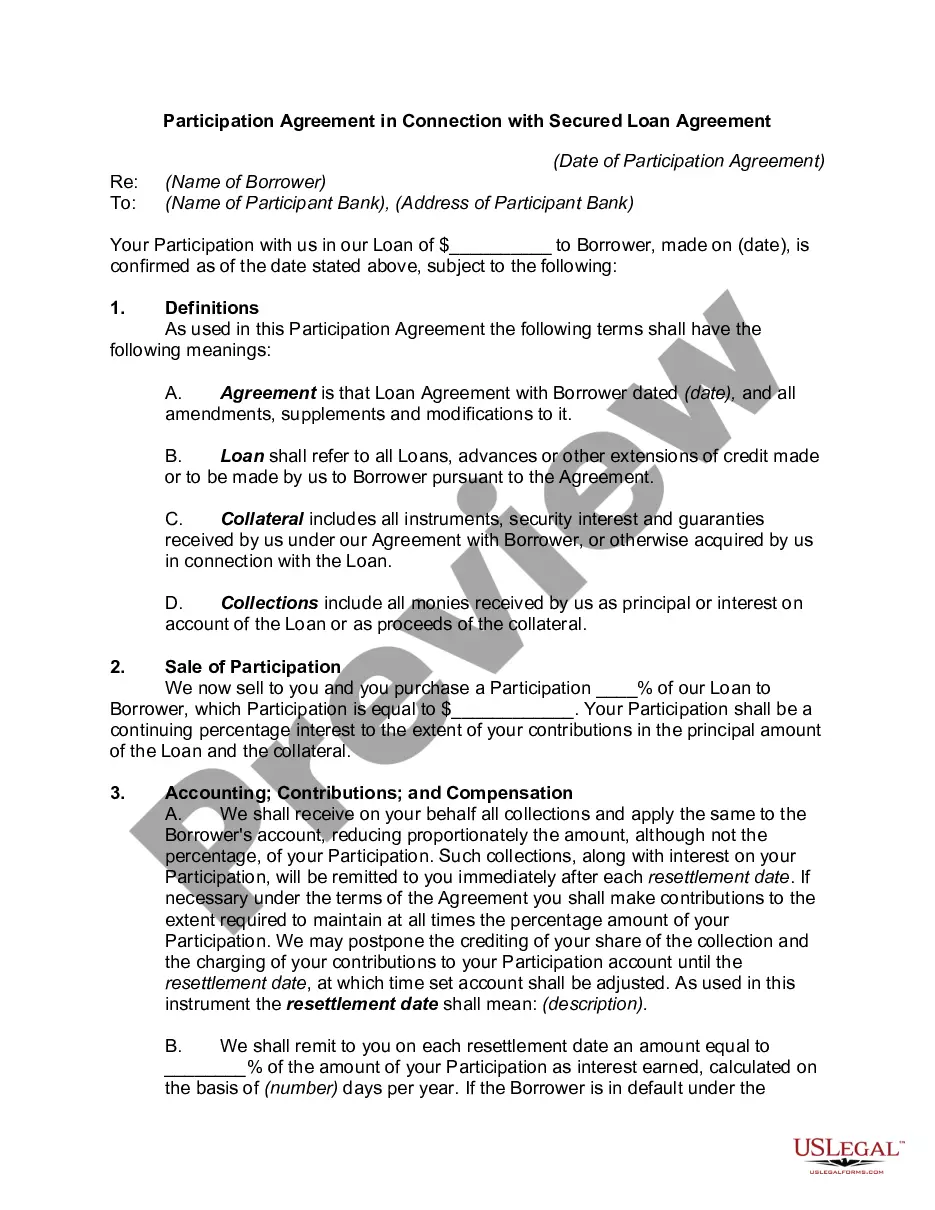

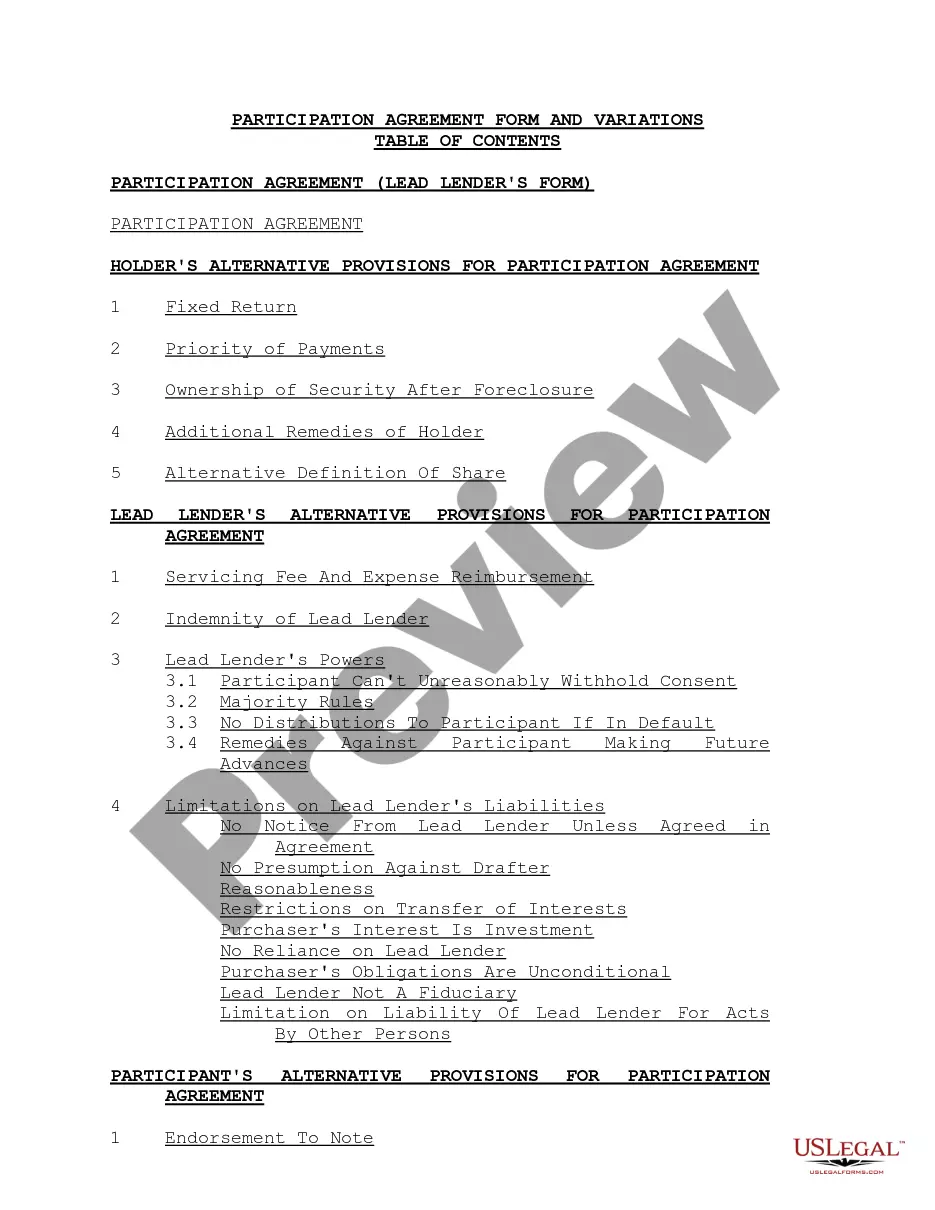

Are you presently within a situation where you will need documents for both organization or specific purposes just about every day time? There are plenty of legitimate record templates available online, but discovering kinds you can depend on is not effortless. US Legal Forms provides 1000s of type templates, just like the Alabama Participating or Participation Loan Agreement in Connection with Secured Loan Agreement, that happen to be written in order to meet federal and state needs.

Should you be currently knowledgeable about US Legal Forms web site and have an account, just log in. Next, you may down load the Alabama Participating or Participation Loan Agreement in Connection with Secured Loan Agreement design.

Should you not provide an accounts and need to start using US Legal Forms, adopt these measures:

- Get the type you need and make sure it is for the proper town/state.

- Use the Preview option to review the form.

- Read the outline to ensure that you have chosen the appropriate type.

- In case the type is not what you`re looking for, use the Search discipline to obtain the type that meets your needs and needs.

- Whenever you obtain the proper type, simply click Acquire now.

- Select the pricing prepare you desire, fill out the necessary info to make your account, and pay money for the transaction making use of your PayPal or Visa or Mastercard.

- Choose a handy file file format and down load your copy.

Locate all of the record templates you may have bought in the My Forms food list. You can get a extra copy of Alabama Participating or Participation Loan Agreement in Connection with Secured Loan Agreement whenever, if needed. Just click the necessary type to down load or print out the record design.

Use US Legal Forms, one of the most extensive assortment of legitimate varieties, in order to save time and prevent errors. The service provides expertly manufactured legitimate record templates that can be used for a selection of purposes. Create an account on US Legal Forms and start generating your daily life a little easier.