Illinois Closing Statement

What this document covers

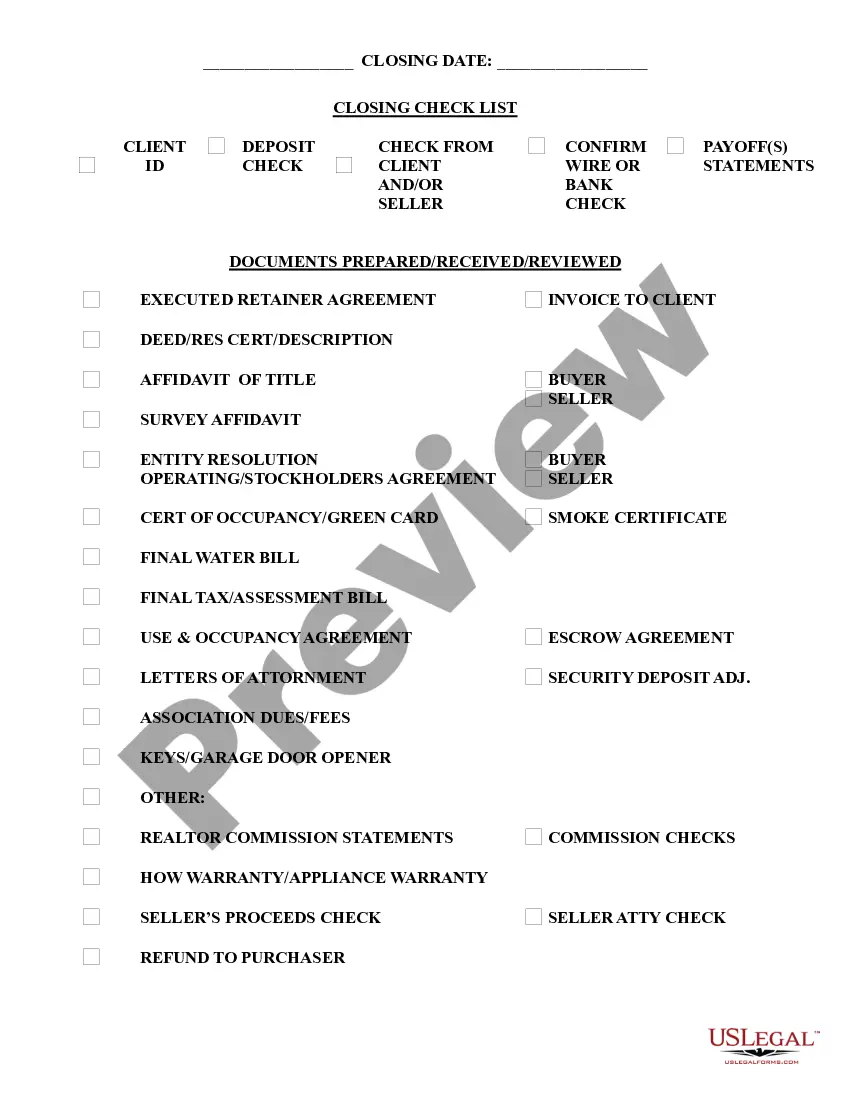

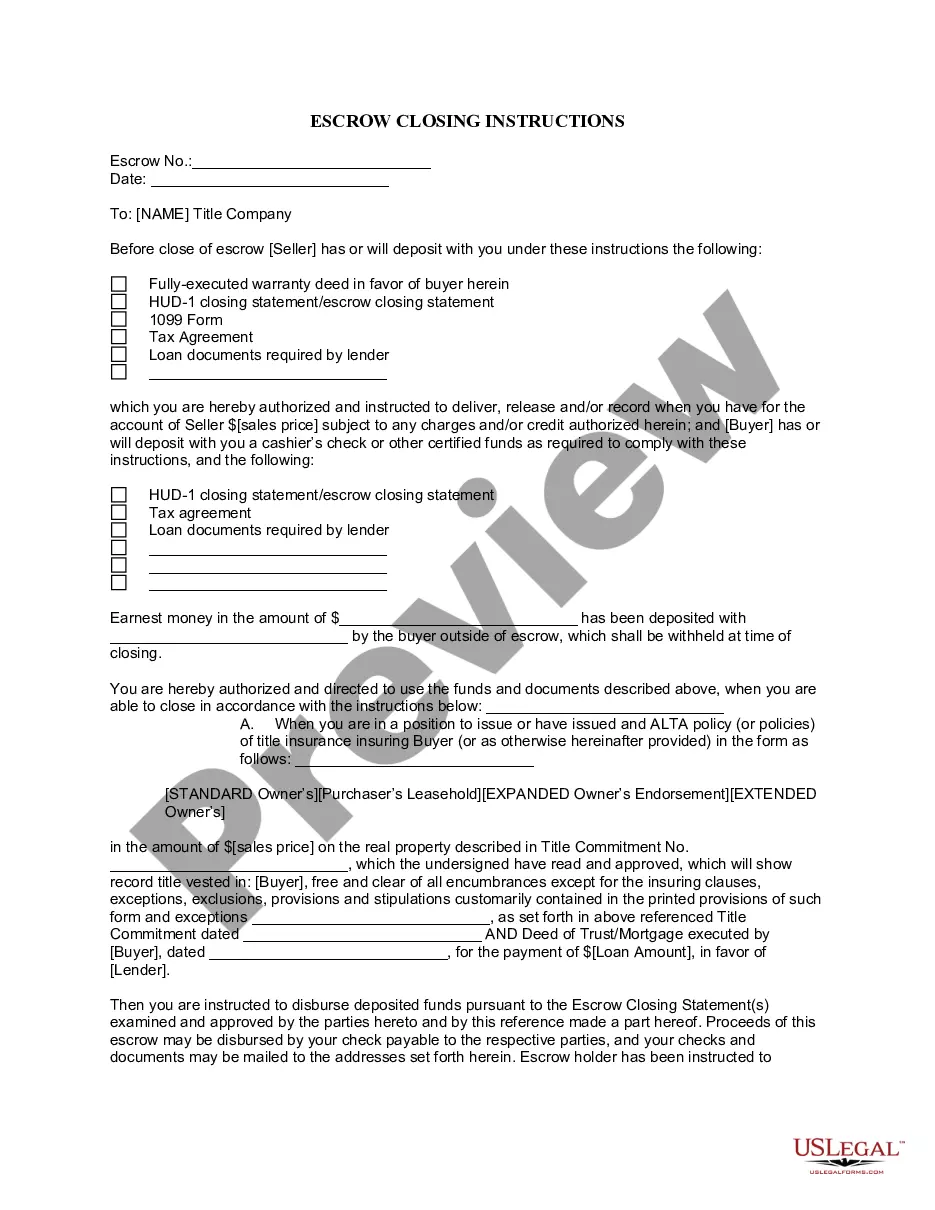

The Closing Statement is a critical document used in real estate transactions, particularly in cash sales or owner-financed deals. This form serves as a detailed settlement statement that outlines all financial aspects of the transaction, including both the buyer's and seller's expenses. It is verified and signed by both parties, ensuring transparency and accountability throughout the closing process.

Main sections of this form

- Balance section: details the financial standing before and after expenses are accounted for.

- Expense breakdown: includes various costs such as title search, recording fees, attorney fees, notary fees, and survey costs.

- Adjustments section: outlines adjustments for taxes or other fees that must be prorated between the buyer and seller.

- Certification statements: sections for both seller's and buyer's signatures to verify the accuracy of the contents.

- Total amounts: summarizes total expenses and balances due or from each party.

When to use this document

Use the Closing Statement when finalizing a real estate transaction. It is essential in scenarios such as cash sales where no mortgage is involved or in situations where owner financing is provided. By completing this form, both buyer and seller can ensure that all financial obligations are met before the property officially changes hands.

Intended users of this form

- Real estate agents involved in transactions.

- Buyers purchasing property through cash or owner financing.

- Sellers transferring ownership of real estate.

- Attorneys representing parties in real estate transactions.

How to complete this form

- Identify the parties involved in the transaction: include the names of the buyer(s) and seller(s).

- Specify the property details: describe the property being sold, including address or parcel number.

- List all applicable expenses: fill in the relevant costs such as title search, recording fees, and attorney fees.

- Complete the adjustments section: detail any prorated taxes and other adjustments that affect the final balance.

- Obtain signatures: ensure that both buyer and seller sign the form to certify its accuracy.

Is notarization required?

This form usually doesn’t need to be notarized. However, local laws or specific transactions may require it. Our online notarization service, powered by Notarize, lets you complete it remotely through a secure video session, available 24/7.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes to avoid

- Failing to include all necessary expenses, leading to incomplete financial disclosure.

- Not obtaining signatures from both parties, which can invalidate the form.

- Entering incorrect property details, causing potential legal issues.

- Neglecting to calculate adjustments accurately, resulting in disputes.

Why complete this form online

- Convenience: download the form immediately and complete it at your own pace.

- Editability: easily customize the form to fit your transaction specifics.

- Reliability: forms are drafted by licensed attorneys to ensure legal compliance.

- Accessibility: use the online form anytime, allowing for timely completion.

Summary of main points

- The Closing Statement is essential for documenting financial details in real estate transactions.

- Both parties must sign the form for it to be valid and enforceable.

- Ensure all expenses and adjustments are accounted for to avoid future disputes.

- Review state-specific requirements to ensure proper legal compliance.

Looking for another form?

Form popularity

FAQ

The settlement statement is prepared by an impartial third party to the transaction, usually an officer with the title or escrow company that performs the closing. In California, both the buyer and the seller sign the HUD-1 settlement statement at closing.

Although different people use different terms, the "closing" or the "settlement" refers to the same finalization of your home purchase. At the closing or settlement date, the seller receives the sale proceeds, and the buyer pays any required expenses to close the transaction, known as closing costs.

The seller's closing statement is an itemized list of fees and credits that shows your net profits as the seller, and summarizes the finances of the entire transaction.

A closing statement is a document that records the details of a financial transaction. A home buyer who finances the purchase will receive a closing statement from the bank, while the home seller will receive one from the real estate agent who handled the sale.

Closing costs are all of the fees and expenses associated with the closing or settlement of a real estate transaction, and they can vary dramatically. The buyer typically pays the closing costs, while other costs are usually the responsibility of the seller.

It outlines the final terms and costs of the mortgage. It's one of the most important pieces of paperwork you'll receive, so check it over carefully. In August 2015, under the direction of the Consumer Financial Protection Bureau (CFPB), the Closing Disclosure Form replaced the HUD-1 settlement statement.

A closing agent prepares the closing statement, which is settlement sheet. It's a comprehensive list of every expense that the buyer and seller must pay to complete the real estate transaction. Fees listed on this sheet include commissions, mortgage insurance, and property tax deposits.

A mortgage closing disclosure is a type of standard settlement statement that is formulated and regulated for the mortgage lending market. The HUD-1 settlement statement is a type of closing statement used in reverse mortgages.

The attorney is responsible for preparing all necessary closing documents, scheduling the closing, explaining all necessary closing documents and having them properly executed and recorded. You will receive copies of most closing documents, including an itemized record of all money paid by you on your behalf.