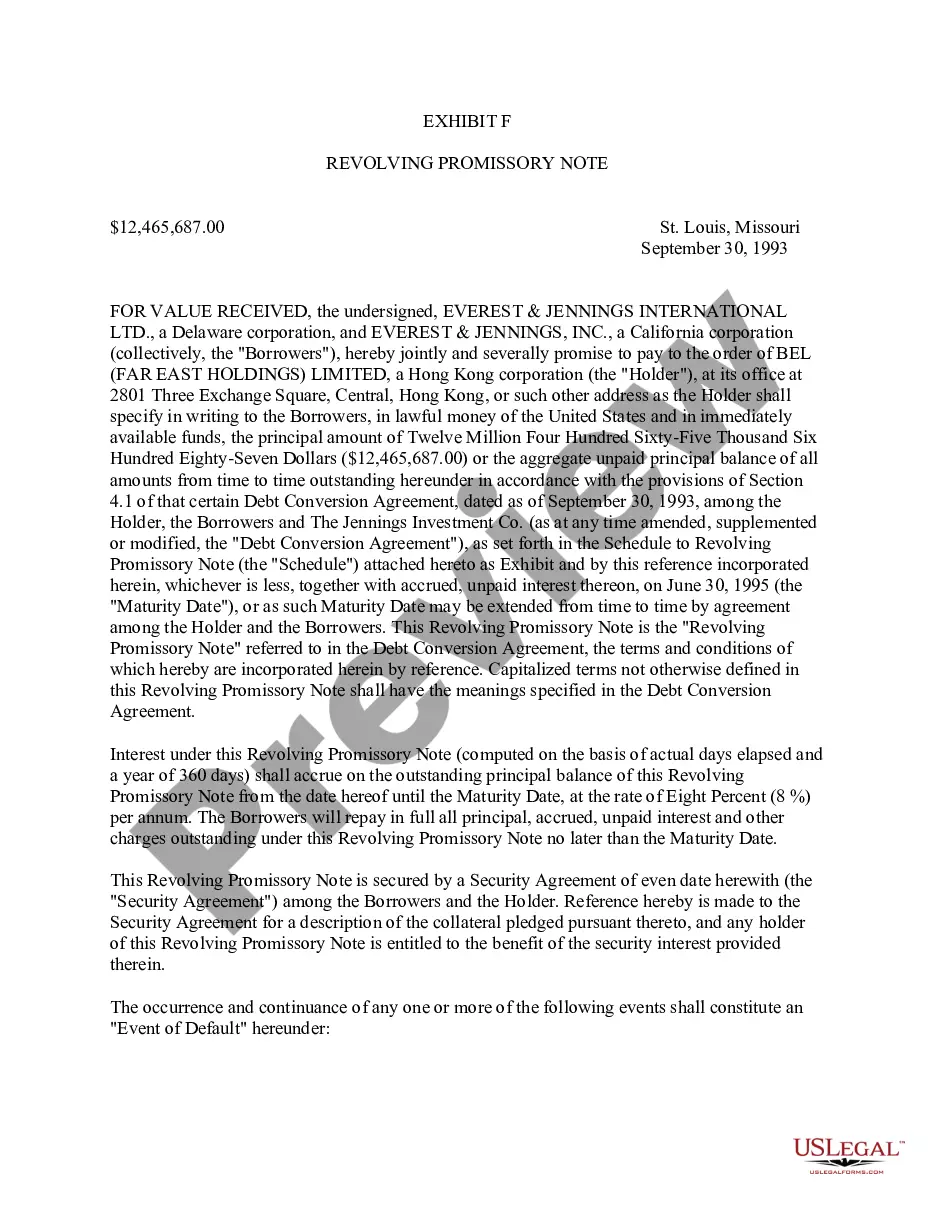

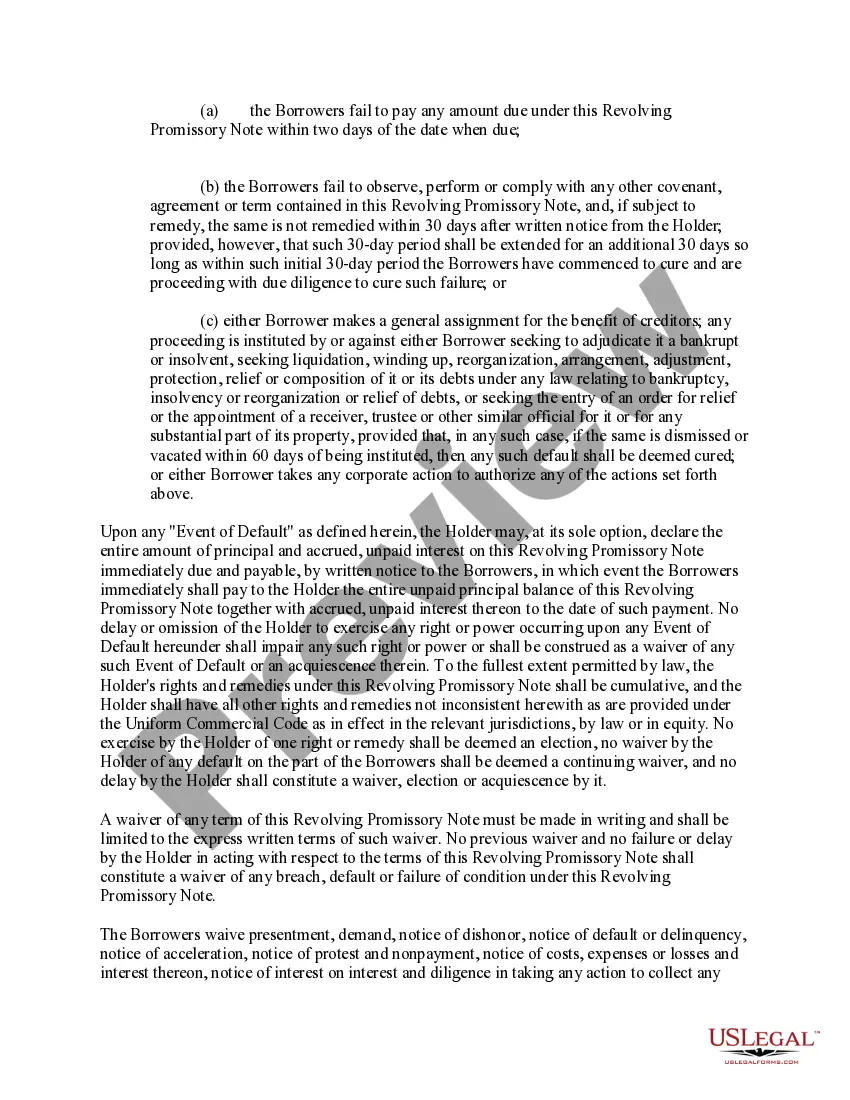

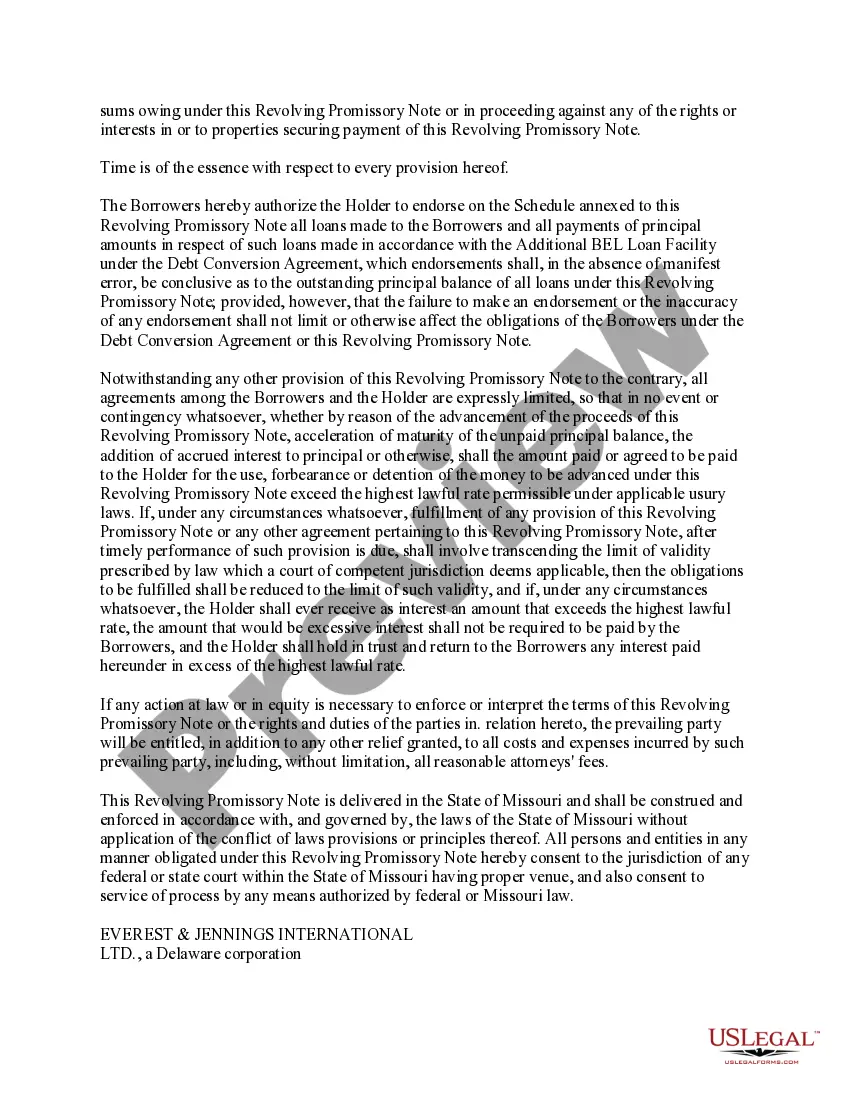

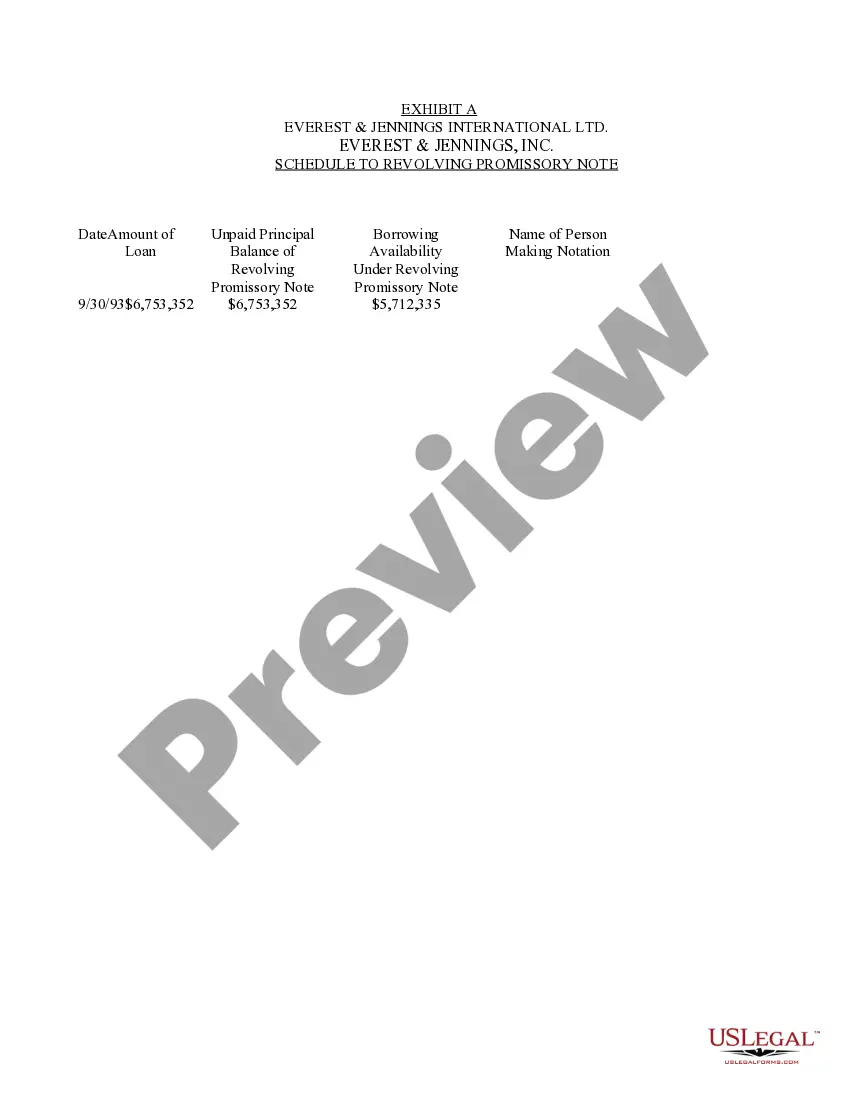

Title: An Overview of the Alaska Form of Revolving Promissory Note: Types and Key Features Introduction: Alaska's Form of Revolving Promissory Note is a legal document used in financial transactions where a lender agrees to provide a revolving line of credit to a borrower. This article aims to provide a detailed description of the Alaska Form of Revolving Promissory Note, including the types and essential components. Types of Alaska Form of Revolving Promissory Note: 1. Traditional Revolving Promissory Note: The traditional form of the Alaska Revolving Promissory Note allows the borrower to borrow, repay, and re-borrow funds as needed within the agreed credit limit. Interest is typically charged based on the outstanding balance, creating flexibility for the borrower. 2. Secured Revolving Promissory Note: Under this variation, the lender requires the borrower to provide collateral to secure the revolving line of credit. Collateral may include real estate, vehicles, equipment, or any valuable asset that holds sufficient value to cover the debt in case of default. 3. Unsecured Revolving Promissory Note: Unlike the secured version, this type does not require any specific collateral to obtain the revolving line of credit. The lender relies solely on the borrower's creditworthiness and financial history to determine eligibility and set the terms. Key Features of the Alaska Form of Revolving Promissory Note: 1. Principal Amount: The principal amount refers to the total credit limit offered to the borrower. It determines the maximum borrowing capacity within the revolving credit facility. 2. Interest Rate and Calculation: The interest rate is determined by the lender and is usually specified as an annual percentage rate (APR). This rate is applied to the outstanding balance, which fluctuates as the borrower borrows and repays funds. The interest calculation method, such as simple interest or compound interest, may also be included. 3. Revolving Credit Period: This describes the duration during which the borrower can utilize the revolving line of credit. It is typically set for a certain period, after which the borrower may need to renegotiate terms or seek a renewal. 4. Repayment Terms: The repayment terms specify how repayments are to be made. This may include minimum monthly payments, repayment periods, and any applicable late payment penalties or fees. 5. Default Provisions: Alaskan Forms of Revolving Promissory Notes outline the consequences of default, including additional fees, penalties, and the potential triggering of the acceleration clause, allowing the lender to demand immediate repayment of the outstanding balance. Conclusion: The Alaska Form of Revolving Promissory Note provides a robust legal framework to facilitate revolving lines of credit between lenders and borrowers. The different types of these promissory notes cater to various borrowing needs, offering flexibility, security, and credit opportunities. Understanding the key components and features of these notes is crucial for borrowers and lenders alike to create a transparent and fair financial arrangement.

Alaska Form of Revolving Promissory Note

Description

How to fill out Alaska Form Of Revolving Promissory Note?

US Legal Forms - one of the greatest libraries of authorized types in the States - offers an array of authorized papers web templates you can obtain or produce. Making use of the web site, you can get 1000s of types for business and individual reasons, sorted by categories, suggests, or search phrases.You will discover the most up-to-date types of types like the Alaska Form of Revolving Promissory Note within minutes.

If you have a subscription, log in and obtain Alaska Form of Revolving Promissory Note from your US Legal Forms local library. The Download option will show up on each kind you see. You have accessibility to all earlier saved types inside the My Forms tab of your own accounts.

If you want to use US Legal Forms initially, allow me to share straightforward guidelines to help you started:

- Ensure you have picked the proper kind for your area/region. Select the Preview option to check the form`s information. See the kind information to actually have selected the right kind.

- When the kind does not satisfy your demands, utilize the Research area near the top of the screen to get the one that does.

- In case you are happy with the form, verify your choice by simply clicking the Get now option. Then, pick the pricing prepare you like and provide your credentials to sign up for an accounts.

- Method the deal. Utilize your Visa or Mastercard or PayPal accounts to complete the deal.

- Pick the file format and obtain the form on your system.

- Make modifications. Fill out, change and produce and indication the saved Alaska Form of Revolving Promissory Note.

Every single format you put into your money lacks an expiration time and is also the one you have permanently. So, if you wish to obtain or produce yet another backup, just visit the My Forms segment and click on about the kind you require.

Gain access to the Alaska Form of Revolving Promissory Note with US Legal Forms, by far the most considerable local library of authorized papers web templates. Use 1000s of skilled and status-particular web templates that satisfy your small business or individual needs and demands.