Alaska Trust Agreement for Minor Qualifying for Annual Gift-Tax Exclusion; Beneficiary has Option to Continue Trust Past Age 21; Income Must be Paid to Beneficiary After Age 21

Instant download

Description

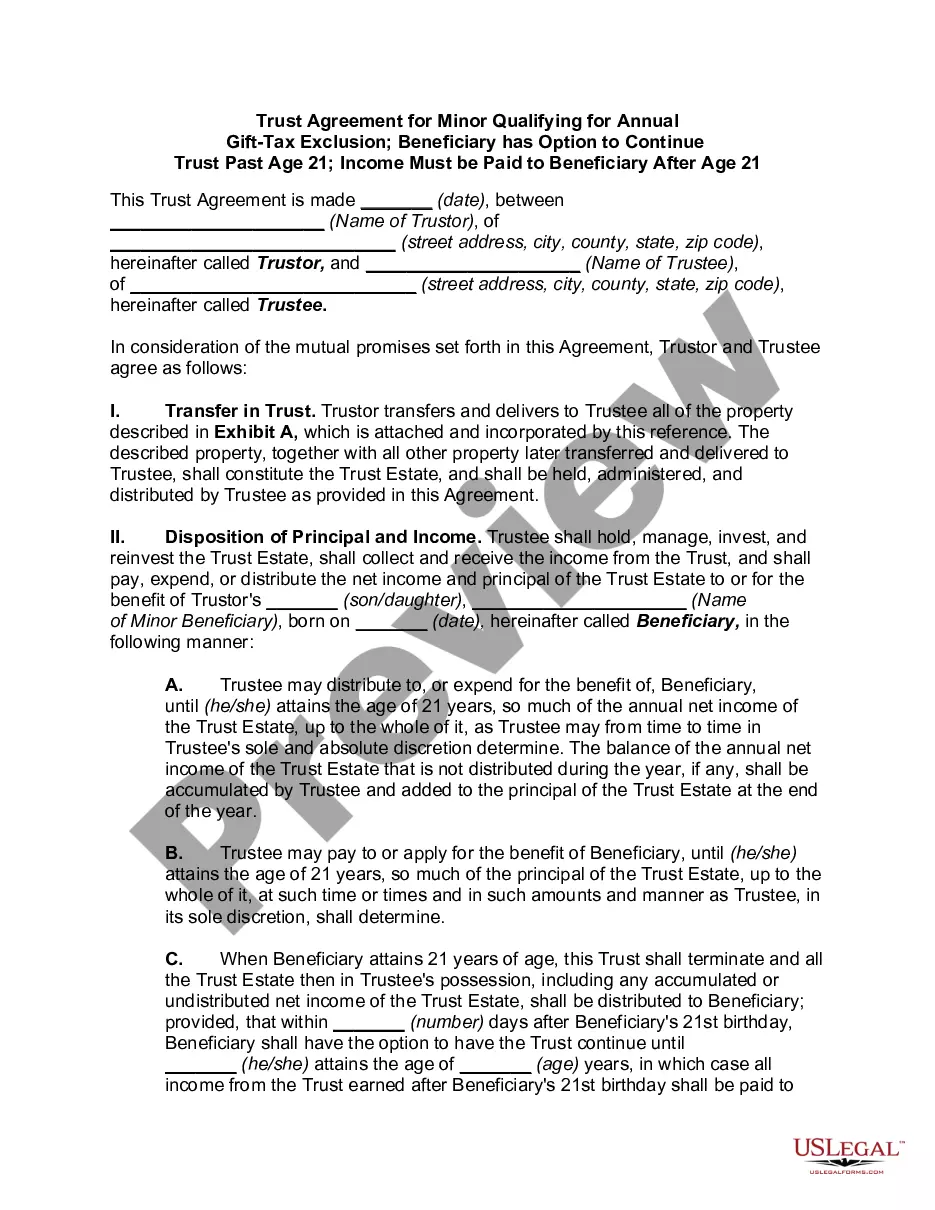

Gifts in trust to minors are quite common, both as a means of building up a child's estate and as a way to minimize federal gift, income, and estate taxes payable by the trustor or the trustor's estate. A carefully drafted minor's trust can provide competent management of the property on the minor's behalf, while avoiding any problem of the minor's disability to act with respect to that property. Such a trust can effect substantial tax savings for the trustor-donor while regulating distribution of the trust income and principal in keeping with the needs of the minor.

A section 2503(c) Minor's Trust is a separate legal entity (a trust) established to hold gifts in trust for a child until the child reaches age 21. The trust is named after the section of the Internal Revenue Code upon which it is based.

Normally, for a gift to qualify for the annual gift tax exclusion, it must be a gift of a present interest. This means the recipient must be able to use the gift immediately. A gift of a future interest in some property (e.g., the right to the money when the child turns 21) would not normally qualify, except for section 2503(c) of the Internal Revenue Code. Section 2503(c) sets out the conditions under which a gift of a future interest to a minor qualifies for the gift tax exclusion.

Free preview