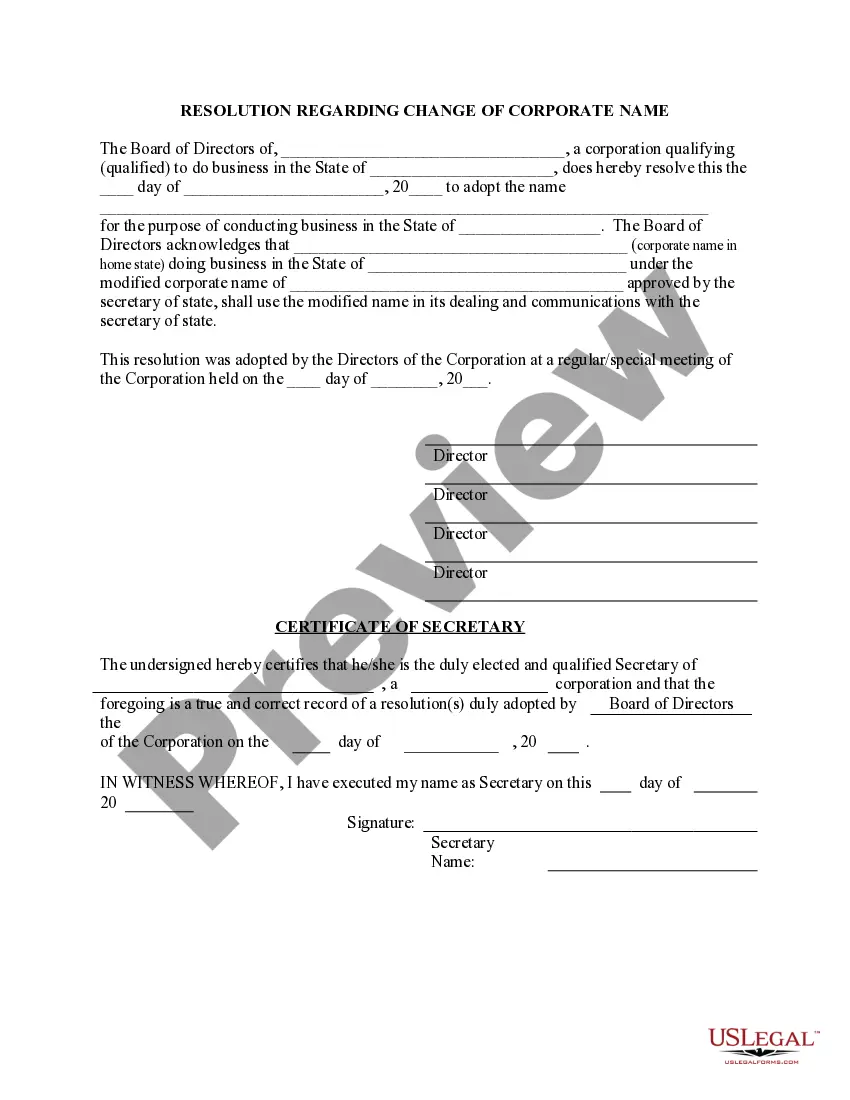

Alaska Final Accounting and Proposed Distribution is the process of determining and allocating the assets of an estate, trust, or decedent’s estate, according to the laws of the state of Alaska. This process includes a final accounting of the estate, the identification of any creditors or heirs, and the division of the assets according to the terms of the will or the applicable state laws. There are two types of Alaska Final Accounting and Proposed Distribution: Formal Accounting and Informal Accounting. Formal Accounting is used when there is a will in place or other legal documents that need to be taken into consideration. This type of accounting is more formal and requires the appointment of an administrator or executor to oversee the process. Informal Accounting is used when there is no will or other legal documents in place. This type of accounting is less formal and is usually handled by the family of the decedent. In either type of accounting, a detailed record of all assets and liabilities of the estate must be established. This includes a list of all creditors, their claims, and any assets that need to be distributed. After the accounting is complete, the assets are then distributed according to the will, the applicable state laws, or other legal documents. Any remaining assets are then distributed to the heirs or creditors according to the terms of the will or applicable state laws.

Alaska Final Accounting and Proposed Distribution is the process of determining and allocating the assets of an estate, trust, or decedent’s estate, according to the laws of the state of Alaska. This process includes a final accounting of the estate, the identification of any creditors or heirs, and the division of the assets according to the terms of the will or the applicable state laws. There are two types of Alaska Final Accounting and Proposed Distribution: Formal Accounting and Informal Accounting. Formal Accounting is used when there is a will in place or other legal documents that need to be taken into consideration. This type of accounting is more formal and requires the appointment of an administrator or executor to oversee the process. Informal Accounting is used when there is no will or other legal documents in place. This type of accounting is less formal and is usually handled by the family of the decedent. In either type of accounting, a detailed record of all assets and liabilities of the estate must be established. This includes a list of all creditors, their claims, and any assets that need to be distributed. After the accounting is complete, the assets are then distributed according to the will, the applicable state laws, or other legal documents. Any remaining assets are then distributed to the heirs or creditors according to the terms of the will or applicable state laws.