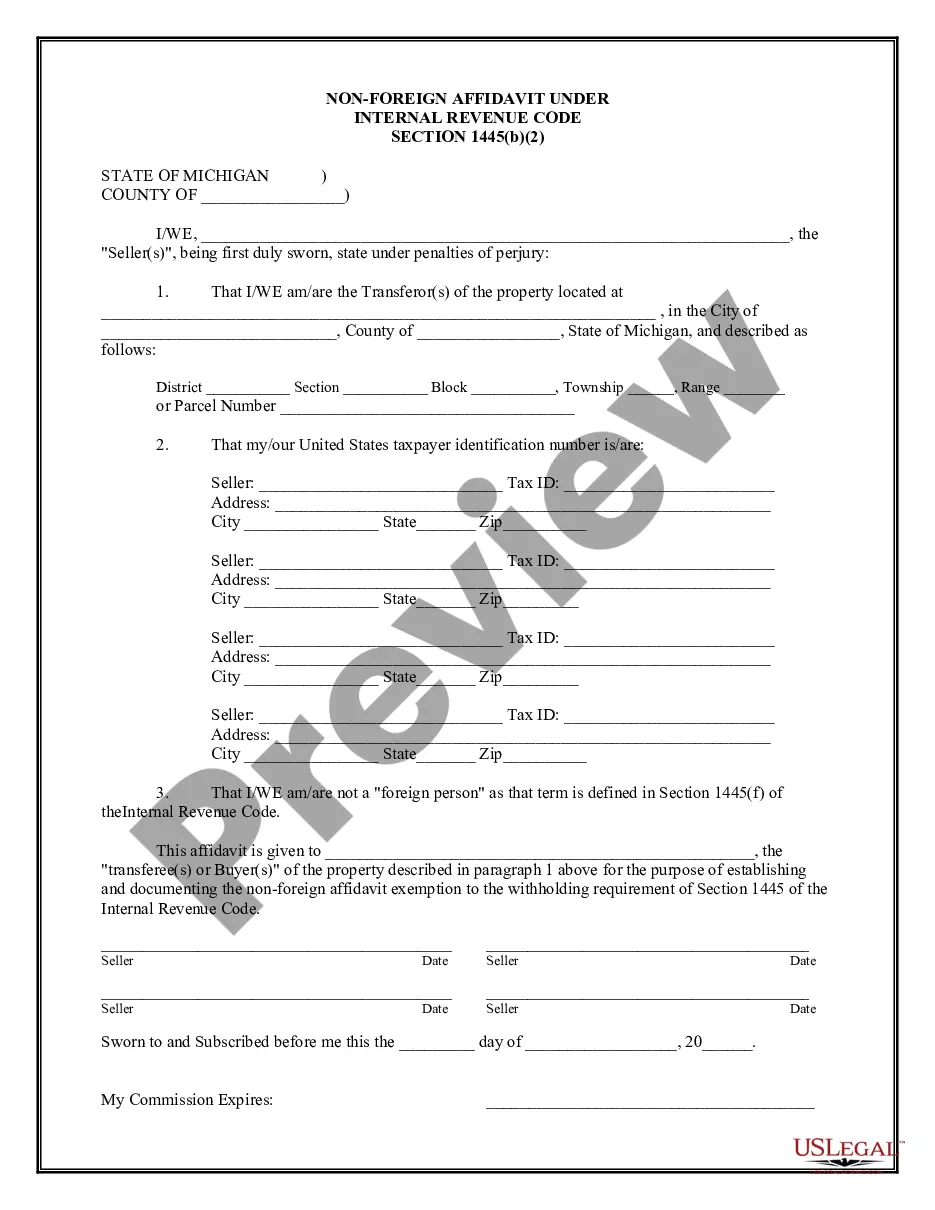

Michigan Non-Foreign Affidavit Under IRC 1445

Description

How to fill out Michigan Non-Foreign Affidavit Under IRC 1445?

Get any template from 85,000 legal documents including Michigan Non-Foreign Affidavit Under IRC 1445 online with US Legal Forms. Every template is drafted and updated by state-accredited lawyers.

If you have a subscription, log in. When you are on the form’s page, click on the Download button and go to My Forms to access it.

In case you have not subscribed yet, follow the tips below:

- Check the state-specific requirements for the Michigan Non-Foreign Affidavit Under IRC 1445 you need to use.

- Look through description and preview the sample.

- Once you are confident the sample is what you need, click on Buy Now.

- Choose a subscription plan that works well for your budget.

- Create a personal account.

- Pay out in one of two suitable ways: by card or via PayPal.

- Choose a format to download the document in; two options are available (PDF or Word).

- Download the file to the My Forms tab.

- Once your reusable template is downloaded, print it out or save it to your gadget.

With US Legal Forms, you’ll always have immediate access to the appropriate downloadable template. The platform gives you access to forms and divides them into categories to simplify your search. Use US Legal Forms to obtain your Michigan Non-Foreign Affidavit Under IRC 1445 fast and easy.

Form popularity

FAQ

The only other way to avoid FIRPTA is via a withholding certificate. If FIRPTA withholding exceeds the maximum tax liability realized on the sale of the real property, sellers can appeal to the IRS for a lower withholding amount.

FIRPTA is a tax law that imposes U.S. income tax on foreign persons selling U.S. real estate. Under FIRPTA, if you buy U.S. real estate from a foreign person, you may be required to withhold 10% of the amount realized from the sale.Along with the form, you submit 10% withholding.

FIRPTA Exemptions The sales price is $300,000 or less, and. The buyer signs affidavit at or before closing stating they intend to use property for personal purposes for at least 50% of time property occupied for the each of the first two 12 month periods immediately after closing.

The disposition of a U.S. real property interest by a foreign person (the transferor) is subject to income tax withholding (IRC section 1445).Withholding is required on certain distributions and other transactions by domestic or foreign corporations, partnerships, trusts, and estates.

1445 provides that when a sale of a U.S. real property interest is made by a foreign person, the buyer is required to deduct and withhold a tax equal to ten percent of the amount realized from the sale of property. An exemption to this rule is a foreign residence affidavit, also called non-foreign person affidavit.

CERTIFICATE OF NON FOREIGN STATUS. Section 1445 of the Internal Revenue Code provides that a transferee (buyer) of a U.S. real property interest must withhold tax if the transferor (seller) is a foreign person.

A: The buyer must agree to sign an affidavit stating that the purchase price is under $300,000 and the buyer intends to occupy. The buyer may choose not to sign the form, in which case withholding must be done.