This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

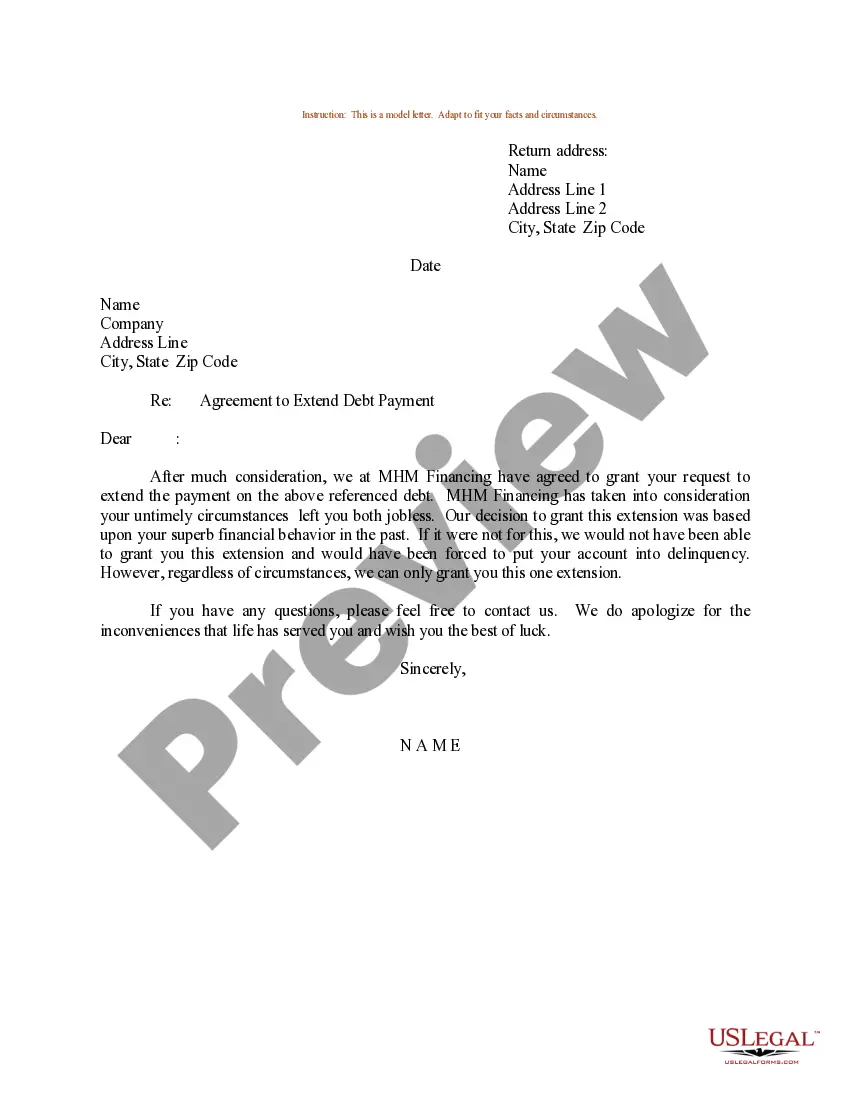

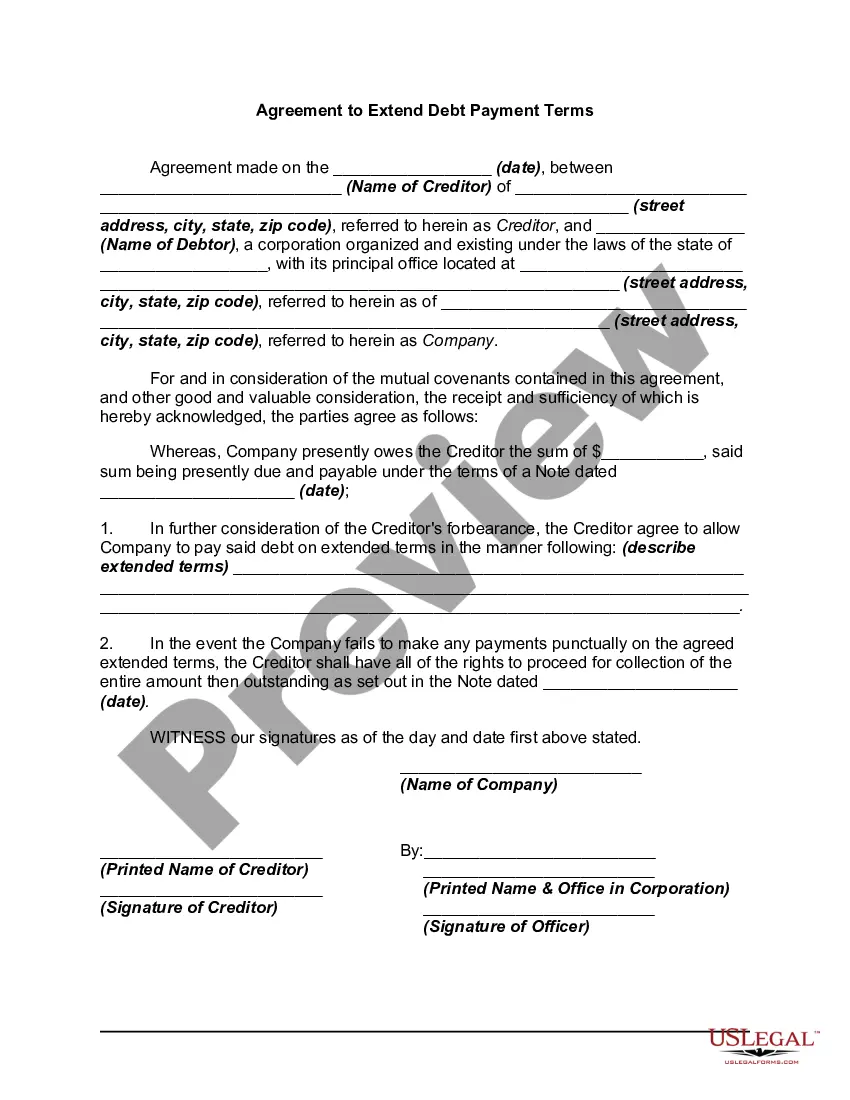

Alaska Agreement to Extend Debt Payment

Instant download

Description

Free preview

How to fill out Agreement To Extend Debt Payment?

Locating the appropriate authentic document template can be a challenge.

Of course, there are numerous formats accessible online, but how can you find the genuine template you require.

Utilize the US Legal Forms platform. The service offers a vast array of templates, such as the Alaska Agreement to Extend Debt Payment, which you can use for business and personal purposes.

You can browse the template using the Review button and read the template description to confirm this is indeed the right one for you.

- All of the forms are verified by professionals and comply with federal and state regulations.

- If you are currently registered, Log In to your account and click the Obtain button to download the Alaska Agreement to Extend Debt Payment.

- Use your account to view the legal forms you have previously acquired.

- Navigate to the My documents section of your account and obtain another copy of the document you require.

- If you are a new user of US Legal Forms, here are some simple steps for you to follow.

- First, ensure you have selected the correct template for your jurisdiction/region.

Form popularity

FAQ

Writing a debt payment agreement involves outlining the debt amount, payment terms, and the method of payment. Be clear and detailed to ensure both parties understand their responsibilities. Utilizing an Alaska Agreement to Extend Debt Payment template can simplify this process and ensure all necessary elements are included. Our platform offers customizable templates to support you in creating an effective agreement.

In Alaska, collectors can actively pursue payment for a debt for up to three years following the last payment or acknowledgment of the debt. Once this period passes, the debt becomes time-barred, meaning the creditor cannot sue you for payment. Knowing this can help you strategically manage your financial obligations and explore options like an Alaska Agreement to Extend Debt Payment. Our platform provides templates to assist in crafting personalized agreements.

Debt collectors can pursue payments for debts that are within the statute of limitations, which is three years in Alaska. This means they can legally attempt to collect debts incurred up to three years prior. It’s important to understand these timelines when entering into an Alaska Agreement to Extend Debt Payment to protect your rights. Engaging with our resources can help clarify any concerns you may have.

In Alaska, a debt can become uncollectible after three years due to the statute of limitations. This means creditors cannot take legal action to recover the debt after this period. Understanding the laws around debt collection is crucial, especially when considering an Alaska Agreement to Extend Debt Payment. Should you find yourself in a situation requiring legal advice, our platform offers resources and templates to assist you.

Yes, like many states, Alaska faces financial obligations that contribute to its overall debt. One of the tools available for managing such financial challenges is the Alaska Agreement to Extend Debt Payment. This agreement allows the state to negotiate payment extensions, providing relief and flexibility in managing its finances. Understanding how the Alaska Agreement to Extend Debt Payment works can help you grasp the state's fiscal strategies.

In Alaska, the statute of limitations for debt collection is generally three years for most debts, including written contracts and open accounts. This timeline means creditors must initiate legal actions within this period to collect unpaid debt. Understanding the implications of the Alaska Agreement to Extend Debt Payment can help debtors navigate their obligations and protect their rights.

To write a debt agreement, start by clearly stating the parties involved. Next, include the amount of debt, the payment terms, and any interest rates. Also, outline the consequences if the terms are not met. Utilizing an Alaska Agreement to Extend Debt Payment can simplify this process and ensure all necessary legal requirements are met.

Typically, offering between 40% to 60% of your total debt may result in a successful negotiation for a settlement. However, this can vary based on your specific situation and the creditor's willingness to negotiate. An Alaska Agreement to Extend Debt Payment can provide you with a framework to propose a fair settlement, showing your commitment to resolving the debt.

To sue someone in Alaska, you must file a complaint in the appropriate court and serve the defendant with the documents. Make sure to gather all evidence and documentation related to your case. If you're dealing with debt collection, consider discussing your options with a legal expert and exploring an Alaska Agreement to Extend Debt Payment before pursuing legal action.

A debt agreement can be a good idea as it provides a clear plan for settling your debts while potentially reducing stress. It allows for honest communication between you and your creditors, which can lead to better terms. Utilizing an Alaska Agreement to Extend Debt Payment can help you regain control over your financial situation and avoid more severe repercussions.