A deed of trust is a document which pledges real property to secure a loan, used instead of a mortgage in certain states. A deed of trust involves a third party called a trustee, usually an attorney of officer of the lender, who acts on behalf of the lender. When you sign a deed of trust, you in effect are giving a trustee title to the property, but you hold the rights and privileges to use and live in or on the property. If the loan becomes delinquent the beneficiary can file a notice of default and, if the loan is not brought current, can demand that the trustee begin foreclosure on the property so that the beneficiary (lender) may either be paid or obtain title. Unlike a mortgage, a deed of trust also gives the trustee the right to foreclose on your property without taking you to court first.

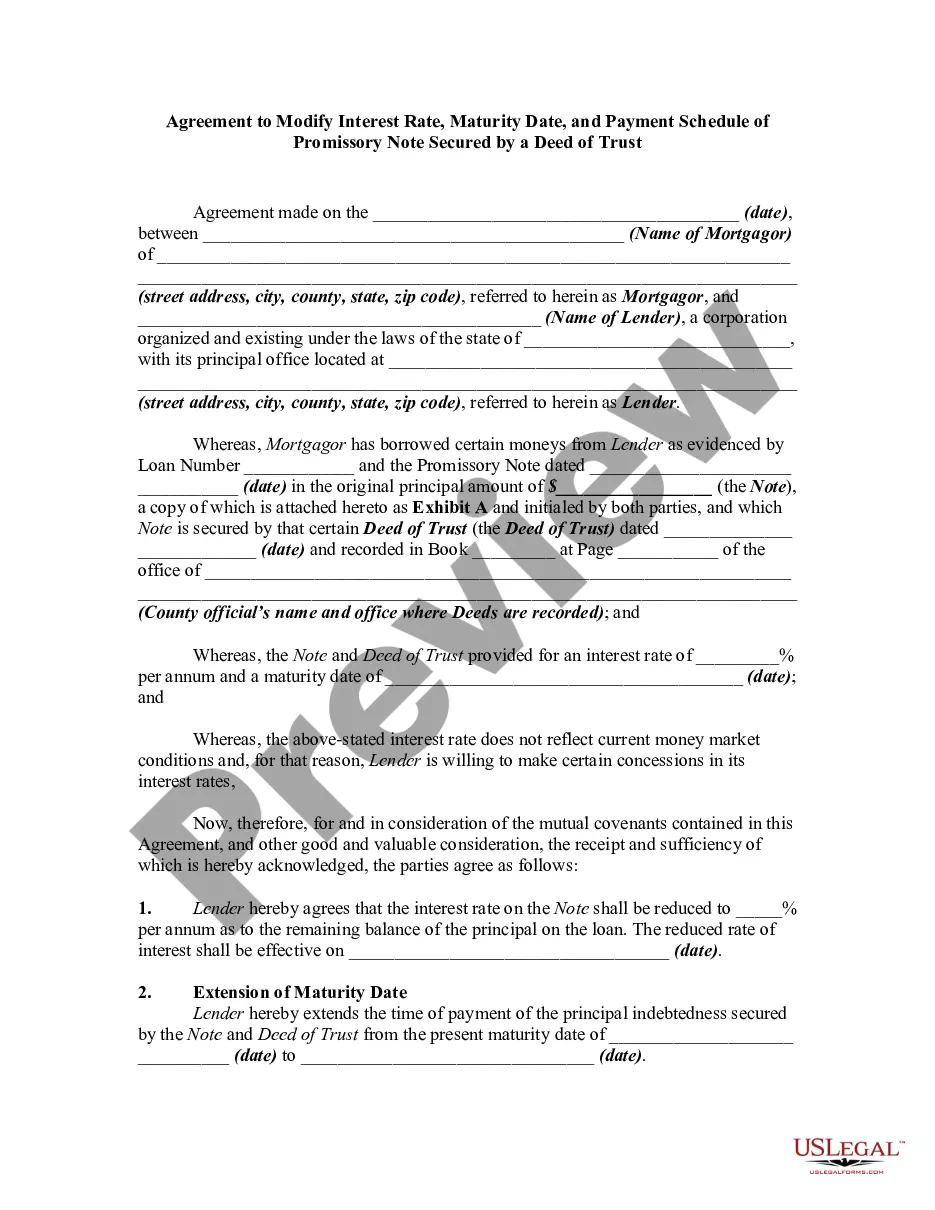

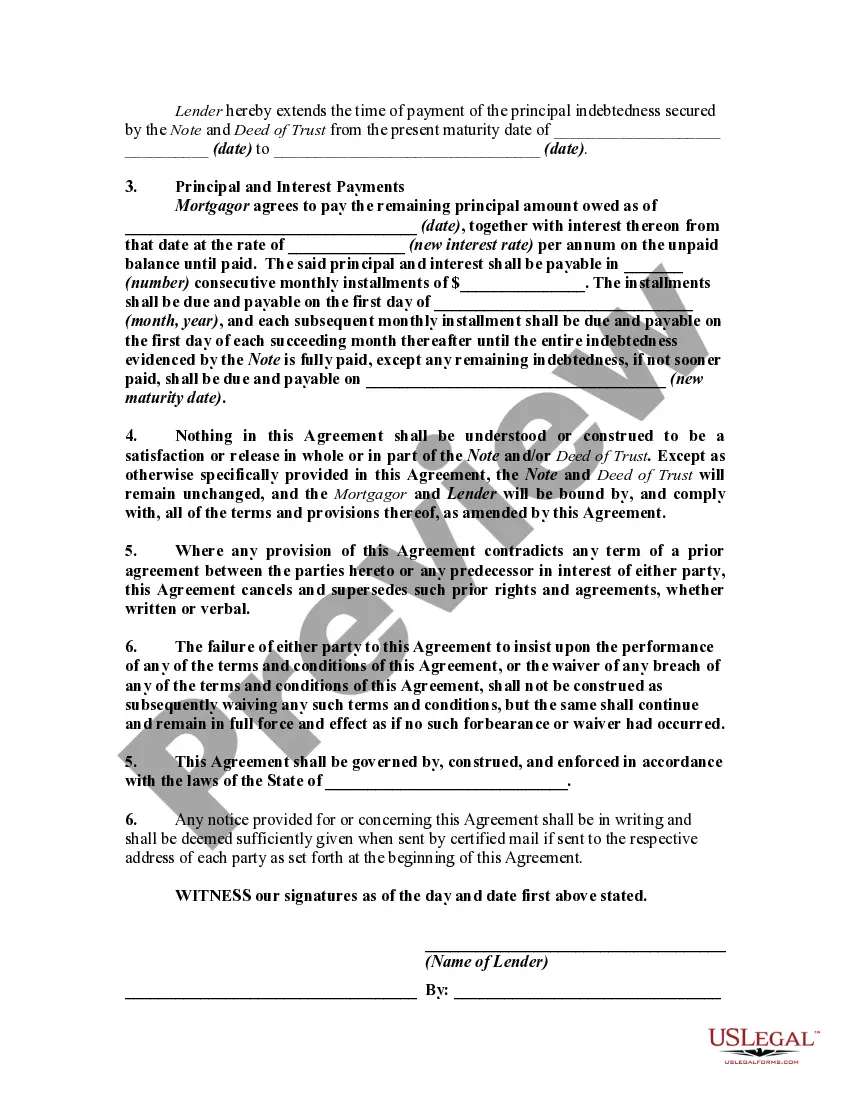

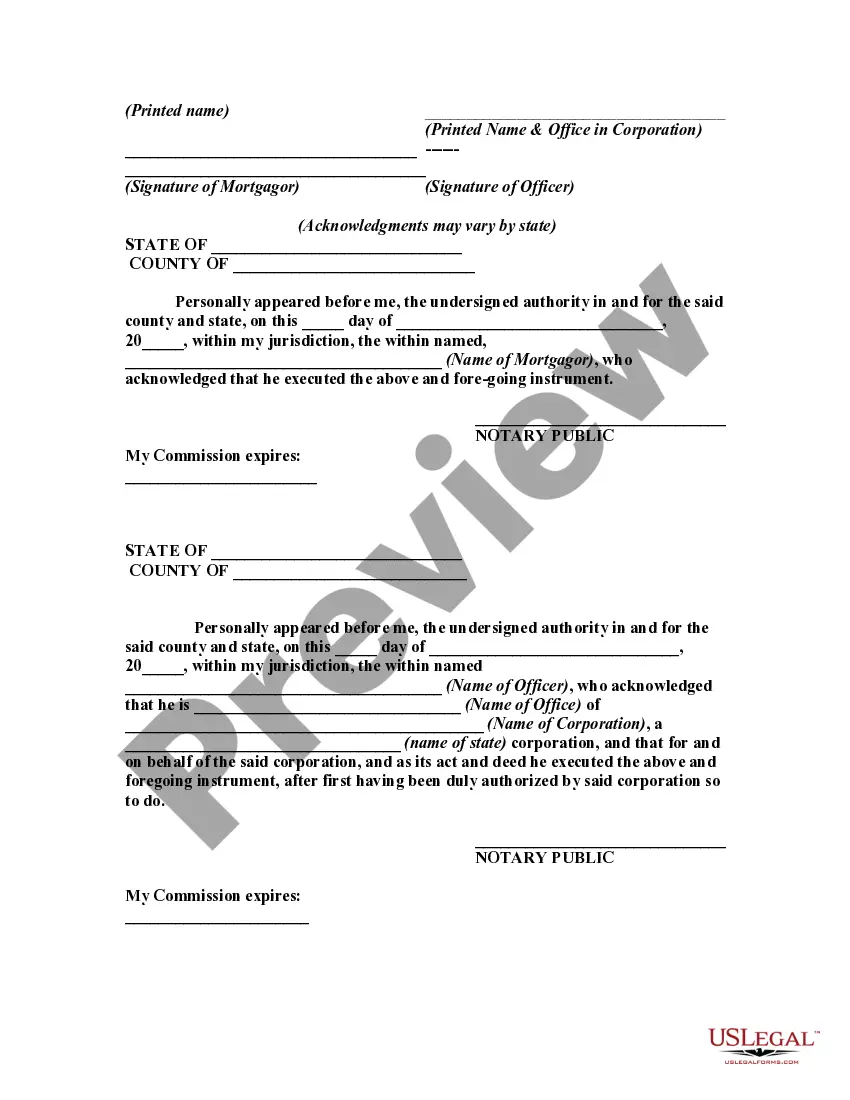

An agreement modifying a promissory note and deed of trust should be signed by both parties to the transaction and recorded in the office of the register of deeds and mortgages where the original deed of trust was recorded.

Alaska Agreement to Change or Modify Interest Rate, Maturity Date, and Payment Schedule of Promissory Note Secured by a Deed of Trust In Alaska, an Agreement to Change or Modify Interest Rate, Maturity Date, and Payment Schedule of a Promissory Note Secured by a Deed of Trust allows the borrower and lender to alter certain terms and conditions of the original loan agreement. This agreement can be utilized in various situations where the borrower requires adjustments to the interest rate, maturity date, or payment schedule to better suit their financial circumstances. Key aspects of this agreement may include: 1. Interest Rate Modification: This type of modification allows the borrower to negotiate a new interest rate for the outstanding loan balance. This can be beneficial if the borrower wants to take advantage of prevailing lower interest rates or if they are facing financial difficulties and need a reduced rate to make the loan more affordable. 2. Maturity Date Extension: If the borrower is struggling to repay the loan within the initially agreed upon timeframe, an extension of the maturity date can be negotiated in this agreement. This provides the borrower with additional time to repay the loan, potentially reducing monthly payment amounts and easing financial strain. 3. Payment Schedule Adjustment: The agreement also enables the borrower and lender to modify the payment schedule. This can include changes to the frequency of payments (e.g., from monthly to quarterly), alterations in the amount of each payment, or restructuring the repayment plan to better align with the borrower's financial capabilities. 4. Additional Terms and Conditions: The Alaska Agreement to Change or Modify Interest Rate, Maturity Date, and Payment Schedule of Promissory Note Secured by a Deed of Trust may involve other adjustments depending on the specific circumstances. This could include changes to the late payment fees, prepayment penalties, or any other provisions that need to be updated in line with the negotiated modifications. It is essential to note that this description outlines the general concept and potential modifications available in an Alaska Agreement to Change or Modify Interest Rate, Maturity Date, and Payment Schedule of a Promissory Note Secured by a Deed of Trust. The specific terms and conditions of such an agreement can vary depending on the lender's policies, borrower's needs, and the details of the underlying loan. It is advisable for parties involved to consult legal professionals or financial advisors to ensure the agreement accurately reflects their intentions and protects their interests.Alaska Agreement to Change or Modify Interest Rate, Maturity Date, and Payment Schedule of Promissory Note Secured by a Deed of Trust In Alaska, an Agreement to Change or Modify Interest Rate, Maturity Date, and Payment Schedule of a Promissory Note Secured by a Deed of Trust allows the borrower and lender to alter certain terms and conditions of the original loan agreement. This agreement can be utilized in various situations where the borrower requires adjustments to the interest rate, maturity date, or payment schedule to better suit their financial circumstances. Key aspects of this agreement may include: 1. Interest Rate Modification: This type of modification allows the borrower to negotiate a new interest rate for the outstanding loan balance. This can be beneficial if the borrower wants to take advantage of prevailing lower interest rates or if they are facing financial difficulties and need a reduced rate to make the loan more affordable. 2. Maturity Date Extension: If the borrower is struggling to repay the loan within the initially agreed upon timeframe, an extension of the maturity date can be negotiated in this agreement. This provides the borrower with additional time to repay the loan, potentially reducing monthly payment amounts and easing financial strain. 3. Payment Schedule Adjustment: The agreement also enables the borrower and lender to modify the payment schedule. This can include changes to the frequency of payments (e.g., from monthly to quarterly), alterations in the amount of each payment, or restructuring the repayment plan to better align with the borrower's financial capabilities. 4. Additional Terms and Conditions: The Alaska Agreement to Change or Modify Interest Rate, Maturity Date, and Payment Schedule of Promissory Note Secured by a Deed of Trust may involve other adjustments depending on the specific circumstances. This could include changes to the late payment fees, prepayment penalties, or any other provisions that need to be updated in line with the negotiated modifications. It is essential to note that this description outlines the general concept and potential modifications available in an Alaska Agreement to Change or Modify Interest Rate, Maturity Date, and Payment Schedule of a Promissory Note Secured by a Deed of Trust. The specific terms and conditions of such an agreement can vary depending on the lender's policies, borrower's needs, and the details of the underlying loan. It is advisable for parties involved to consult legal professionals or financial advisors to ensure the agreement accurately reflects their intentions and protects their interests.