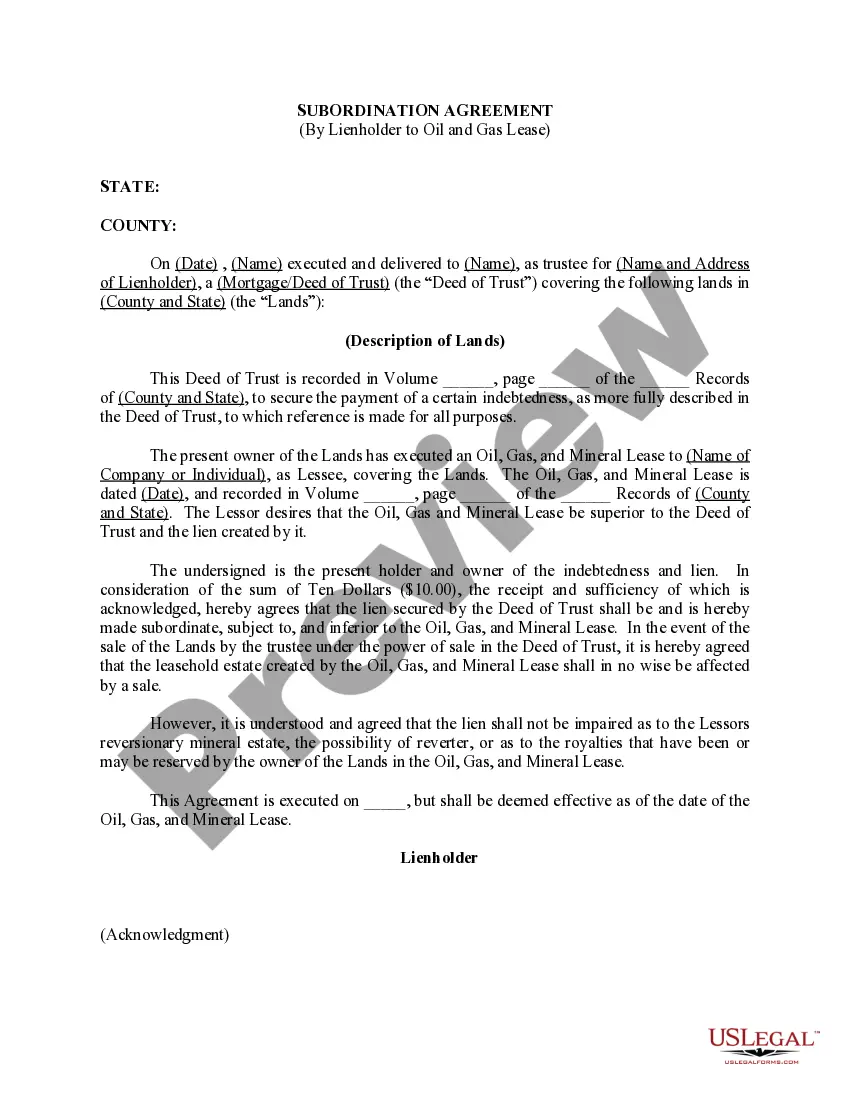

Alaska Subordination of Lien (Deed of Trust/Mortgage)

Description

How to fill out Subordination Of Lien (Deed Of Trust/Mortgage)?

Choosing the best lawful papers web template might be a have difficulties. Needless to say, there are a lot of templates available online, but how can you obtain the lawful type you will need? Utilize the US Legal Forms web site. The assistance delivers 1000s of templates, including the Alaska Subordination of Lien (Deed of Trust/Mortgage), that you can use for business and private demands. All the types are inspected by experts and meet up with state and federal requirements.

Should you be presently signed up, log in for your bank account and click the Download button to obtain the Alaska Subordination of Lien (Deed of Trust/Mortgage). Make use of bank account to check from the lawful types you may have purchased earlier. Check out the My Forms tab of your own bank account and get yet another copy in the papers you will need.

Should you be a brand new consumer of US Legal Forms, listed here are straightforward recommendations that you can follow:

- First, make certain you have chosen the appropriate type to your area/county. You are able to look over the shape using the Preview button and look at the shape outline to make sure it will be the best for you.

- In case the type is not going to meet up with your requirements, make use of the Seach area to find the right type.

- Once you are certain the shape is suitable, go through the Buy now button to obtain the type.

- Choose the rates prepare you want and type in the necessary information and facts. Design your bank account and pay for the transaction with your PayPal bank account or bank card.

- Pick the file file format and download the lawful papers web template for your gadget.

- Full, revise and print and indicator the received Alaska Subordination of Lien (Deed of Trust/Mortgage).

US Legal Forms is the most significant catalogue of lawful types that you can discover a variety of papers templates. Utilize the service to download appropriately-manufactured documents that follow state requirements.

Form popularity

FAQ

Subordination agreements may be included in existing deeds of trust or may be outlined in an independent contract. In situations where two deeds of trust are being recorded concurrently, the lien priority is typically handled by instructing the title company as to which security instrument will be recorded first.

Who Executes a Subordination Agreement? The new lender prepares the subordination agreement in conjunction with the subordinating lienholder. Then, the parties typically sign the agreement.

Lien subordination refers to the order in which claims on collateral are prioritized. This takes place most often among senior secured lenders and does not imply that one tranche of senior debt has payment preference over another.

A subordinated loan agreement (SLA) must be filed with NFA at least ten days prior to the proposed effective date of the agreement.

A subordination agreement prioritizes debts, ranking one behind another for purposes of collecting repayment from a debtor in the event of foreclosure or bankruptcy. A second-in-line creditor collects only when and if the priority creditor has been fully paid.

This Security Instrument secures to Lender (i) the. repayment of the Loan, and all renewals, extensions, and modifications of the Note, and (ii) the performance. of Borrower's covenants and agreements under this Security Instrument and the Note.

The creditor usually will require the debtor to sign a subordination agreement which ensures they get paid before other creditors, ensuring they are not taking on high risks.

The states that use a deed of trust are: Alaska. Arizona. California.

")