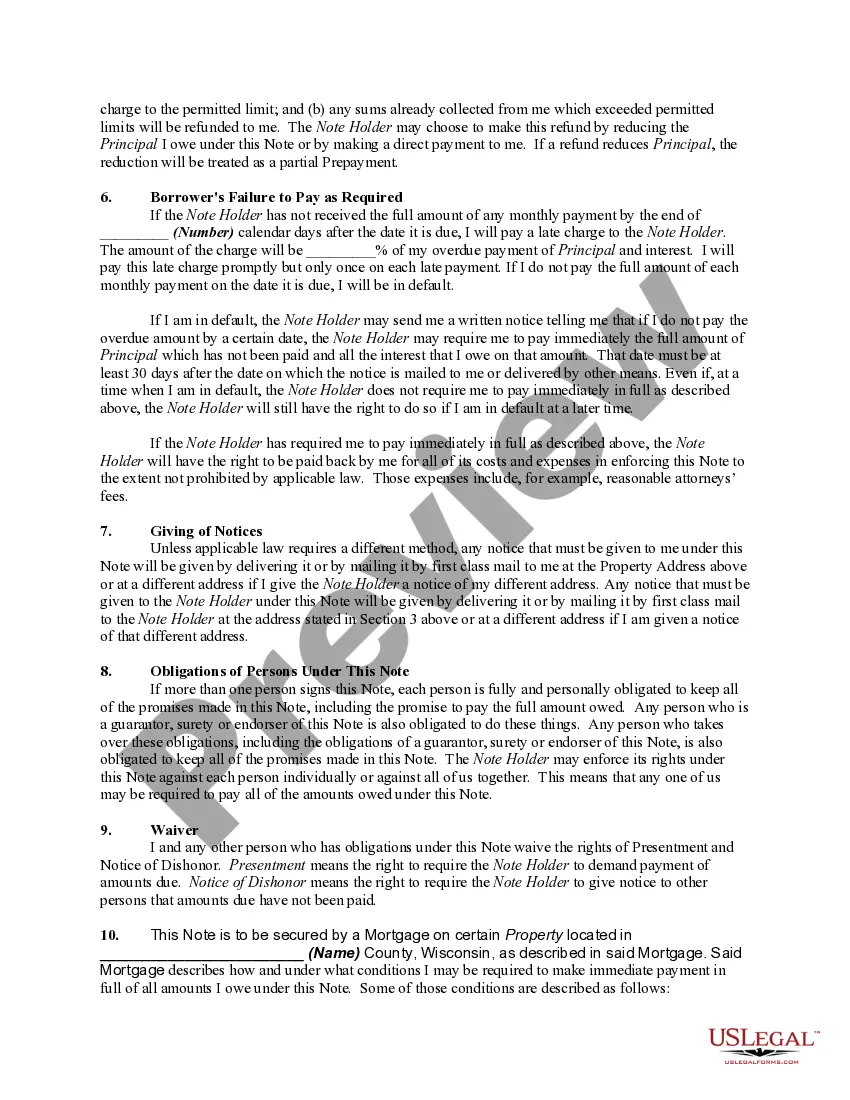

This promissory is a form that can be used in a transaction between one individual and another as opposed to an individual and lender bank.

A mortgage note example for a HELOT (Home Equity Line of Credit) serves as the legal document that outlines the terms and conditions of the loan, including repayment terms, interest rate, and any other relevant details. It is a crucial document that both the borrower and the lender must agree upon and sign. Here is an example of the key contents typically found in a mortgage note for a HELOT: 1. Parties involved: The mortgage note begins by identifying the borrower and the lender. It includes their legal names, addresses, and contact information. 2. Loan amount: The mortgage note specifies the total loan amount, which represents the maximum credit limit that the borrower can draw from their HELOT. 3. Interest rate: This section outlines the interest rate charged on the borrowed funds. It may be a fixed or variable rate, depending on the terms agreed upon. 4. Repayment terms: The mortgage note includes detailed information about the repayment schedule, which includes the minimum monthly payments required. It also mentions any penalties or fees associated with late or missed payments. 5. Draw period: In the case of a HELOT, there is typically an initial draw period during which the borrower can access funds. The mortgage note specifies the duration of this period, usually ranging from 5 to 10 years. 6. Repayment period: After the draw period ends, the mortgage note outlines the repayment period during which the borrower must repay the outstanding balance. The duration of this period can vary and is mentioned in the document. 7. Payment calculation method: The mortgage note specifies how the minimum monthly payment is calculated. It can be a percentage of the outstanding balance or a fixed amount. 8. Prepayment clauses: This section includes information on whether the borrower is allowed to make additional payments towards the principal or pay off the loan early, and if any penalties or fees apply for doing so. 9. Default and foreclosure: The mortgage note outlines the consequences if the borrower fails to meet the repayment obligations, including potential default, foreclosure procedures, and any associated costs. 10. Other terms: The document may include additional terms, such as insurance requirements, escrow accounts, or any special conditions agreed upon by both parties. Different types of mortgage notes for Helots can vary based on the specific agreements between the borrower and the lender. These may include variations in interest rates, repayment terms, or draw and repayment periods. It is crucial for borrowers to carefully review and understand the contents of their mortgage note before signing. Overall, a mortgage note example for a HELOT serves as a legally binding agreement between the borrower and the lender, establishing the terms and conditions of the loan. It is essential to consult with professionals, such as mortgage brokers or attorneys, to ensure a thorough understanding of the mortgage note's contents and potential implications.