This form is a type of asset-financing arrangement in which a company uses its receivables (money owed by customers) as collateral in a financing agreement. The company receives an amount that is equal to a reduced value of the receivables pledged. The age of the receivables have a large effect on the amount a company will receive. The older the receivables, the less the company can expect.

This type of financing helps companies free up capital that is stuck in accounts receivables. Accounts receivable financing transfers the default risk associated with the accounts receivables to the financing company. This transfer of risk can help the company using the financing to shift focus from trying to collect receivables to current business activities.

This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

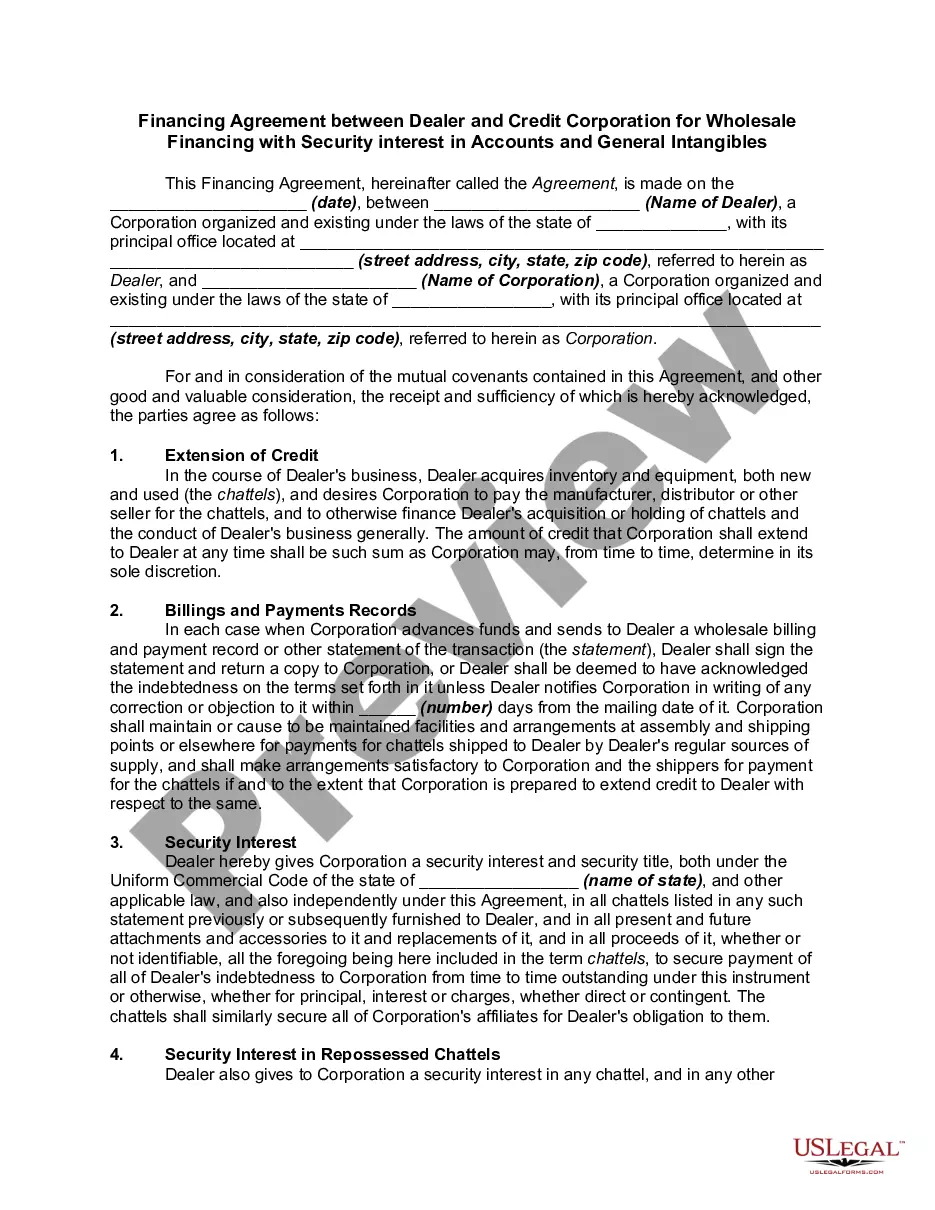

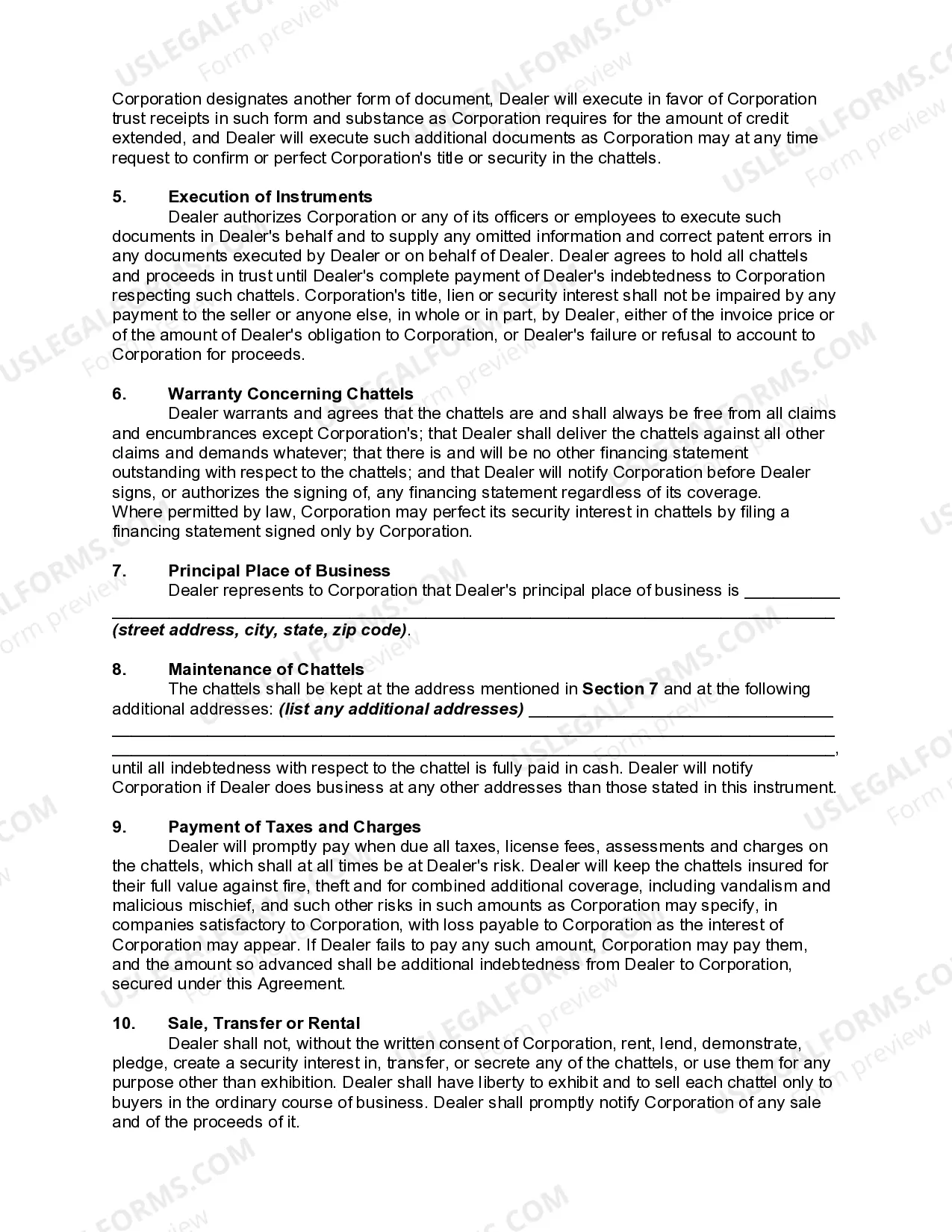

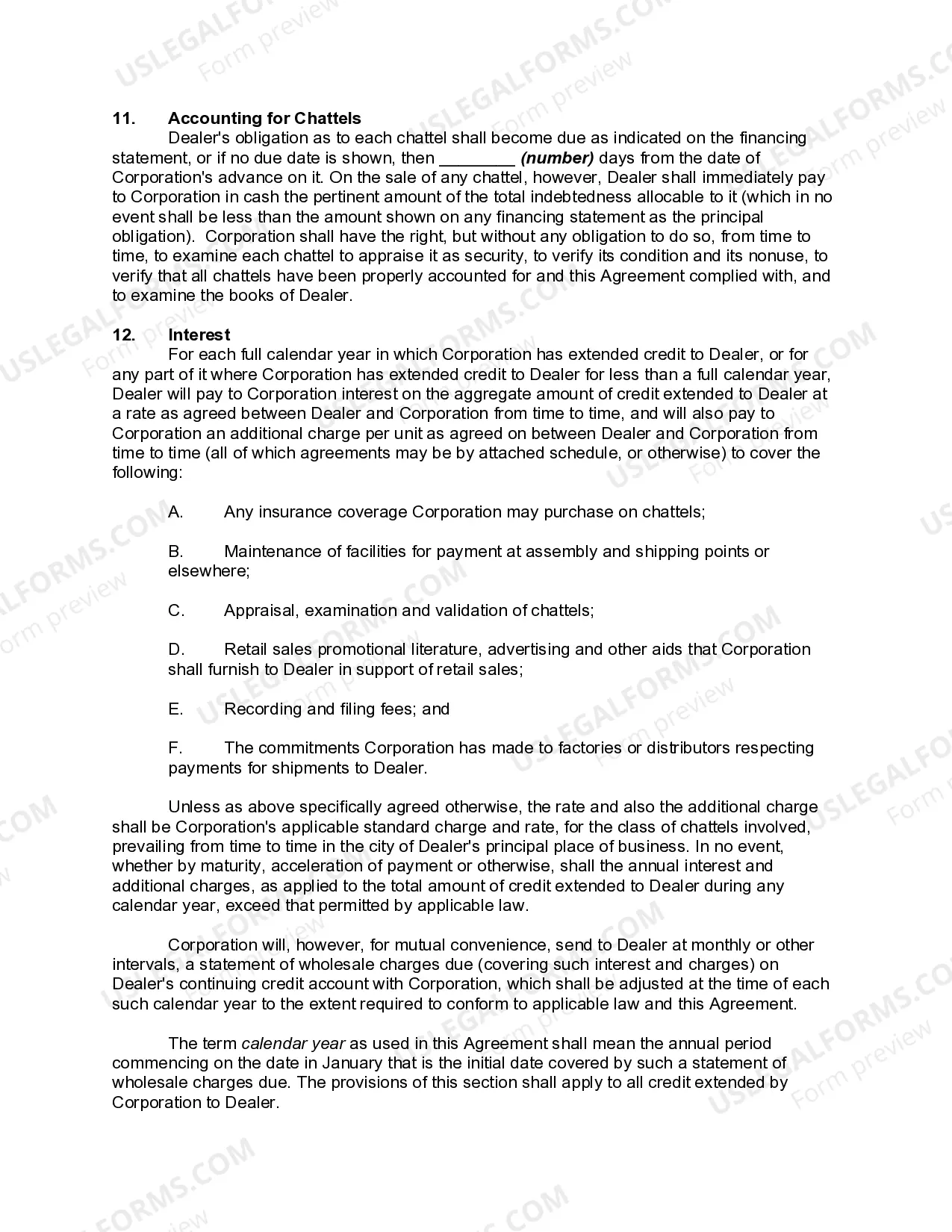

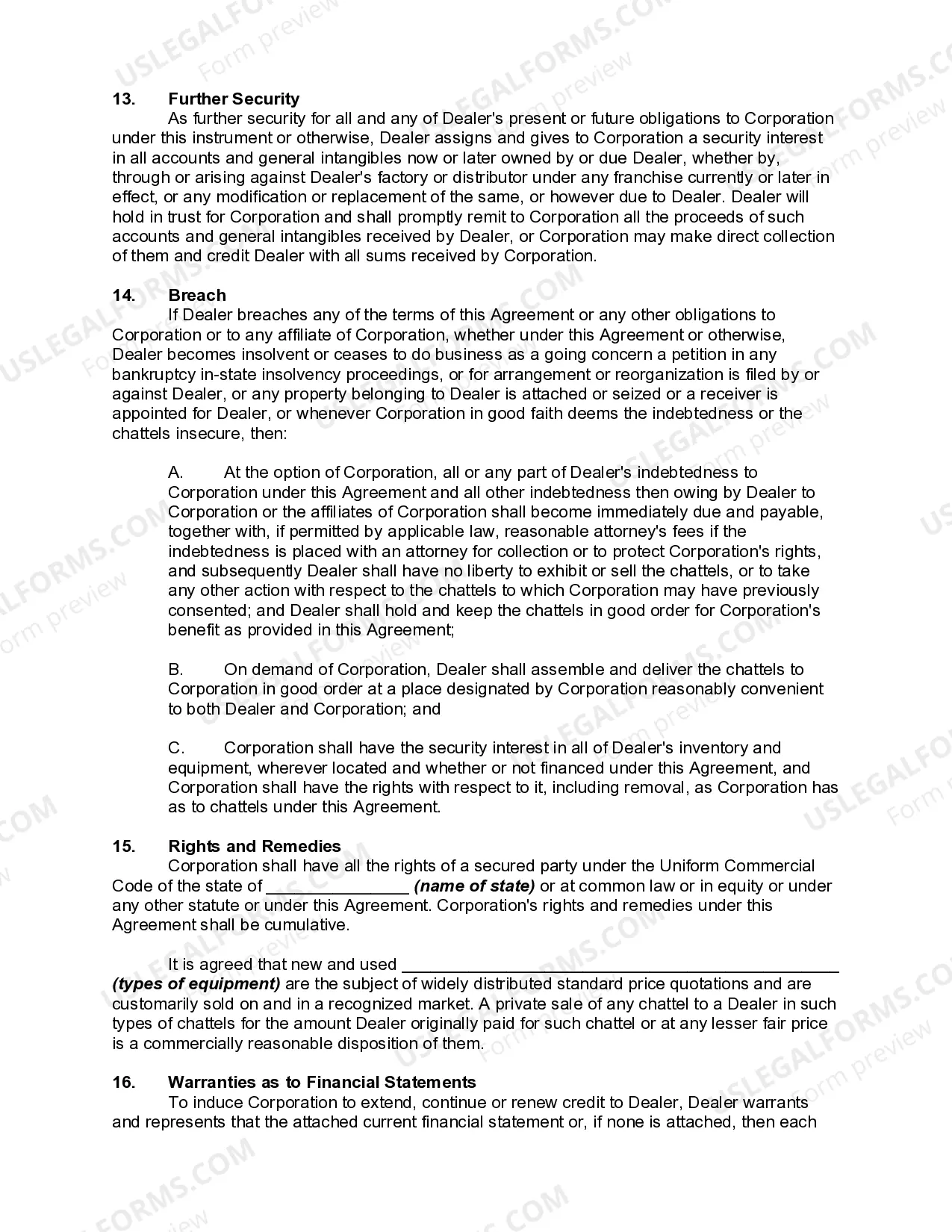

An Alaska Financing Agreement between a dealer and a credit corporation serves as a crucial contract that facilitates wholesale financing and establishes a security interest in accounts and general intangibles. This agreement is designed to ensure a smooth flow of funds and provide protection for both parties involved. Below, we will discuss the different types of Alaska Financing Agreements available, along with their key features and relevant keywords: 1. Wholesale Financing: Wholesale financing refers to a specialized form of financing where the credit corporation provides funds to the dealer for purchasing inventory in bulk. This enables the dealer to stock up on products and fulfill customer demands efficiently. 2. Security Interest: In this financing agreement, both parties establish a security interest in accounts and general intangibles. The credit corporation holds a security interest as collateral to secure the repayment of the financed amount. This is important to protect the credit corporation's investment and minimize risks. 3. Retail Financing: Apart from wholesale financing, some Alaska Financing Agreements may include provisions for retail financing. Retail financing caters to customers directly, enabling them to purchase goods from the dealer on credit. In this case, the credit corporation provides the necessary funds for the dealer to extend credit to customers. 4. Promissory Note: A promissory note is a critical component of the Alaska Financing Agreement. It outlines the borrower's promise to repay the funds borrowed from the credit corporation, including the terms and conditions of repayment, interest rates, and any additional fees or charges applicable. 5. Personal Guarantee: Some financing agreements may require a personal guarantee from the dealer's principal(s) or guarantor(s). This acts as an additional layer of security for the credit corporation, ensuring that assets owned by the guarantor(s) can be utilized for repayment in case of default. 6. Default and Remedies: To safeguard the credit corporation's interests, the Alaska Financing Agreement outlines the consequences of default and the available remedies. It typically includes provisions on late payment penalties, repossession of collateral, legal actions, and the distribution of proceeds from the sale of collateral. 7. Terms and Conditions: The agreement contains detailed terms and conditions agreed upon by both the dealer and the credit corporation. These include provisions related to the amount of funds provided, repayment schedule, interest rates, use of proceeds, financial covenants, termination rights, and confidentiality clauses. 8. Governing Law: Given the agreement's nature, it will specify the governing law of the state of Alaska, ensuring that any disputes or legal matters arising from the agreement are resolved in accordance with Alaskan laws. Keywords: Alaska Financing Agreement, Dealer, Credit Corporation, Wholesale Financing, Security Interest, Accounts, General Intangibles, Promissory Note, Personal Guarantee, Default, Remedies, Terms and Conditions, Governing Law.An Alaska Financing Agreement between a dealer and a credit corporation serves as a crucial contract that facilitates wholesale financing and establishes a security interest in accounts and general intangibles. This agreement is designed to ensure a smooth flow of funds and provide protection for both parties involved. Below, we will discuss the different types of Alaska Financing Agreements available, along with their key features and relevant keywords: 1. Wholesale Financing: Wholesale financing refers to a specialized form of financing where the credit corporation provides funds to the dealer for purchasing inventory in bulk. This enables the dealer to stock up on products and fulfill customer demands efficiently. 2. Security Interest: In this financing agreement, both parties establish a security interest in accounts and general intangibles. The credit corporation holds a security interest as collateral to secure the repayment of the financed amount. This is important to protect the credit corporation's investment and minimize risks. 3. Retail Financing: Apart from wholesale financing, some Alaska Financing Agreements may include provisions for retail financing. Retail financing caters to customers directly, enabling them to purchase goods from the dealer on credit. In this case, the credit corporation provides the necessary funds for the dealer to extend credit to customers. 4. Promissory Note: A promissory note is a critical component of the Alaska Financing Agreement. It outlines the borrower's promise to repay the funds borrowed from the credit corporation, including the terms and conditions of repayment, interest rates, and any additional fees or charges applicable. 5. Personal Guarantee: Some financing agreements may require a personal guarantee from the dealer's principal(s) or guarantor(s). This acts as an additional layer of security for the credit corporation, ensuring that assets owned by the guarantor(s) can be utilized for repayment in case of default. 6. Default and Remedies: To safeguard the credit corporation's interests, the Alaska Financing Agreement outlines the consequences of default and the available remedies. It typically includes provisions on late payment penalties, repossession of collateral, legal actions, and the distribution of proceeds from the sale of collateral. 7. Terms and Conditions: The agreement contains detailed terms and conditions agreed upon by both the dealer and the credit corporation. These include provisions related to the amount of funds provided, repayment schedule, interest rates, use of proceeds, financial covenants, termination rights, and confidentiality clauses. 8. Governing Law: Given the agreement's nature, it will specify the governing law of the state of Alaska, ensuring that any disputes or legal matters arising from the agreement are resolved in accordance with Alaskan laws. Keywords: Alaska Financing Agreement, Dealer, Credit Corporation, Wholesale Financing, Security Interest, Accounts, General Intangibles, Promissory Note, Personal Guarantee, Default, Remedies, Terms and Conditions, Governing Law.