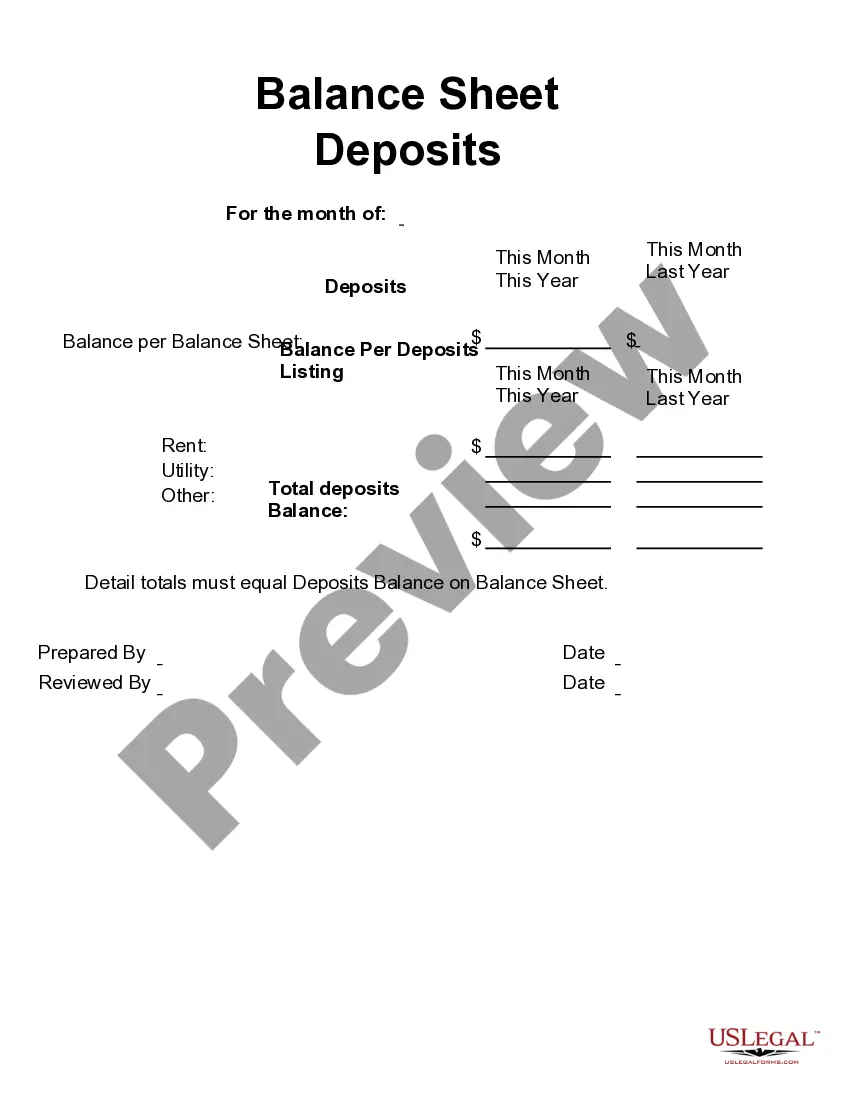

Alaska Balance Sheet Deposits: A Comprehensive Overview In the context of finance and banking, a balance sheet is a crucial financial statement that provides an overview of an organization's financial position at a given point in time. Among the various elements that constitute a balance sheet, deposits play a pivotal role in Alaska's financial landscape. In this article, we delve into the intricacies of Alaska Balance Sheet Deposits, shedding light on their significance and various types. Keywords: Alaska Balance Sheet Deposits, finance, banking, financial statement, deposits, types What are Alaska Balance Sheet Deposits? Alaska Balance Sheet Deposits refer to the funds held by banks, credit unions, and other financial institutions within the state of Alaska, as presented on their respective balance sheets. These deposits comprise various financial instruments such as demand deposits, time deposits, and savings deposits that institutions receive from customers, businesses, and organizations. 1. Demand Deposits: Demand deposits, sometimes referred to as checking or current accounts, are a type of Alaska Balance Sheet Deposit that facilitates immediate access to funds. Depositors can withdraw money without prior notice or restrictions. These deposits often serve as a transactional account, offering services such as transfers, bill payments, and debit card usage. 2. Time Deposits: Time deposits, also commonly known as certificates of deposit (CDs), are Alaska Balance Sheet Deposits that have a fixed term and predetermined interest rate. The term typically ranges from a few months to several years. These deposits require depositors to commit their funds for the specified period, and an early withdrawal may entail penalties. Time deposits often offer higher interest rates than demand deposits due to the customer's commitment to keep the funds locked for a specific duration. 3. Savings Deposits: Savings deposits are a type of Alaska Balance Sheet Deposit that allows individuals and organizations to earn interest while maintaining access to their funds. These deposits typically have lower interest rates compared to time deposits but provide more flexibility in terms of withdrawal frequency and ease of access. Savings deposits are suitable for customers who want to grow their funds while keeping them relatively liquid. 4. Money Market Deposits: Money market deposits are a less common yet significant type of Alaska Balance Sheet Deposit. These deposits combine the features of savings and checking accounts, offering depositors a higher interest rate on their funds. Money market deposit accounts often require higher minimum balances and limit the number of monthly transactions. Financial institutions utilize these deposits to invest in short-term securities and other low-risk investments. 5. Brokered Deposits: Brokered deposits are a specialized type of Alaska Balance Sheet Deposits orchestrated by brokers. These deposits involve third-party intermediaries who gather deposits from multiple individuals or businesses and then distribute them among different financial institutions. Brokered deposits can be an effective means for institutions to boost their deposit base quickly and access funds outside their typical geographical reach. In conclusion, Alaska Balance Sheet Deposits encompass a range of financial instruments that financial institutions hold to ensure liquidity and facilitate economic growth within the state. Demand deposits, time deposits, savings deposits, money market deposits, and brokered deposits are some key types of Alaska Balance Sheet Deposits. Understanding these categories helps individuals, businesses, and financial institutions make informed decisions regarding their deposit and investment strategies, ultimately contributing to Alaska's financial stability.

Alaska Balance Sheet Deposits

Description

How to fill out Alaska Balance Sheet Deposits?

If you want to complete, download, or print legal file themes, use US Legal Forms, the largest collection of legal forms, that can be found on-line. Utilize the site`s basic and practical search to discover the papers you will need. Various themes for company and personal uses are sorted by classes and suggests, or key phrases. Use US Legal Forms to discover the Alaska Balance Sheet Deposits in a few click throughs.

In case you are previously a US Legal Forms customer, log in to the profile and click the Download switch to find the Alaska Balance Sheet Deposits. Also you can entry forms you formerly delivered electronically in the My Forms tab of your own profile.

If you are using US Legal Forms the very first time, follow the instructions below:

- Step 1. Ensure you have chosen the form for your correct metropolis/region.

- Step 2. Use the Review option to examine the form`s information. Don`t forget to read through the information.

- Step 3. In case you are unsatisfied using the kind, utilize the Search industry near the top of the display screen to discover other versions of your legal kind web template.

- Step 4. After you have discovered the form you will need, click on the Purchase now switch. Choose the prices plan you choose and include your references to sign up for the profile.

- Step 5. Procedure the financial transaction. You should use your charge card or PayPal profile to finish the financial transaction.

- Step 6. Find the formatting of your legal kind and download it in your gadget.

- Step 7. Full, change and print or signal the Alaska Balance Sheet Deposits.

Each and every legal file web template you acquire is your own permanently. You may have acces to every single kind you delivered electronically inside your acccount. Click on the My Forms segment and pick a kind to print or download once more.

Compete and download, and print the Alaska Balance Sheet Deposits with US Legal Forms. There are many professional and status-specific forms you can use for the company or personal needs.