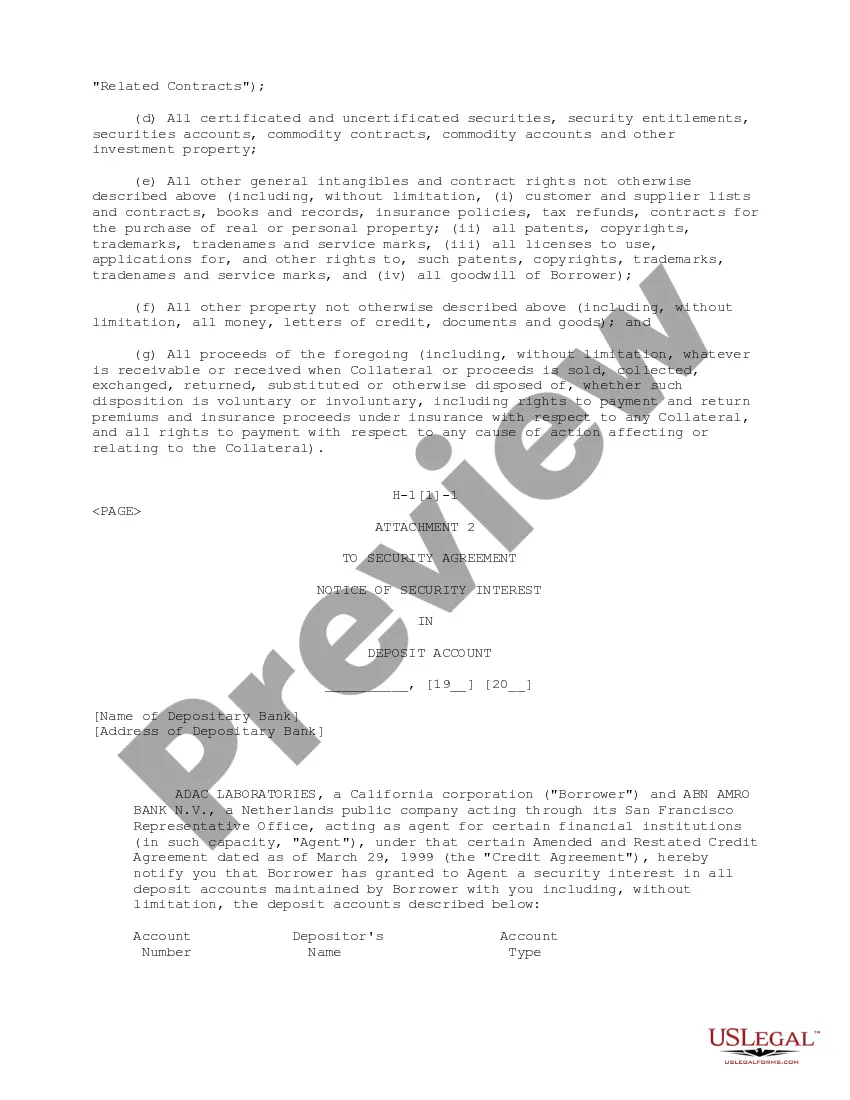

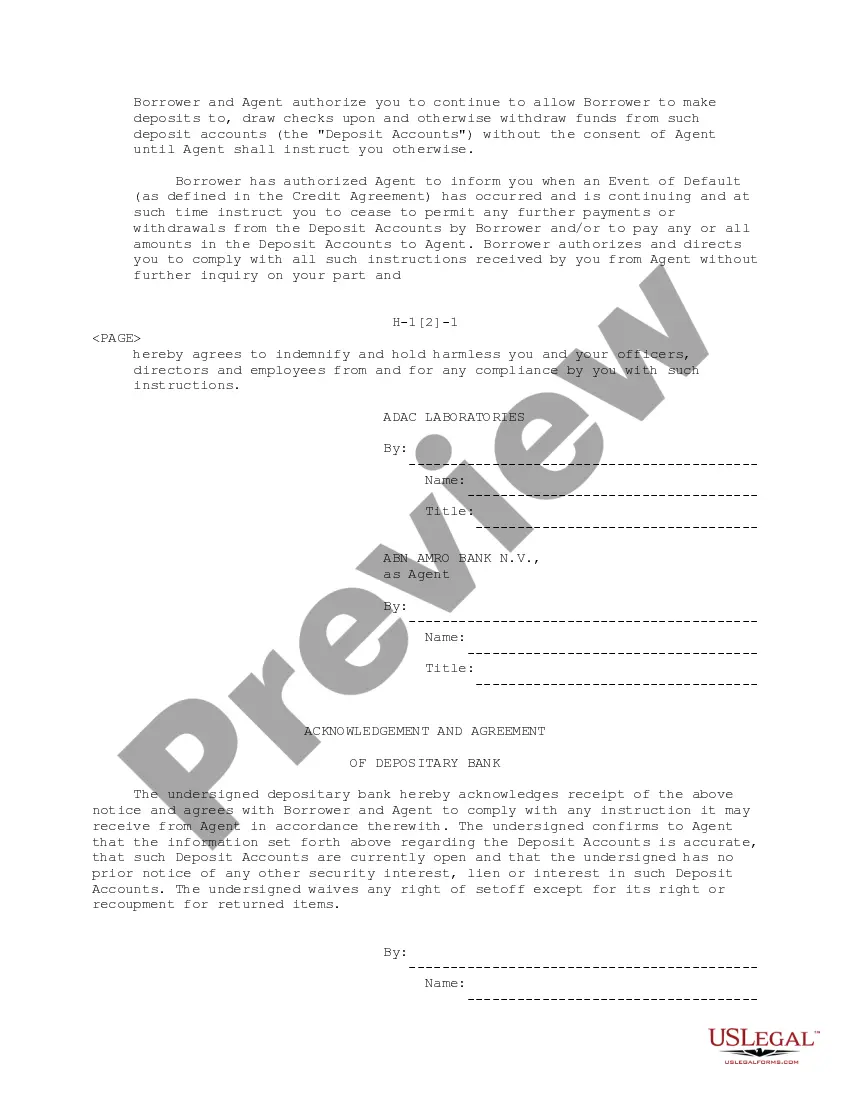

The Alaska Borrower Security Agreement regarding the extension of credit facilities is a legally binding document that outlines the terms and conditions between a borrower and a lender in Alaska. This agreement is designed to protect the interests of the lender by providing additional security for the extension of credit facilities, ensuring the borrower's obligation to repay the loan. Keywords: Alaska, Borrower Security Agreement, extension of credit facilities, legally binding document, terms and conditions, borrower, lender, protect interests, additional security, obligation, repay loan. There can be different types of Alaska Borrower Security Agreements regarding the extension of credit facilities. Some examples include: 1. Real Estate Mortgage: This type of agreement involves the borrower providing a mortgage on a specific property they own or plan to purchase. The property acts as collateral for the loan, providing the lender with security in case the borrower defaults on the loan. 2. Personal Guarantee: In this type of agreement, the borrower offers their personal assets or guarantees from third-party individuals (such as co-signers or guarantors) as security for the loan. This ensures that if the borrower fails to repay the loan, the lender can pursue these assets to recover the outstanding amount. 3. Pledge of Assets: This agreement involves the borrower pledging specific assets such as equipment, vehicles, or inventory as collateral for the credit facilities. If the borrower defaults, the lender can seize and sell these pledged assets to recover their funds. 4. Assignment of Accounts Receivables: In this type of agreement, the borrower assigns their existing or future accounts receivables to the lender as collateral for the loan. This means that the borrower's customers' payments are directly redirected to the lender until the loan is repaid, providing added security to the lender. 5. Stock Pledge: This agreement involves the borrower pledging their stocks or shares in a company as collateral for the loan. If the borrower defaults, the lender can take ownership of these shares and sell them to recover their funds. It is important for both borrowers and lenders in Alaska to carefully review and understand the specific terms and conditions outlined in the Borrower Security Agreement regarding the extension of credit facilities to ensure both parties' rights and obligations are clearly defined and protected.

Alaska Borrower Security Agreement regarding the extension of credit facilities

Description

How to fill out Alaska Borrower Security Agreement Regarding The Extension Of Credit Facilities?

Choosing the right legitimate papers template can be a have difficulties. Obviously, there are a lot of layouts available on the Internet, but how will you get the legitimate form you will need? Take advantage of the US Legal Forms internet site. The support provides a huge number of layouts, for example the Alaska Borrower Security Agreement regarding the extension of credit facilities, that can be used for organization and private requirements. Each of the kinds are examined by professionals and meet up with state and federal demands.

If you are presently authorized, log in for your accounts and click the Down load switch to find the Alaska Borrower Security Agreement regarding the extension of credit facilities. Make use of your accounts to appear throughout the legitimate kinds you have acquired formerly. Go to the My Forms tab of your own accounts and obtain one more backup of the papers you will need.

If you are a fresh consumer of US Legal Forms, listed below are simple recommendations that you can comply with:

- Very first, make certain you have selected the proper form to your metropolis/region. It is possible to look over the shape while using Review switch and read the shape explanation to ensure this is the best for you.

- When the form is not going to meet up with your expectations, take advantage of the Seach industry to obtain the correct form.

- When you are certain the shape is suitable, click the Buy now switch to find the form.

- Select the rates plan you would like and enter the essential info. Create your accounts and pay for an order with your PayPal accounts or credit card.

- Select the document format and obtain the legitimate papers template for your product.

- Total, edit and printing and sign the attained Alaska Borrower Security Agreement regarding the extension of credit facilities.

US Legal Forms will be the most significant collection of legitimate kinds where you can see a variety of papers layouts. Take advantage of the service to obtain professionally-created documents that comply with express demands.