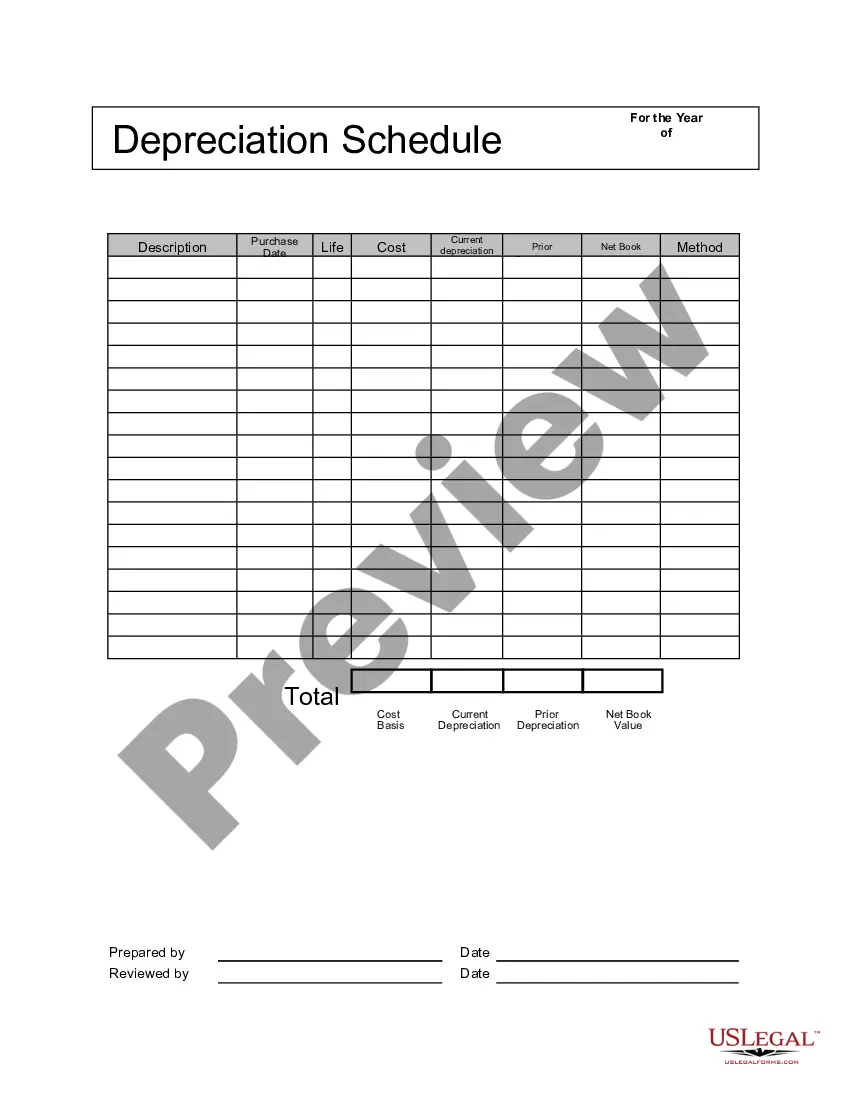

Alaska Depreciation Schedule is a specific regulated timeline that determines the deduction of expenses related to the wear and tear, deterioration, or obsolescence of tangible assets used for business purposes in the state of Alaska. It is an integral part of financial planning and tax management for businesses operating in Alaska. The Alaska Depreciation Schedule enables businesses to accurately allocate the costs of acquiring or improving the assets over their useful life, helping them recover the investment expended over time and lowering their taxable income. By spreading the cost of assets over their expected lifespan, businesses can reflect the gradual reduction in value of those assets on their financial statements and tax returns. Different types of Alaska Depreciation Schedules can be created based on the accounting methods used to calculate depreciation. Commonly used methods include: 1. Straight-Line Depreciation: This method allocates the cost of an asset evenly over its useful life. It assumes that the asset's value depreciates at a constant rate each year. 2. Declining Balance Depreciation: This method allows for a higher deduction in the early years of asset ownership, assuming that assets lose value more rapidly initially and then at a decreasing rate over time. 3. Double Declining Balance Depreciation: Similar to declining balance depreciation, this method enables businesses to depreciate assets at twice the rate of straight-line depreciation each year. 4. Sum-of-the-Years-Digits Depreciation: This method assigns higher depreciation in the early years and lower depreciation in the later years of an asset's useful life. It is calculated by using a fraction that consists of the sum of the asset's useful years as the numerator and decreasing this fraction each year until it reaches one in the final year. 5. MARS (Modified Accelerated Cost Recovery System): This is a commonly used depreciation method for federal income tax purposes. It assigns a shorter useful life to assets, allowing for more rapid deductions in the early years of an asset's life. It is essential for businesses in Alaska to comply with the necessary regulations and properly document their depreciation schedules to ensure accurate financial reporting and tax filings. Seeking professional guidance from accountants or tax advisors familiar with Alaska's depreciation laws can help businesses choose the most appropriate method for their specific assets and maximize tax benefits while remaining compliant with state regulations.

Alaska Depreciation Schedule

Description

How to fill out Alaska Depreciation Schedule?

Are you presently in the place where you require documents for either enterprise or person reasons nearly every working day? There are a variety of authorized papers layouts available online, but locating types you can rely on isn`t easy. US Legal Forms delivers 1000s of kind layouts, like the Alaska Depreciation Schedule, that happen to be created in order to meet federal and state demands.

If you are previously knowledgeable about US Legal Forms website and have a free account, simply log in. Next, you can download the Alaska Depreciation Schedule design.

Should you not come with an account and want to begin using US Legal Forms, adopt these measures:

- Get the kind you will need and ensure it is for your appropriate town/region.

- Make use of the Preview switch to check the shape.

- Browse the explanation to actually have selected the correct kind.

- If the kind isn`t what you are looking for, make use of the Lookup discipline to get the kind that meets your requirements and demands.

- Whenever you find the appropriate kind, simply click Purchase now.

- Pick the rates prepare you would like, submit the specified info to generate your account, and buy your order making use of your PayPal or Visa or Mastercard.

- Pick a practical data file formatting and download your backup.

Find all of the papers layouts you possess bought in the My Forms food selection. You can obtain a further backup of Alaska Depreciation Schedule anytime, if possible. Just click on the necessary kind to download or printing the papers design.

Use US Legal Forms, probably the most considerable assortment of authorized types, in order to save time as well as stay away from errors. The services delivers expertly created authorized papers layouts which can be used for a range of reasons. Create a free account on US Legal Forms and start creating your lifestyle a little easier.