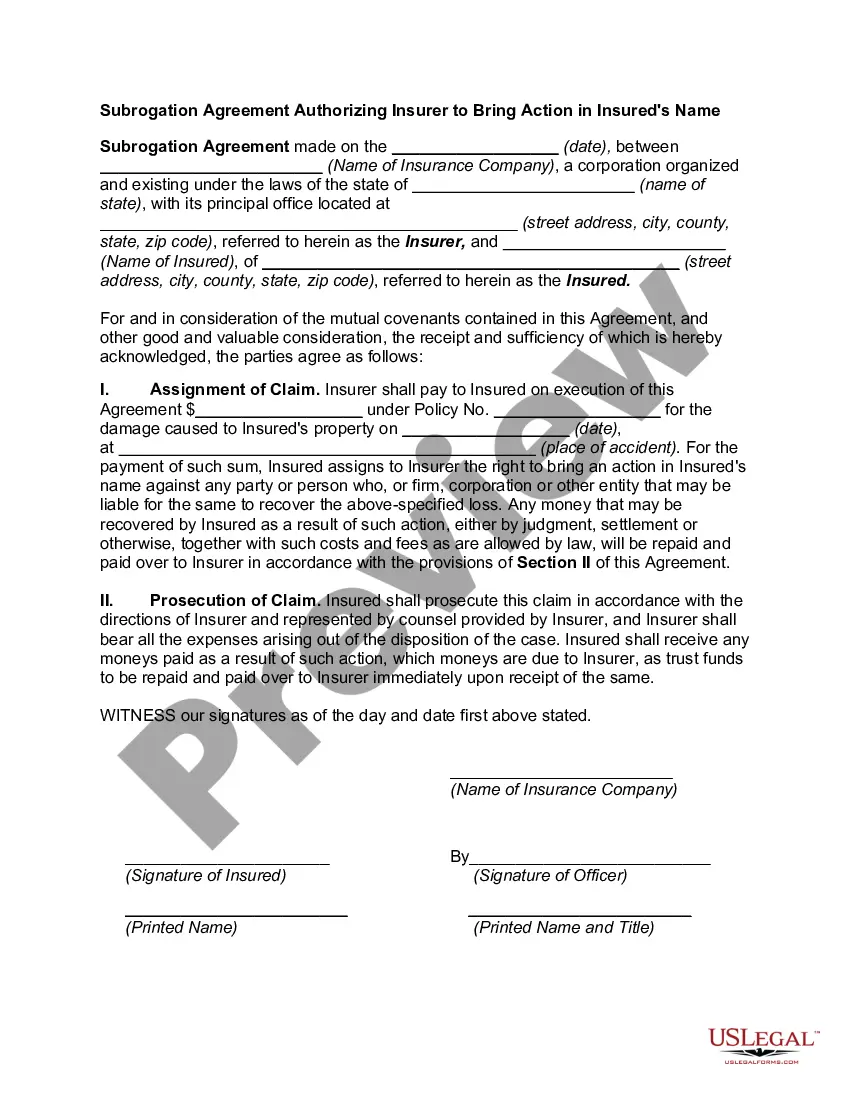

Alaska Subrogation Agreement Authorizing Insurer to Bring Action in Insured's Name: A Comprehensive Overview Introduction: The Alaska Subrogation Agreement Authorizing Insurer to Bring Action in Insured's Name is a legal document that empowers an insurance company to pursue legal action on behalf of their insured party, known as the suborder. This agreement enables the insurer, referred to as the surge, to seek recovery for damages caused by a third party and assert the rights of the insured. Types of Alaska Subrogation Agreement Authorizing Insurer to Bring Action in Insured's Name: 1. Automobile Insurance Subrogation Agreement: This type of subrogation agreement deals specifically with motor vehicle insurance policies. It enables the insurer to stand in the place of the insured when pursuing legal actions related to accidents or damages caused by another driver. 2. Property Insurance Subrogation Agreement: This agreement pertains to property insurance policies, allowing the insurer to initiate legal proceedings against liable parties who caused damage to the insured property. It commonly covers incidents such as fires, floods, or other forms of property damage. 3. Medical Insurance Subrogation Agreement: Medical insurance policies often contain subrogation clauses that authorize the insurer to recover expenses paid for medical treatments from third parties legally responsible for the injuries sustained by the insured. This agreement empowers the insurer to file lawsuits against negligent parties, such as at-fault individuals in personal injury cases. Key Elements of an Alaska Subrogation Agreement Authorizing Insurer to Bring Action in Insured's Name: 1. Subrogation Rights and Benefits: This section outlines the contractual provision that grants the insurer the right to pursue legal action on behalf of the insured and seek compensation for damages. It also clarifies the benefits the insurer may recover, including direct expenses, legal costs, and potential future losses caused by the third party's actions. 2. Subrogation Process: This part details the procedural aspects of the subrogation process, such as the insurer's responsibility to investigate the incident that led to the insured party's loss or injury. It also specifies the timelines, notifications, and documentation required for initiating legal proceedings in the insured's name. 3. Cooperation and Assistance: To ensure a smooth subrogation process, this segment emphasizes the insured's obligation to cooperate fully with the insurer in all legal matters. It may include requirements such as providing necessary evidence, attending court hearings if needed, and assisting in settlement negotiations. 4. Subrogation Payment Distribution: The agreement should address how any recovered funds or settlements will be distributed. Common distribution methods include first satisfying the insurer's subrogation costs, followed by reimbursing the insured for any out-of-pocket expenses, and finally, dividing the remaining proceeds between the insured and the insurer, according to their respective interests. Conclusion: The Alaska Subrogation Agreement Authorizing Insurer to Bring Action in Insured's Name is a crucial legal document that empowers insurance companies to act on behalf of their insured parties and pursue compensation from liable third parties. By understanding the different types and key elements of such agreements, both insurers and insured parties can navigate subrogation processes more effectively and protect their rights and interests.

Alaska Subrogation Agreement Authorizing Insurer to Bring Action in Insured's Name

Description

How to fill out Alaska Subrogation Agreement Authorizing Insurer To Bring Action In Insured's Name?

US Legal Forms - one of many greatest libraries of legitimate types in the USA - provides a wide range of legitimate papers web templates you can down load or print out. Making use of the web site, you may get thousands of types for business and specific uses, categorized by classes, states, or keywords and phrases.You will discover the latest versions of types just like the Alaska Subrogation Agreement Authorizing Insurer to Bring Action in Insured's Name within minutes.

If you already have a monthly subscription, log in and down load Alaska Subrogation Agreement Authorizing Insurer to Bring Action in Insured's Name through the US Legal Forms collection. The Download key will appear on each kind you see. You have access to all formerly acquired types in the My Forms tab of your profile.

If you would like use US Legal Forms for the first time, listed below are easy instructions to help you get started out:

- Be sure you have picked out the correct kind for the town/region. Click on the Preview key to examine the form`s information. Look at the kind outline to ensure that you have selected the right kind.

- If the kind does not match your requirements, take advantage of the Research area at the top of the display to get the one who does.

- When you are happy with the form, affirm your decision by clicking on the Purchase now key. Then, choose the pricing strategy you prefer and provide your accreditations to sign up for an profile.

- Procedure the financial transaction. Use your Visa or Mastercard or PayPal profile to finish the financial transaction.

- Choose the formatting and down load the form on your device.

- Make changes. Complete, change and print out and indicator the acquired Alaska Subrogation Agreement Authorizing Insurer to Bring Action in Insured's Name.

Every design you added to your money lacks an expiration particular date and is yours permanently. So, in order to down load or print out yet another copy, just check out the My Forms portion and then click in the kind you will need.

Obtain access to the Alaska Subrogation Agreement Authorizing Insurer to Bring Action in Insured's Name with US Legal Forms, probably the most extensive collection of legitimate papers web templates. Use thousands of skilled and status-particular web templates that meet up with your business or specific requirements and requirements.

Form popularity

FAQ

If you've been in an accident and filed a claim with your insurance company, you may have received a subrogation letter. This document allows the insurance company to pursue a claim against a third party that caused damage to their insured, after the insurance company has paid out a claim to the insured.

If you've been in an accident and filed a claim with your insurance company, you may have received a subrogation letter. This document allows the insurance company to pursue a claim against a third party that caused damage to their insured, after the insurance company has paid out a claim to the insured.

Simply put, subrogation protects you and your insurer from paying for losses that aren't your fault. It's common in auto, health insurance and homeowners policies. It lets your insurer pursue the person at fault to recover the money paid out for a claim that wasn't your fault.

At the minimum, your subrogation file should contain all elements corresponding to liability determination and proof of damages. Being able to prove who is at fault is essential. You'll want to include documentation and any information you've gathered, such as witness statements or police reports.

Additional Details letter creation date. insured name. claim number and policy number. date of loss. recipient name. damage amount. claims specialist name and title.

If your business contracts with clients, you may want a waiver of subrogation in place. This will protect you if you are fully or partially responsible for damages accrued during or after a job with a client.

A subrogation receipt transferring the insured's entire causes of action to the insurer allows the insurer to recover in the insured's name for the entire loss, not just to the extent of its payment.

Simply put, subrogation protects you and your insurer from paying for losses that aren't your fault. It's common in auto, health insurance and homeowners policies. It lets your insurer pursue the person at fault to recover the money paid out for a claim that wasn't your fault.