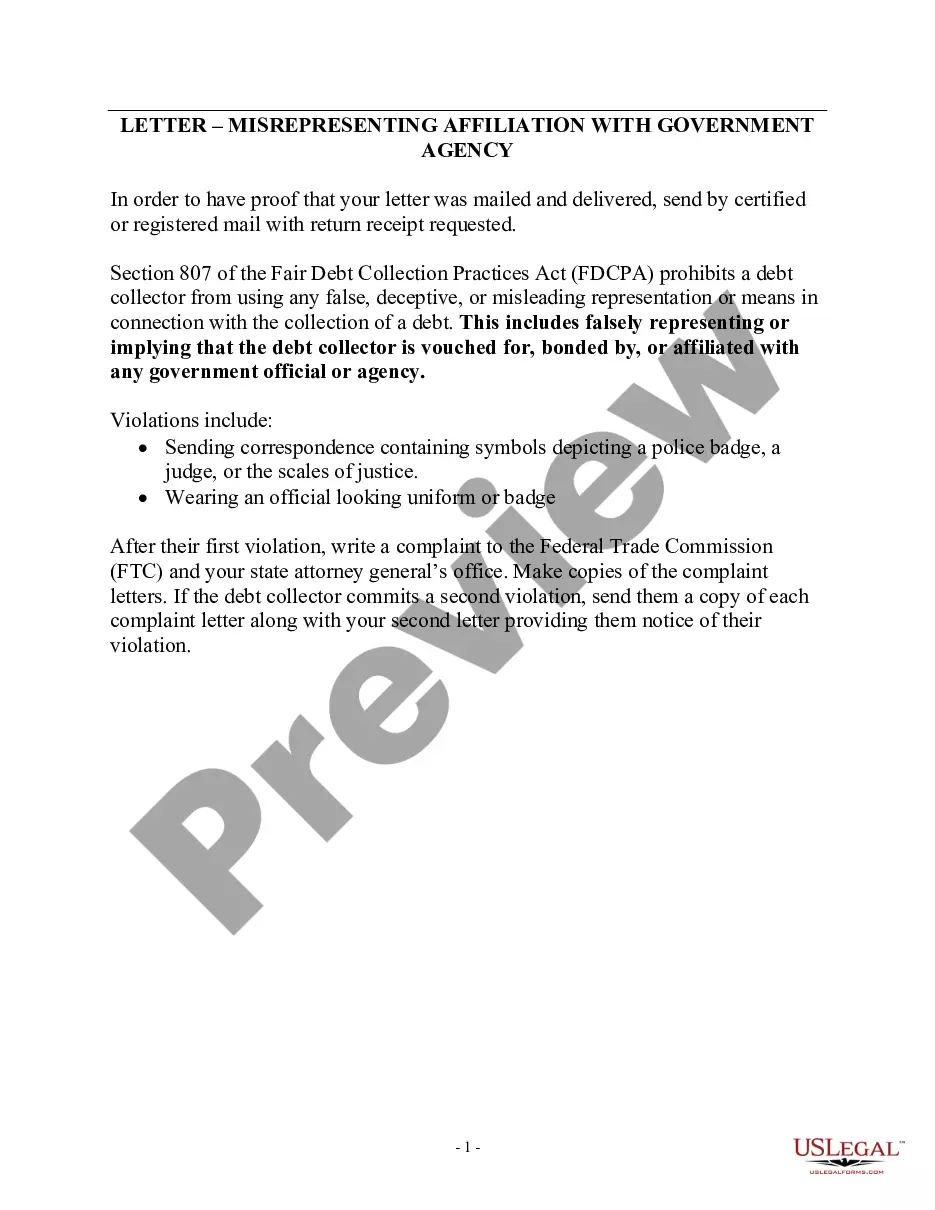

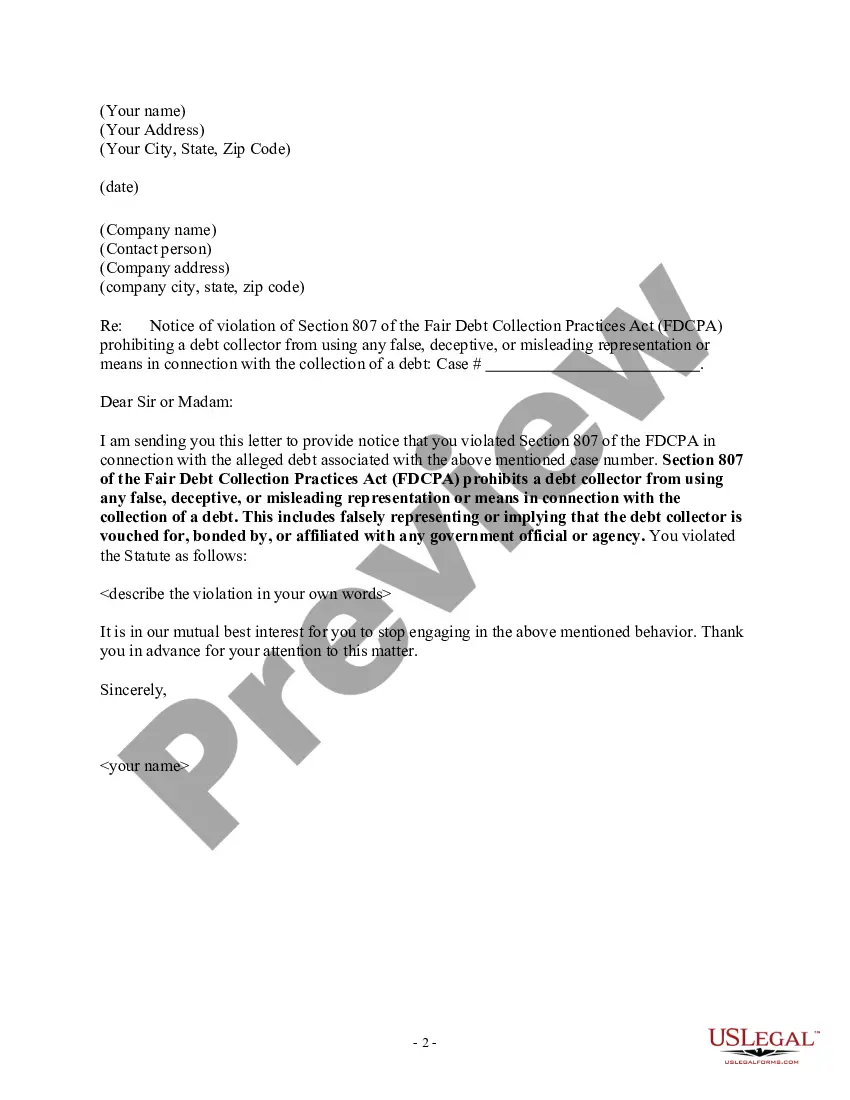

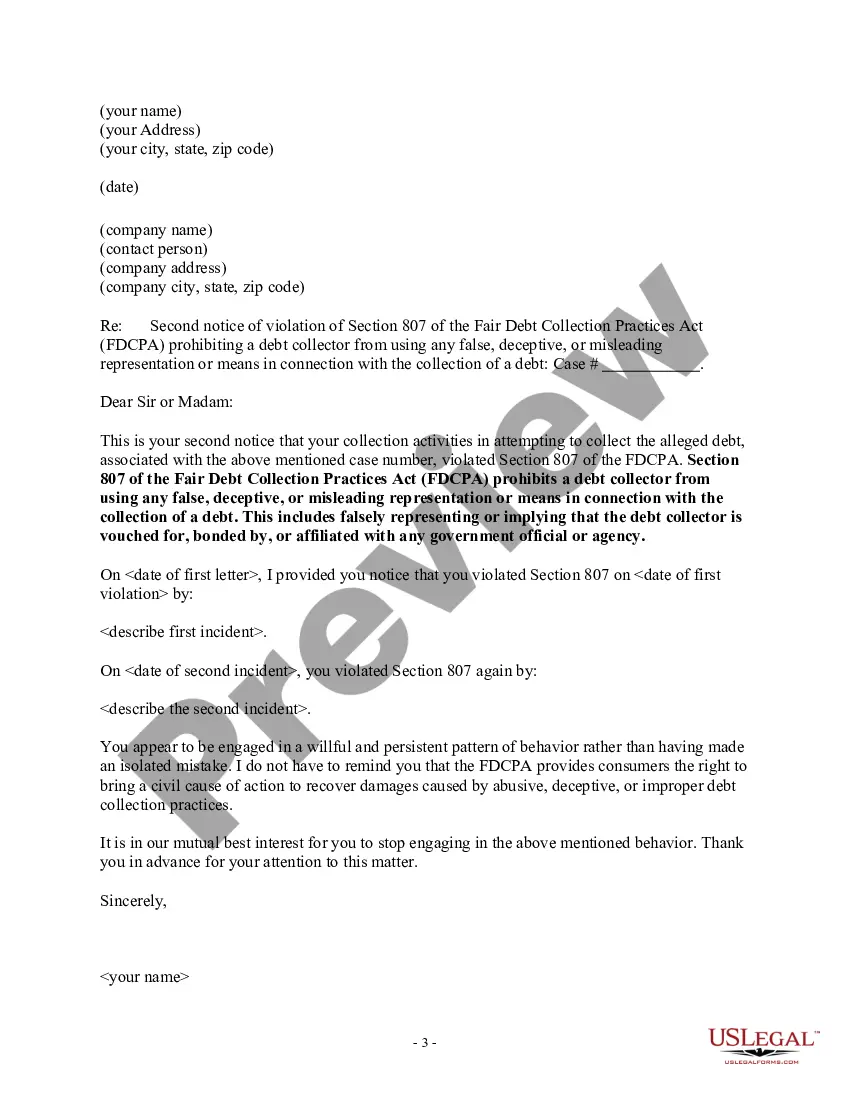

Alaska Notice of Violation of Fair Debt Act - Creditor Misrepresented Himself

Description

How to fill out Alaska Notice Of Violation Of Fair Debt Act - Creditor Misrepresented Himself?

It is possible to spend hours on-line looking for the authorized file design that suits the federal and state needs you need. US Legal Forms gives a large number of authorized forms that are examined by pros. It is simple to acquire or produce the Alaska Notice of Violation of Fair Debt Act - Creditor Misrepresented Himself from your services.

If you already possess a US Legal Forms bank account, it is possible to log in and click the Obtain button. Following that, it is possible to complete, revise, produce, or signal the Alaska Notice of Violation of Fair Debt Act - Creditor Misrepresented Himself. Every single authorized file design you get is the one you have for a long time. To have yet another copy of any obtained type, visit the My Forms tab and click the corresponding button.

If you are using the US Legal Forms web site for the first time, adhere to the simple directions beneath:

- Initially, ensure that you have selected the correct file design for your region/metropolis of your liking. See the type description to ensure you have picked out the correct type. If available, use the Review button to look through the file design also.

- In order to get yet another model of the type, use the Lookup field to discover the design that meets your requirements and needs.

- Upon having located the design you would like, click Purchase now to carry on.

- Pick the costs strategy you would like, type in your accreditations, and register for an account on US Legal Forms.

- Complete the financial transaction. You may use your credit card or PayPal bank account to fund the authorized type.

- Pick the file format of the file and acquire it to your product.

- Make changes to your file if necessary. It is possible to complete, revise and signal and produce Alaska Notice of Violation of Fair Debt Act - Creditor Misrepresented Himself.

Obtain and produce a large number of file themes utilizing the US Legal Forms Internet site, which provides the largest variety of authorized forms. Use skilled and status-specific themes to tackle your organization or personal demands.

Form popularity

FAQ

Debt collectors are legally required to send one within five days of first contact. You have within 30 days from receiving a debt validation letter to send a debt verification letter. Here's the important part: You have just 30 days to respond to a debt validation letter with your debt verification letter.

Failing to respond to a Debt Validation Letter while continuing to collect on the debt is a direct violation of the FDCPA. You can report a debt collector's failure to respond to your state's attorney general, the Consumer Financial Protection Bureau (CFPB), or the FTC.

If they can't validate the debt, the credit bureau cannot list it as a negative mark on your credit report. With debt validation, you're requesting that the debt collector proves they have the legal right to collect the money. It also confirms that you agreed to pay the debt and the amount owed is accurate.

Federal law says that after receiving written notice of a debt, consumers have a 30-day window to respond with a debt dispute letter.

If a debt collector violates the FDCPA, you may sue that collector in state or federal court. You can even sue in small claims court. You must do this within one year from the date on which the violation occurred.

Unless your state law provides otherwise, the FDCPA only requires debt collectors, not original creditors, to verify debts in certain circumstances. This requirement includes law firms that are routinely engaged in collecting debts.

Debt collectors are legally required to send one within five days of first contact. You have within 30 days from receiving a debt validation letter to send a debt verification letter. Here's the important part: You have just 30 days to respond to a debt validation letter with your debt verification letter.

If a debt collector fails to verify the debt but continues to go after you for payment, you have the right to sue that debt collector in federal or state court. You might be able to get $1,000 per lawsuit, plus actual damages, attorneys' fees, and court costs.

If a debt collector fails to verify the debt but continues to go after you for payment, you have the right to sue that debt collector in federal or state court. You might be able to get $1,000 per lawsuit, plus actual damages, attorneys' fees, and court costs.

You have 30 days to dispute a debt or part of a debt within 30 days from when you first receive the required information from the debt collector.