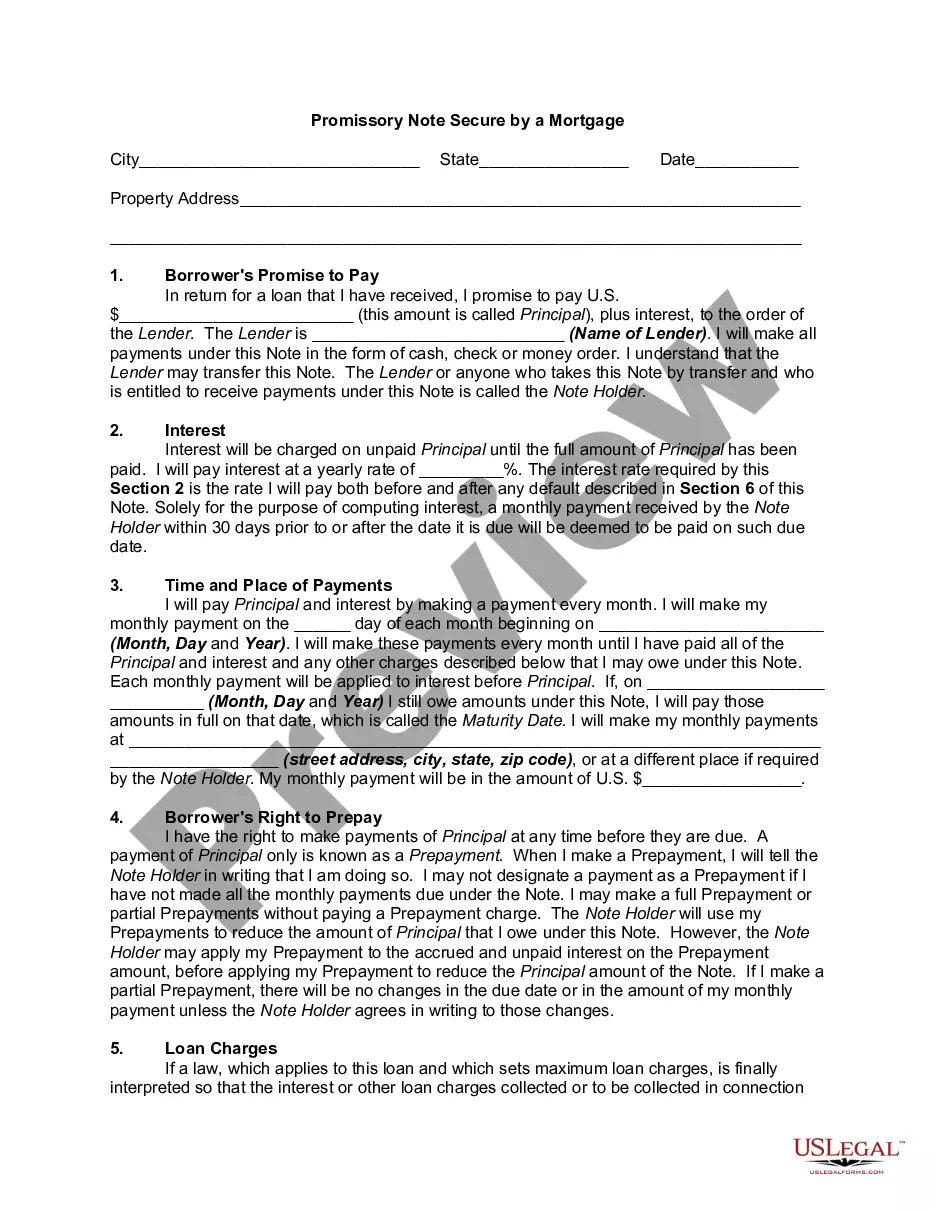

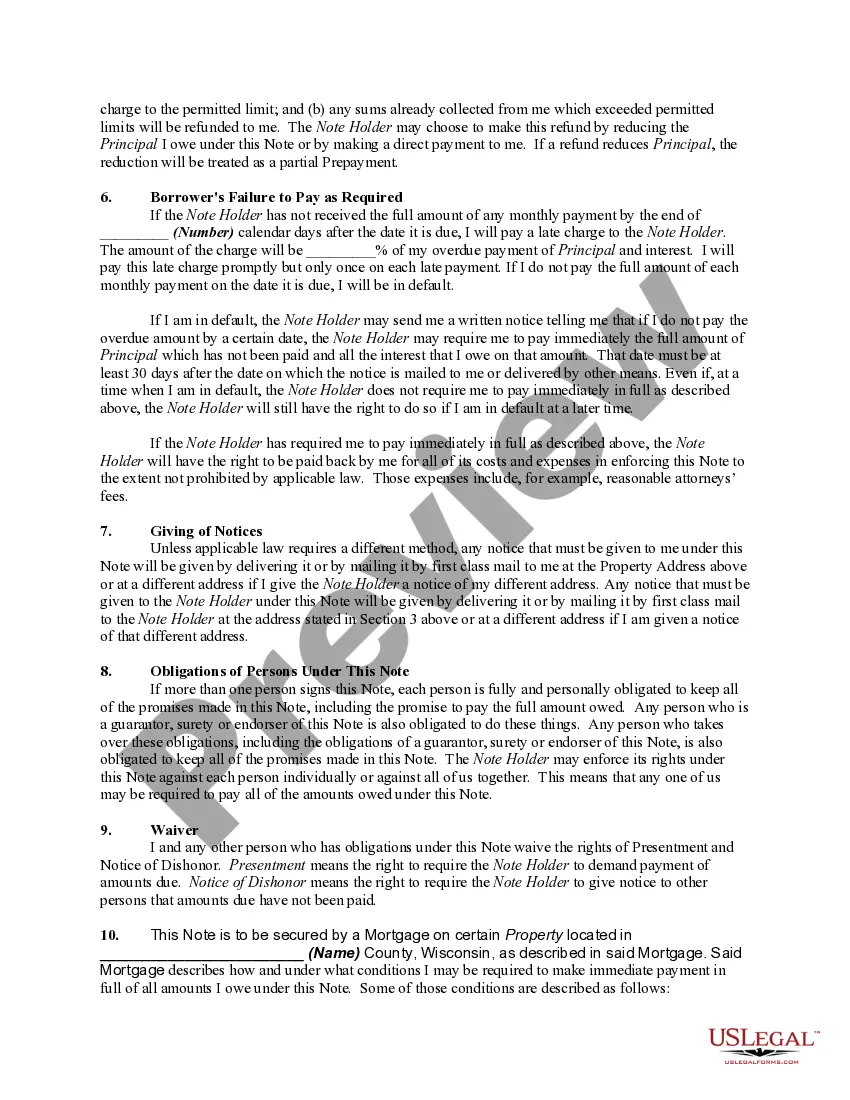

This promissory is a form that can be used in a transaction between one individual and another as opposed to an individual and lender bank.

A mortgage note refers to a legal document that serves as evidence of a debt and is used in real estate transactions involving a bank or other lending institution. It outlines the terms and conditions under which a borrower agrees to repay a loan secured by a mortgage or deed of trust on a property. One common type of mortgage note example with a bank is the fixed-rate mortgage note. This type of note provides for a fixed interest rate on the loan throughout its term, typically ranging from 15 to 30 years. Borrowers benefit from knowing exactly what their monthly payments will be, thereby providing stability and predictability. Another type of mortgage note example is the adjustable-rate mortgage (ARM) note. Unlike the fixed-rate mortgage, the interest rate on an ARM note can change periodically, typically after a certain initial fixed-rate period. This change is usually based on a benchmark index, such as the US Prime Rate, and is accompanied by specific interest rate adjustment intervals and caps to limit drastic fluctuations. ARM's offer initial lower interest rates but entail increased risk due to potential rate adjustments in the future. Furthermore, an interest-only mortgage note example might be issued by a bank. With this type of note, borrowers are only required to pay the interest on the loan for a set period, usually 5 to 10 years. After the interest-only period expires, borrowers must begin paying both the principal and interest, resulting in higher monthly payments. In the case of a balloon mortgage note example, borrowers agree to make smaller monthly payments throughout the term; however, at the end of the loan term, a large final payment, or "balloon payment," is due. This type of mortgage is often used by borrowers who anticipate refinancing or selling the property before the balloon payment becomes due. Furthermore, there are various other mortgage note types available, such as government-backed mortgages or adjustable-rate mortgages indexed to specific rates, such as the London Interbank Offered Rate (LIBOR). When entering into a mortgage note agreement with a bank, it is essential to carefully review and understand the terms and conditions, including information about interest rates, payment schedules, and potential penalties for late payments or defaults. Borrowers should also consult with a qualified professional, such as a real estate attorney or financial advisor, to ensure a thorough understanding and to make informed decisions regarding their mortgage.