Alaska Mortgage Note

Description

How to fill out Mortgage Note?

Discovering the right legitimate record template could be a battle. Naturally, there are plenty of templates accessible on the Internet, but how would you obtain the legitimate form you want? Utilize the US Legal Forms web site. The service offers thousands of templates, like the Alaska Mortgage Note, which you can use for organization and personal demands. Every one of the types are inspected by pros and satisfy state and federal demands.

If you are presently listed, log in to your bank account and then click the Down load option to get the Alaska Mortgage Note. Make use of your bank account to check with the legitimate types you possess ordered previously. Proceed to the My Forms tab of your respective bank account and acquire an additional copy of the record you want.

If you are a brand new end user of US Legal Forms, listed here are basic guidelines for you to follow:

- Initially, make sure you have selected the right form for the metropolis/area. You can look through the form using the Preview option and browse the form outline to ensure it is the right one for you.

- In the event the form does not satisfy your needs, make use of the Seach field to obtain the appropriate form.

- When you are certain the form is acceptable, go through the Get now option to get the form.

- Opt for the prices plan you want and type in the necessary info. Build your bank account and pay money for an order with your PayPal bank account or charge card.

- Choose the file structure and down load the legitimate record template to your device.

- Total, revise and produce and indication the attained Alaska Mortgage Note.

US Legal Forms is the largest library of legitimate types in which you can find various record templates. Utilize the service to down load appropriately-manufactured files that follow state demands.

Form popularity

FAQ

A person or entity collecting loan payments has the ability to sell a mortgage note for a lump sum of cash today, instead of holding the loan long-term over many years. You can choose to sell all, or just a portion of your note, depending on your capital needs.

Most mortgage note investments range from $20,000 to $50,000 per note. The cost will vary based on several factors, including the age of the note, payment history, loan-to-value ratio, and more.

When it comes to valuing a note, the key factors that impact the value are the stated interest rate and the amortization schedule of the note. A note with a below market interest rate would sell at a discount from its balance just like bonds trade in the public market.

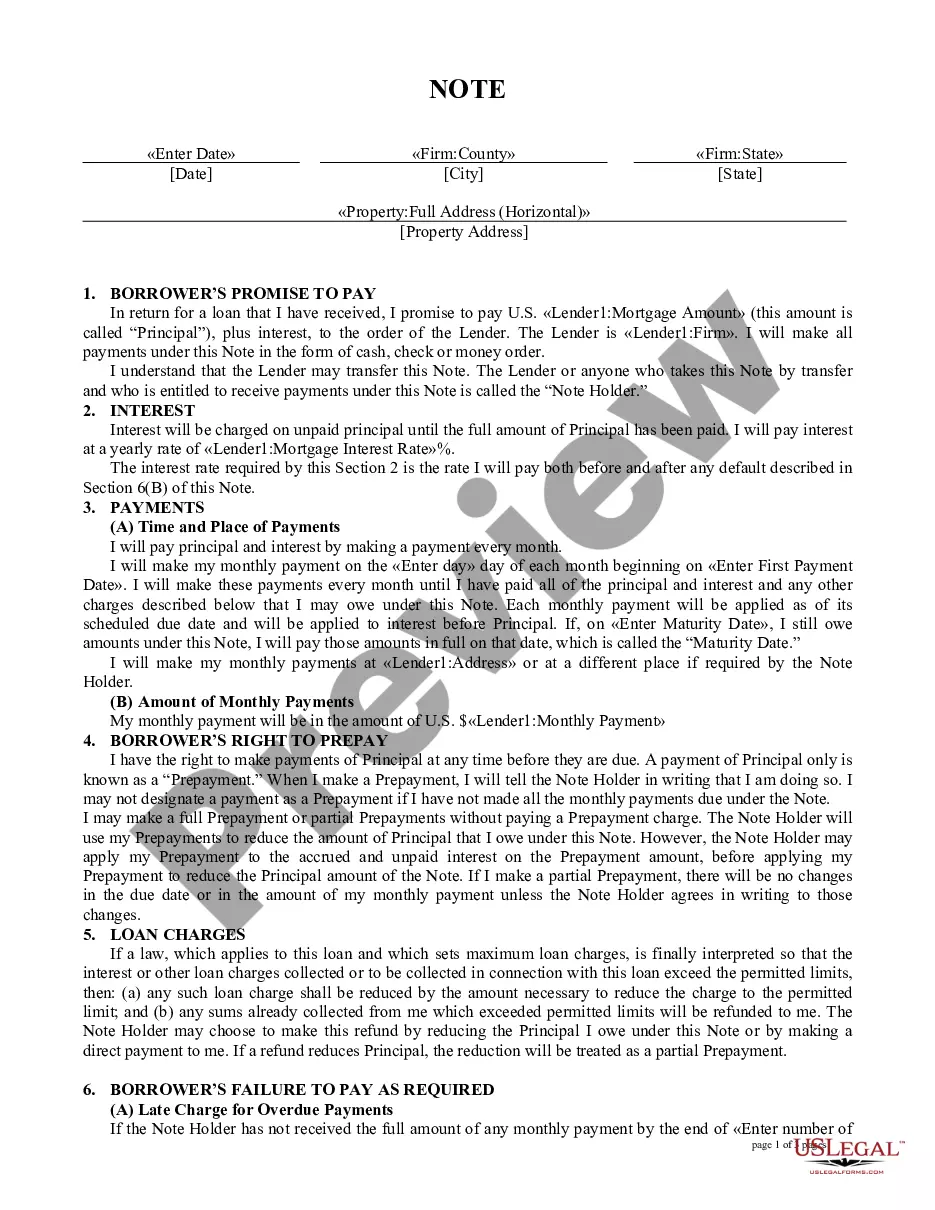

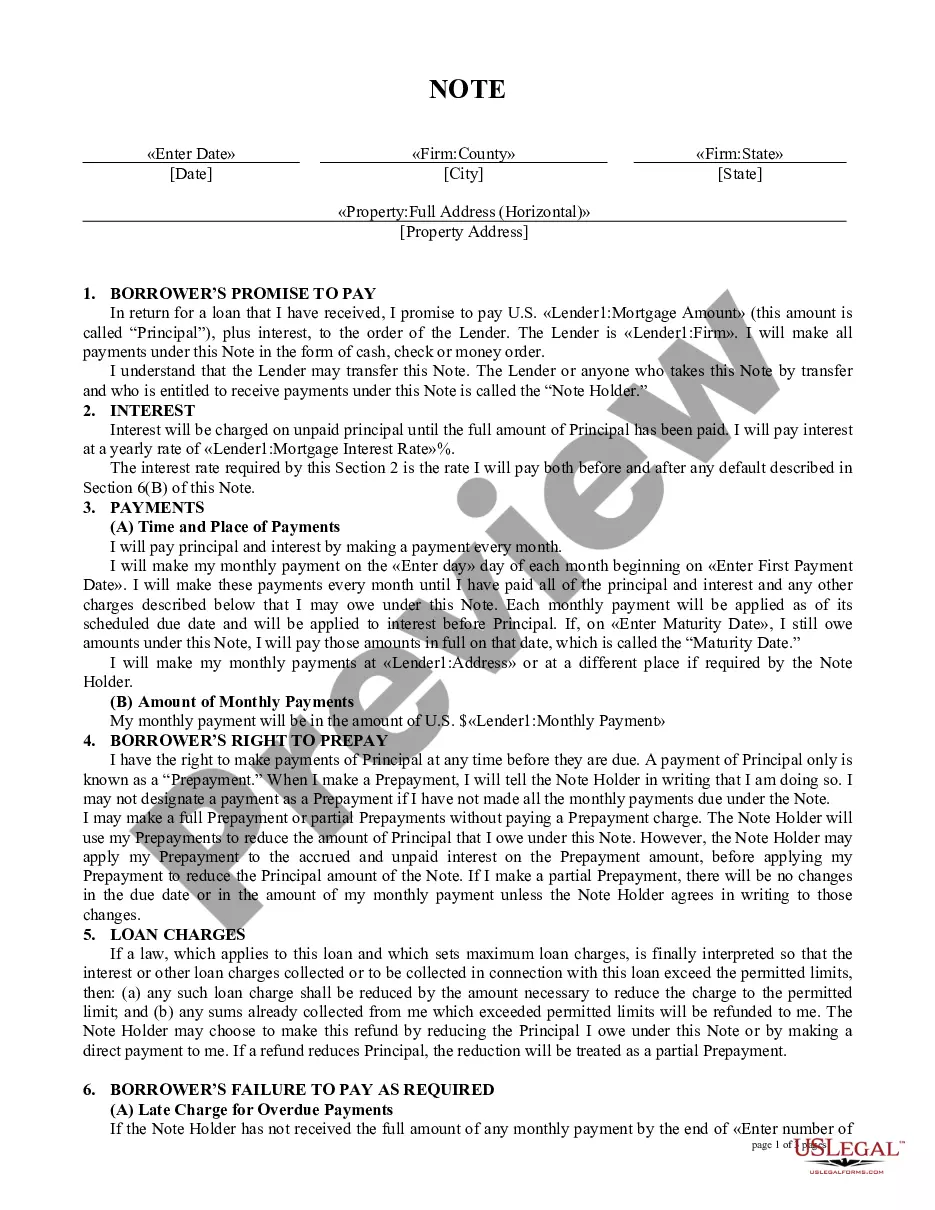

A mortgage note contains important legal information related to your property purchase loan, such as the interest rate and consequences if you fail to repay your loan. You can get a copy of your mortgage note by checking the county recorder or reaching directly to the lender.

The value of a mortgage note depends on several variables. Reputable buyers may offer around $0.70 on the dollar for the remaining principal balance, depending on the amount of risk they must take on should they purchase the note.

If you take out a home loan and are on the property's deed, you'll likely have to sign the mortgage. But even if the lender requires you to sign the mortgage, you might not have to sign the note. For example, say you're not eligible for a home loan at a good interest rate because your credit scores are terrible.

The mortgage note is signed by borrowers at the end of the home buying process stating your promise to repay the money you're borrowing from your mortgage lender. This document will list how much you'll pay each month, when you'll make these payments and your mortgage's interest rate.

There are three main options for selling a promissory note: to an individual, to a family member, or to a note-buying company. A note-buying company will offer you a partial or full purchase of the remaining balance on loan. The entire process of selling a promissory note can take 15 to 35 days.