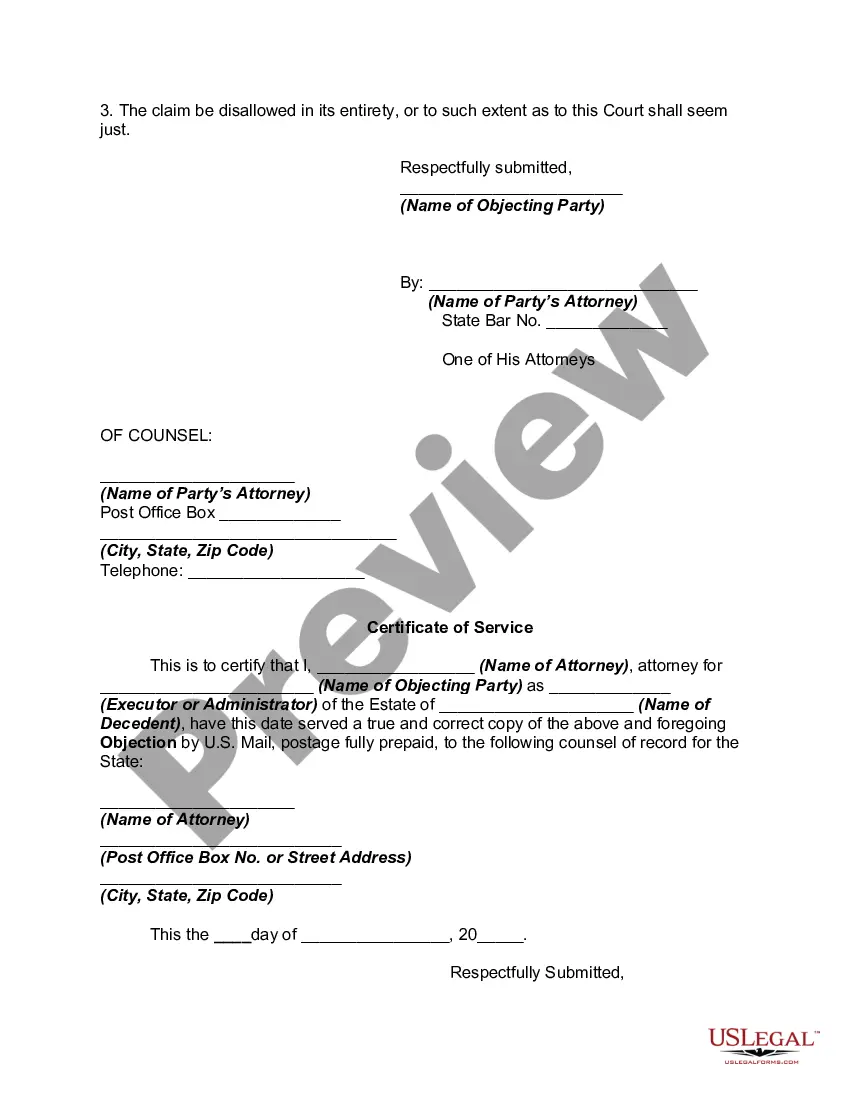

Any interested party in an estate of a decedent generally has the right to make objections to the accounting of the executor, the compensation paid or

proposed to be paid, or the proposed distribution of assets. Such objections must be filed within within a certain period of time from the date of service of the Petition for approval of the accounting.

This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

Alaska Objection to Allowed Claim in Accounting refers to a specific type of objection raised by the state of Alaska regarding an allowed claim in accounting. This objection arises when a claimant requests reimbursement or payment from the state but encounters opposition due to certain discrepancies or issues identified by Alaska's accounting department. Such objections can occur in various scenarios and can be divided into different types based on the nature of the claim or the reasons behind the objection. One type of Alaska Objection to Allowed Claim in Accounting is related to discrepancies or inconsistencies in the claimant's financial documentation. If the claimant fails to provide accurate and comprehensive financial records, the accounting department may object to the claim, as it hinders their ability to assess the validity of the request and ensure appropriate use of public funds. In such cases, the objection highlights the need for the claimant to provide more substantial evidence and clarification regarding their financial transactions. Another type of objection could be due to the failure of the claimant to meet specific legal or technical requirements set by Alaska state law. For instance, if the claimant does not fulfill the necessary criteria or fails to file their claim within the designated timeframe, the accounting department may object to the claim on procedural grounds. This type of objection reinforces the importance of adhering to legal obligations and deadlines to ensure smooth processing of claims. Furthermore, an objection may arise when there is suspicion or evidence of fraudulent activity or misrepresentation by the claimant. In such instances, Alaska may object to the claim by pointing out discrepancies, providing evidence of fraud, or highlighting misinterpretation or manipulation of financial data. These objections serve to protect the state's financial interests, prevent any misuse of public funds, and deter fraudulent behavior. In summary, Alaska Objection to Allowed Claim in Accounting refers to objections raised by the state's accounting department regarding a claim. Different types of objections may include discrepancies in financial documentation, failure to meet legal requirements, or suspicion of fraudulent activity. By identifying and addressing these objections, the state of Alaska aims to ensure the integrity of its accounting processes and the proper allocation of public resources.

Alaska Objection to Allowed Claim in Accounting refers to a specific type of objection raised by the state of Alaska regarding an allowed claim in accounting. This objection arises when a claimant requests reimbursement or payment from the state but encounters opposition due to certain discrepancies or issues identified by Alaska's accounting department. Such objections can occur in various scenarios and can be divided into different types based on the nature of the claim or the reasons behind the objection. One type of Alaska Objection to Allowed Claim in Accounting is related to discrepancies or inconsistencies in the claimant's financial documentation. If the claimant fails to provide accurate and comprehensive financial records, the accounting department may object to the claim, as it hinders their ability to assess the validity of the request and ensure appropriate use of public funds. In such cases, the objection highlights the need for the claimant to provide more substantial evidence and clarification regarding their financial transactions. Another type of objection could be due to the failure of the claimant to meet specific legal or technical requirements set by Alaska state law. For instance, if the claimant does not fulfill the necessary criteria or fails to file their claim within the designated timeframe, the accounting department may object to the claim on procedural grounds. This type of objection reinforces the importance of adhering to legal obligations and deadlines to ensure smooth processing of claims. Furthermore, an objection may arise when there is suspicion or evidence of fraudulent activity or misrepresentation by the claimant. In such instances, Alaska may object to the claim by pointing out discrepancies, providing evidence of fraud, or highlighting misinterpretation or manipulation of financial data. These objections serve to protect the state's financial interests, prevent any misuse of public funds, and deter fraudulent behavior. In summary, Alaska Objection to Allowed Claim in Accounting refers to objections raised by the state's accounting department regarding a claim. Different types of objections may include discrepancies in financial documentation, failure to meet legal requirements, or suspicion of fraudulent activity. By identifying and addressing these objections, the state of Alaska aims to ensure the integrity of its accounting processes and the proper allocation of public resources.