The Alaska Certificate of Borrower is an essential document that is often required when applying for a commercial loan in the state of Alaska. This certificate serves as proof of the borrower's identity, financial standing, and compliance with state laws. It is a crucial step in the loan application process, providing lenders with crucial information to assess the borrower's credibility and ability to repay the loan. Keywords: Alaska, certificate of borrower, commercial loan, identity, financial standing, compliance, loan application, lenders, credibility, repayment. There are several types of Alaska Certificate of Borrower specifically designed for different commercial loan scenarios. Let's look at a few of the most common types: 1. Alaska Certificate of Borrower for Small Business Loans: This type of certificate is tailored for small business owners seeking financial assistance for their ventures. It includes detailed information about the business, such as its legal structure, ownership details, financial statements, tax records, and other relevant documentation. 2. Alaska Certificate of Borrower for Construction Loans: Construction projects often require specialized financing, and this type of certificate aims to provide lenders with crucial information related to the borrower's construction project. It includes details about the project's scope, budget, timeline, contractor information, permits, and other relevant documentation to assess the feasibility of the loan. 3. Alaska Certificate of Borrower for Real Estate Loans: Real estate transactions, such as purchasing commercial property or developing land, involve substantial financial commitments. This certificate provides lenders with information about the borrower's real estate development plans, property details, market analysis, financial projections, and other relevant documents for evaluating the borrower's eligibility for the loan. 4. Alaska Certificate of Borrower for Equipment Financing: When businesses require financing for purchasing or leasing equipment, this type of certificate becomes crucial. It includes details about the equipment, its value, intended use, financial projections, and other documentation necessary to assess the equipment's viability as collateral. 5. Alaska Certificate of Borrower for Agricultural Loans: Agricultural loans cater to farmers and other agricultural businesses. This certificate focuses on providing lenders with information about the borrower's farming operations, land details, crop yields, livestock inventory, financial statements, and other related documents. It is important to note that the specific requirements for each type of Alaska Certificate of Borrower may vary depending on the lender, loan amount, and the borrower's industry. As such, potential borrowers should consult with their lender or financial institution to gather the necessary information and documentation before commencing the loan application process.

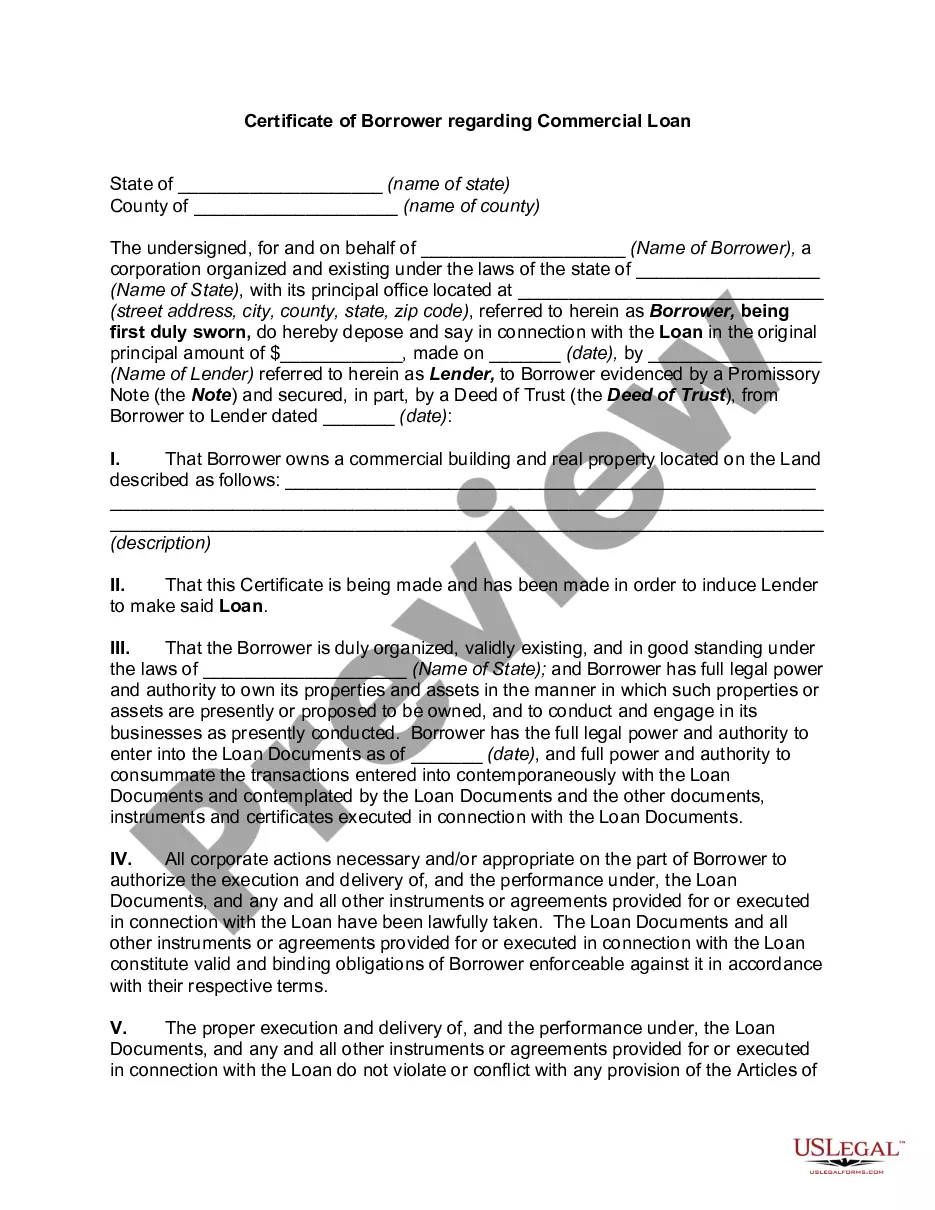

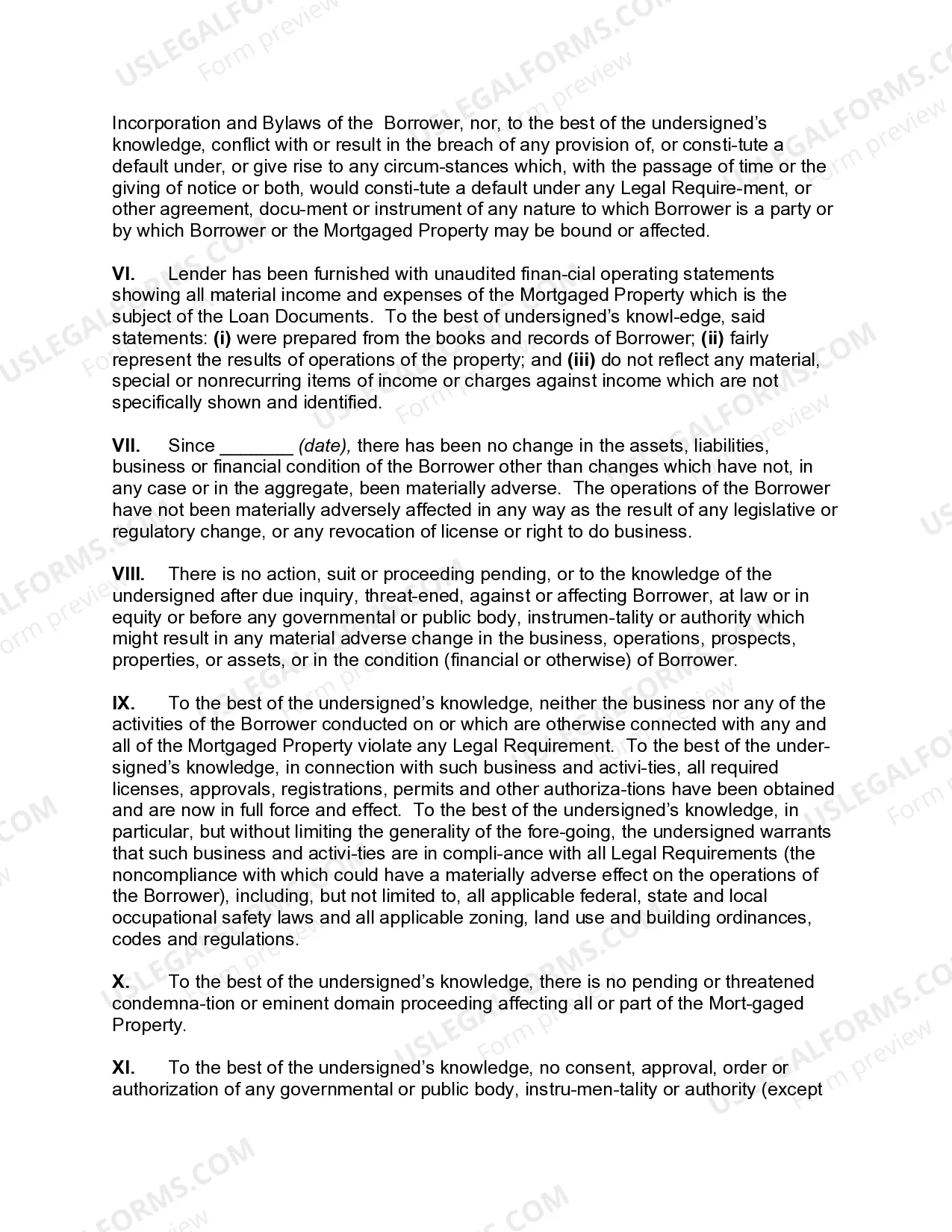

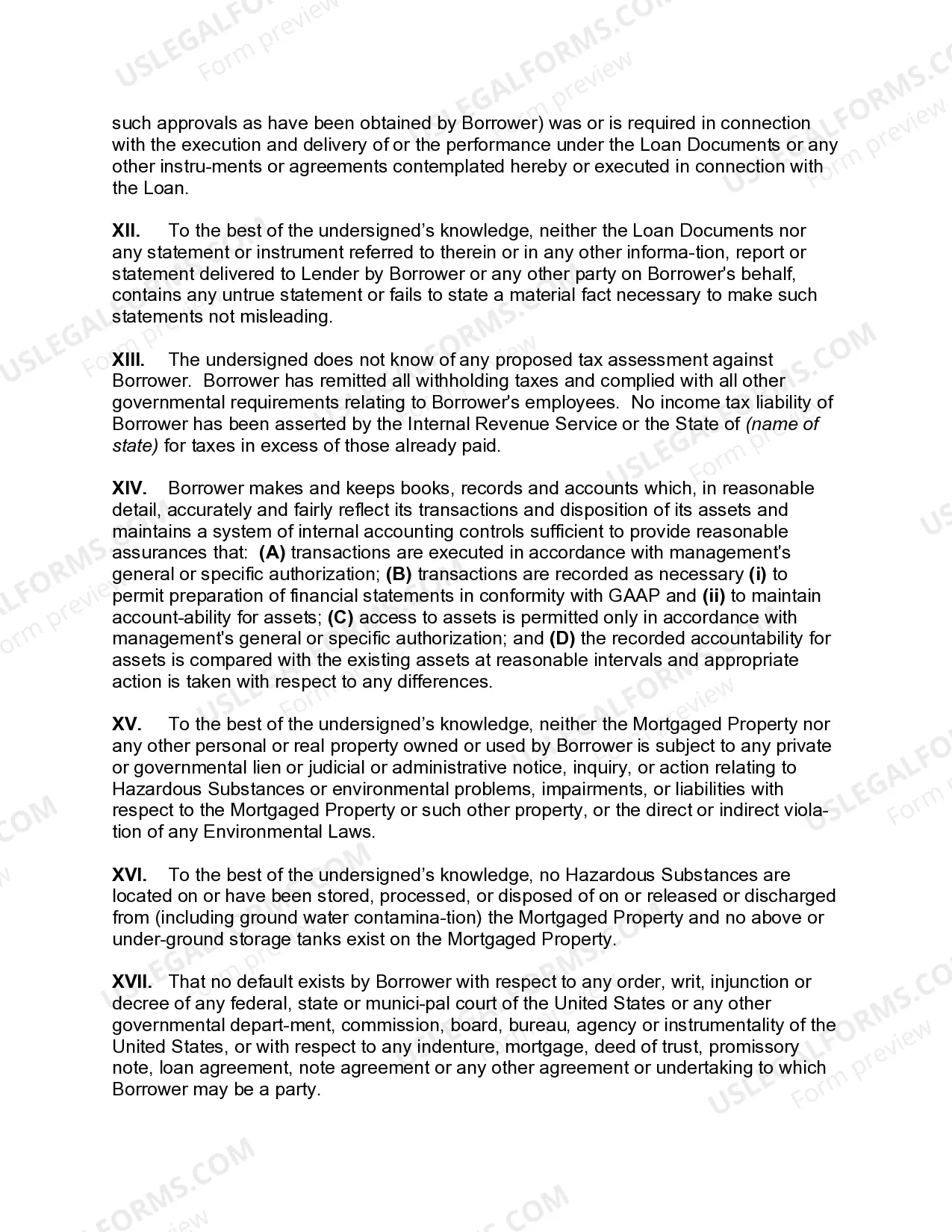

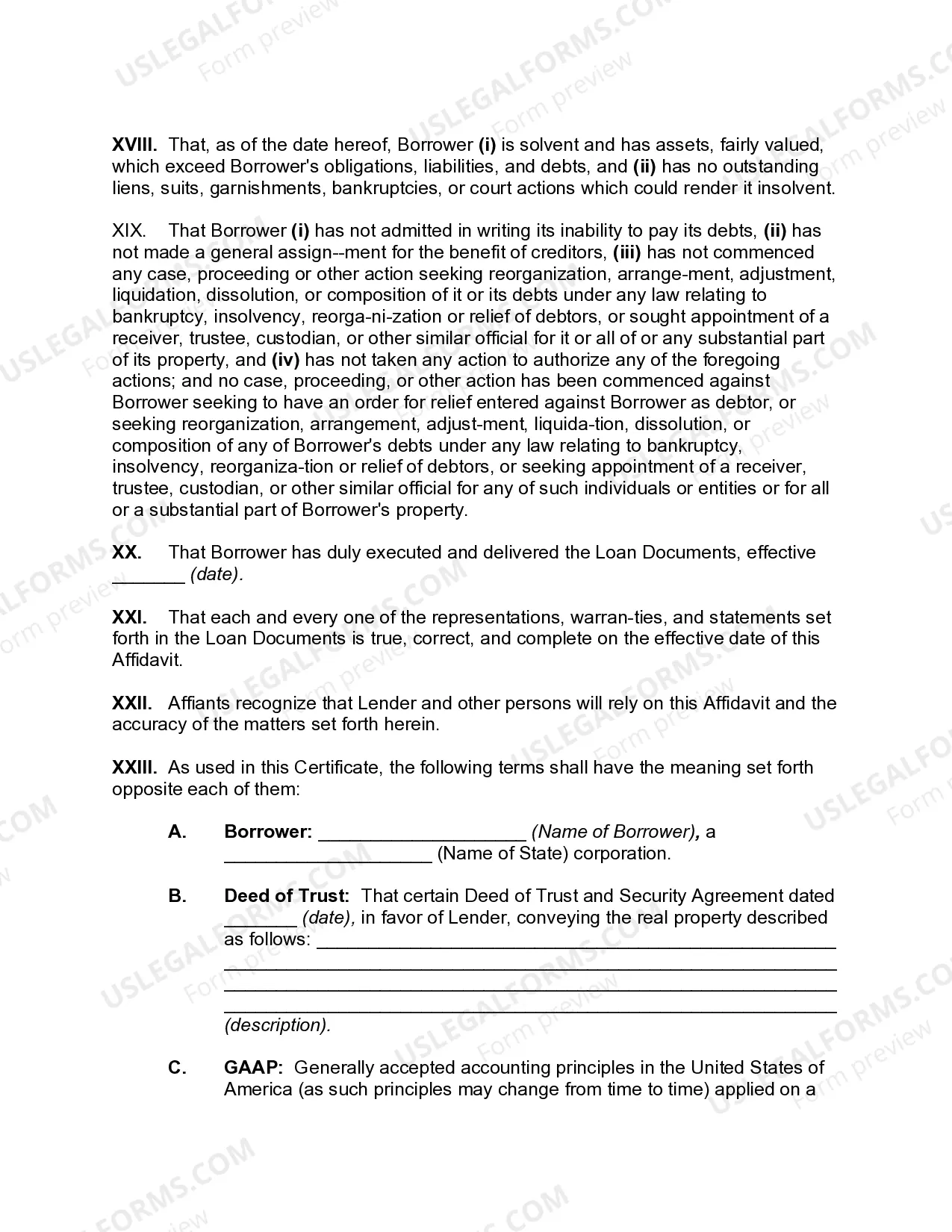

Alaska Certificate of Borrower regarding Commercial Loan

Description

How to fill out Alaska Certificate Of Borrower Regarding Commercial Loan?

You are able to invest hours on the Internet trying to find the legal papers template that meets the state and federal needs you will need. US Legal Forms gives a huge number of legal varieties which are evaluated by specialists. It is simple to obtain or print the Alaska Certificate of Borrower regarding Commercial Loan from our services.

If you have a US Legal Forms bank account, it is possible to log in and click the Download switch. Following that, it is possible to full, change, print, or signal the Alaska Certificate of Borrower regarding Commercial Loan. Every legal papers template you get is the one you have eternally. To acquire one more backup of any purchased type, check out the My Forms tab and click the corresponding switch.

Should you use the US Legal Forms site the very first time, follow the straightforward directions under:

- First, make certain you have chosen the proper papers template for the area/area that you pick. Look at the type outline to make sure you have picked out the correct type. If readily available, make use of the Review switch to search from the papers template also.

- If you wish to discover one more edition from the type, make use of the Search industry to find the template that meets your requirements and needs.

- When you have located the template you desire, simply click Purchase now to continue.

- Pick the rates program you desire, type in your accreditations, and sign up for a free account on US Legal Forms.

- Total the financial transaction. You can use your bank card or PayPal bank account to fund the legal type.

- Pick the file format from the papers and obtain it in your product.

- Make adjustments in your papers if required. You are able to full, change and signal and print Alaska Certificate of Borrower regarding Commercial Loan.

Download and print a huge number of papers web templates while using US Legal Forms web site, that provides the greatest variety of legal varieties. Use professional and express-specific web templates to tackle your small business or person demands.