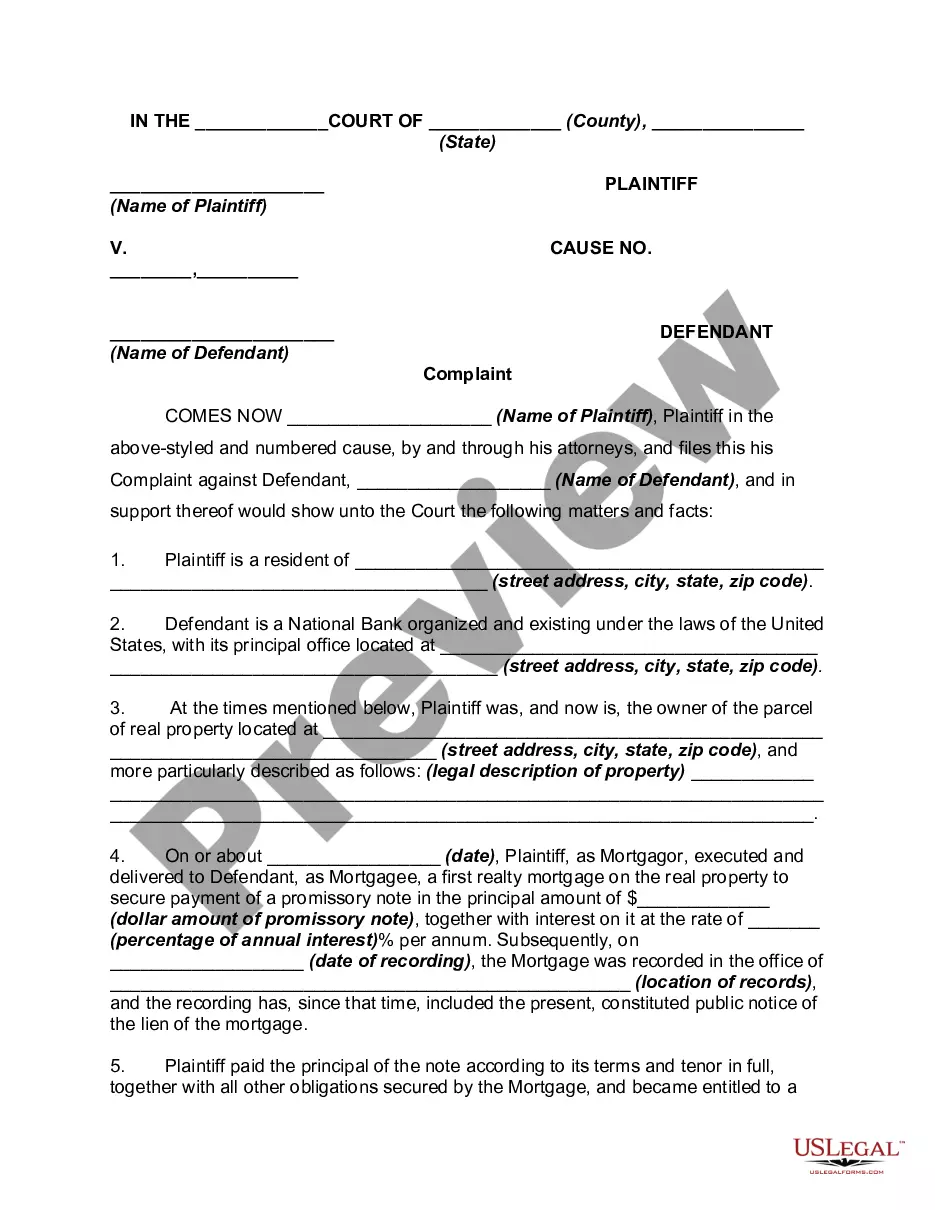

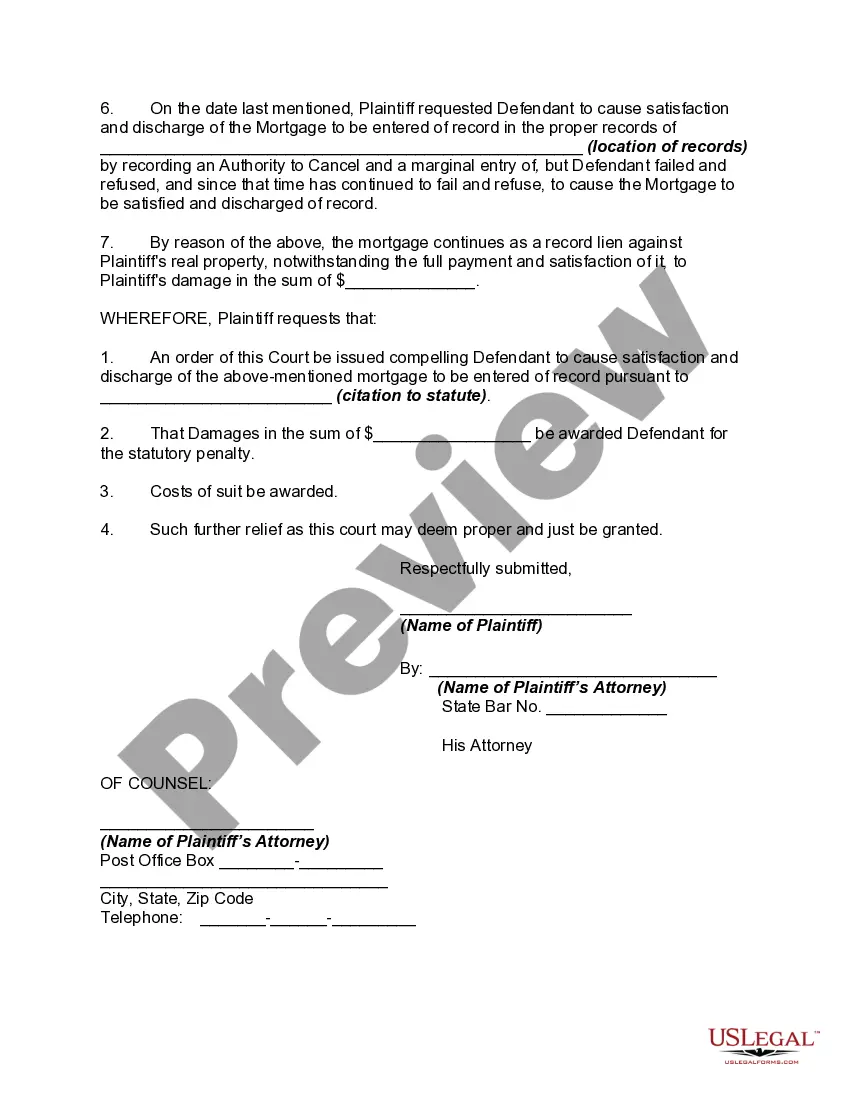

This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

Title: Understanding Alaska Complaints to Compel Mortgagee to Execute and Record Satisfaction and Discharge of Mortgage Introduction: Alaska Complaint to Compel Mortgagee to Execute and Record Satisfaction and Discharge of Mortgage is a legal remedy that homeowners can pursue to enforce the mortgagee's obligation to acknowledge the repayment of a mortgage and release the lien on the property. This comprehensive guide explores the intricacies of this complaint, clarifies its purpose, and highlights different types that may exist. 1. Key Components of an Alaska Complaint to Compel Mortgagee to Execute and Record Satisfaction and Discharge of Mortgage: — Complaint Overview: Gain an understanding of the complaint's purpose and the legal basis for its filing under Alaska's mortgage laws. — Notification of Payment: Detail the obligation of the mortgagee to recognize and acknowledge the borrower's repayment on the mortgage loan. — Mortgagee's Failure to Comply: Discuss the circumstances under which the mortgagee may fail to execute and record satisfaction and discharge of the mortgage despite being legally obligated to do so. — Homeowner's Rights and Legal Remedies: Outline the rights of the homeowner and the remedies available to compel the mortgagee to fulfill their obligations. — Procedural Requirements: Explain the specific steps and formalities involved in initiating an Alaska Complaint to Compel Mortgagee to Execute and Record Satisfaction and Discharge of Mortgage, such as proper notice, jurisdiction, and applicable deadlines. 2. Types of Alaska Complaints to Compel Mortgagee to Execute and Record Satisfaction and Discharge of Mortgage: a) Residential Mortgages: Elaborate on the specific aspects of residential mortgage complaints, including common issues faced by homeowners, such as delays or inaccurate documentation. b) Commercial Mortgages: Discuss the unique challenges and considerations associated with commercial mortgage complaints, emphasizing commercial property owners' particular concerns and interests. c) Multi-Beneficiary Mortgages: Address the complexities that may arise when multiple beneficiaries are involved in a mortgage and the potential variations in filing complaints based on these circumstances. d) Post-Foreclosure and Redemption Period Mortgages: Describe the distinct features and relevant factors that homeowners should be aware of when filing complaints after foreclosure or during the redemption period. Conclusion: Alaska Complaint to Compel Mortgagee to Execute and Record Satisfaction and Discharge of Mortgage empowers homeowners to protect their rights and interests by holding mortgagees accountable for fulfilling their legal obligations. Understanding the nuances of this legal remedy is essential to navigating the complexities of mortgage transactions and ensuring a satisfactory resolution for borrowers. Whether a residential, commercial, or multi-beneficiary mortgage, homeowners can pursue appropriate action when their mortgagees fail to execute and record satisfaction and discharge of the mortgage as required by the law.Title: Understanding Alaska Complaints to Compel Mortgagee to Execute and Record Satisfaction and Discharge of Mortgage Introduction: Alaska Complaint to Compel Mortgagee to Execute and Record Satisfaction and Discharge of Mortgage is a legal remedy that homeowners can pursue to enforce the mortgagee's obligation to acknowledge the repayment of a mortgage and release the lien on the property. This comprehensive guide explores the intricacies of this complaint, clarifies its purpose, and highlights different types that may exist. 1. Key Components of an Alaska Complaint to Compel Mortgagee to Execute and Record Satisfaction and Discharge of Mortgage: — Complaint Overview: Gain an understanding of the complaint's purpose and the legal basis for its filing under Alaska's mortgage laws. — Notification of Payment: Detail the obligation of the mortgagee to recognize and acknowledge the borrower's repayment on the mortgage loan. — Mortgagee's Failure to Comply: Discuss the circumstances under which the mortgagee may fail to execute and record satisfaction and discharge of the mortgage despite being legally obligated to do so. — Homeowner's Rights and Legal Remedies: Outline the rights of the homeowner and the remedies available to compel the mortgagee to fulfill their obligations. — Procedural Requirements: Explain the specific steps and formalities involved in initiating an Alaska Complaint to Compel Mortgagee to Execute and Record Satisfaction and Discharge of Mortgage, such as proper notice, jurisdiction, and applicable deadlines. 2. Types of Alaska Complaints to Compel Mortgagee to Execute and Record Satisfaction and Discharge of Mortgage: a) Residential Mortgages: Elaborate on the specific aspects of residential mortgage complaints, including common issues faced by homeowners, such as delays or inaccurate documentation. b) Commercial Mortgages: Discuss the unique challenges and considerations associated with commercial mortgage complaints, emphasizing commercial property owners' particular concerns and interests. c) Multi-Beneficiary Mortgages: Address the complexities that may arise when multiple beneficiaries are involved in a mortgage and the potential variations in filing complaints based on these circumstances. d) Post-Foreclosure and Redemption Period Mortgages: Describe the distinct features and relevant factors that homeowners should be aware of when filing complaints after foreclosure or during the redemption period. Conclusion: Alaska Complaint to Compel Mortgagee to Execute and Record Satisfaction and Discharge of Mortgage empowers homeowners to protect their rights and interests by holding mortgagees accountable for fulfilling their legal obligations. Understanding the nuances of this legal remedy is essential to navigating the complexities of mortgage transactions and ensuring a satisfactory resolution for borrowers. Whether a residential, commercial, or multi-beneficiary mortgage, homeowners can pursue appropriate action when their mortgagees fail to execute and record satisfaction and discharge of the mortgage as required by the law.