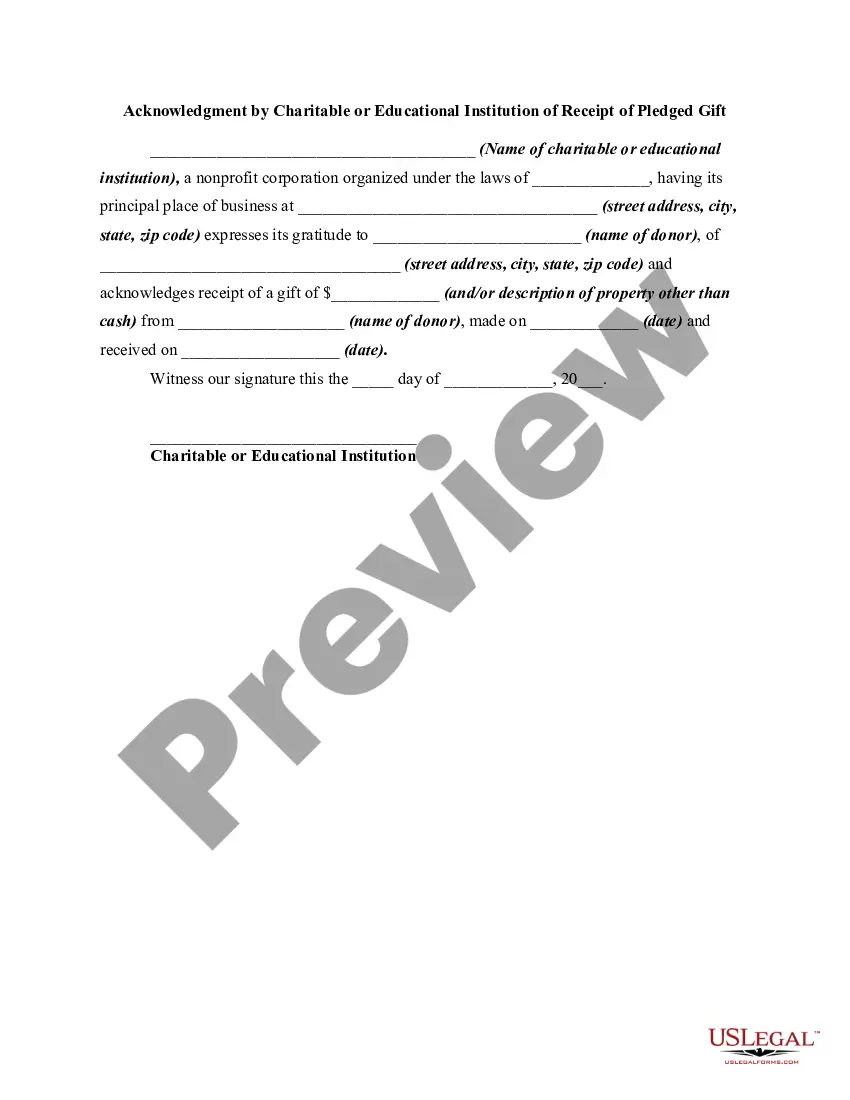

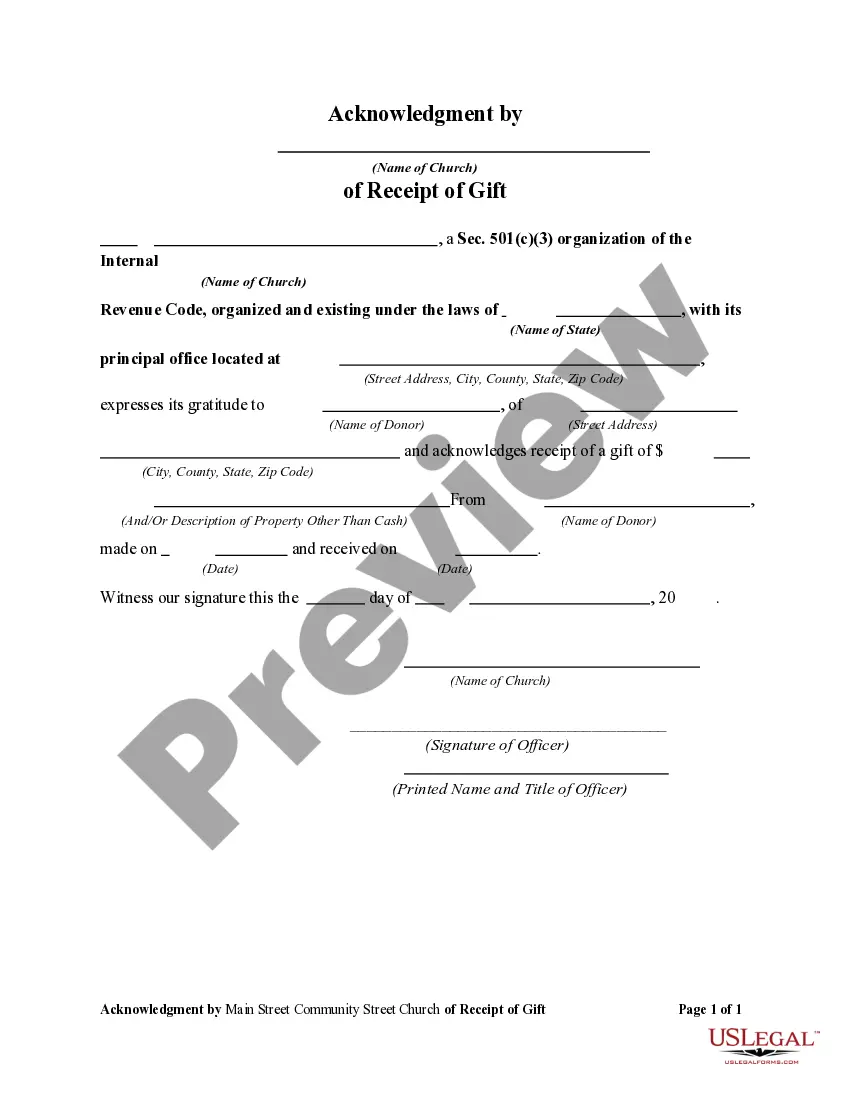

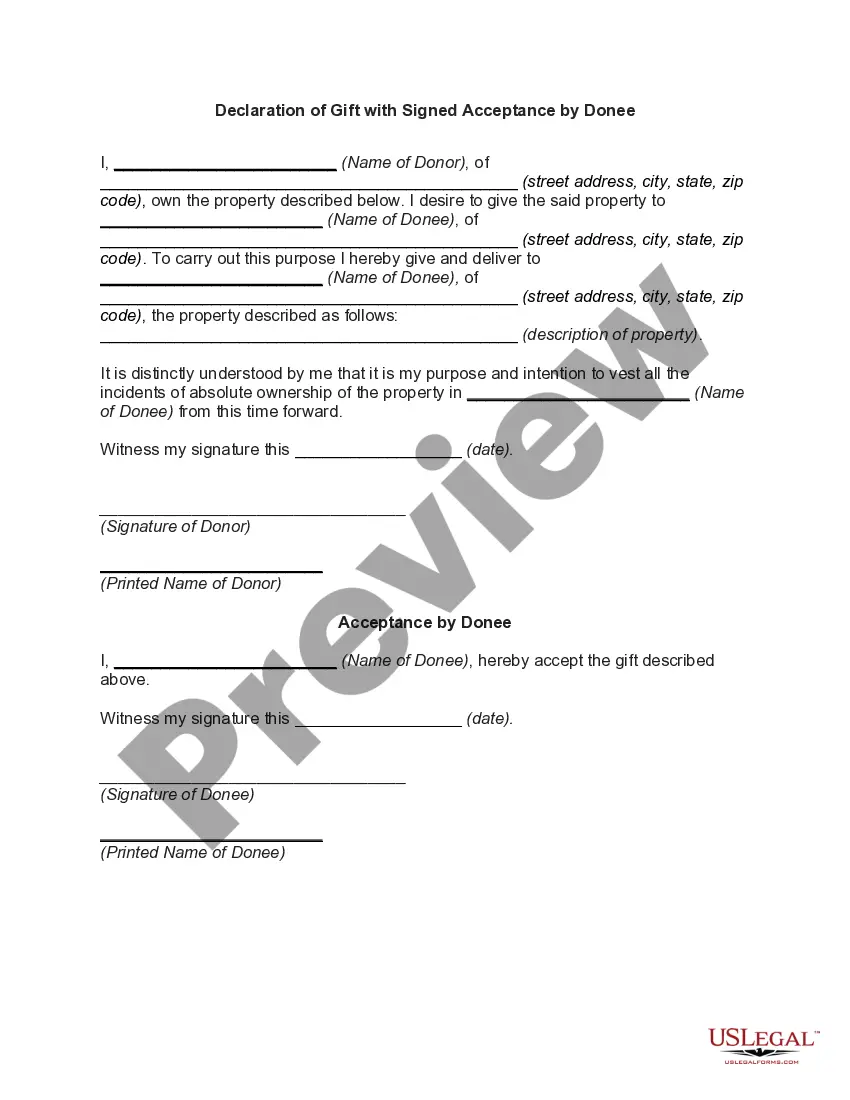

Alabama Acknowledgment by Charitable or Educational Institution of Receipt of Gift

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Acknowledgment By Charitable Or Educational Institution Of Receipt Of Gift?

Selecting the most suitable legal documents template can be a challenge. Of course, there are numerous designs accessible online, but how can you find the legal form you require? Utilize the US Legal Forms website. The platform offers thousands of designs, including the Alabama Acknowledgment by Charitable or Educational Institution of Receipt of Gift, which you can use for both business and personal purposes. All the forms are reviewed by experts and comply with state and federal regulations.

If you are already registered, Log In to your account and click the Download button to access the Alabama Acknowledgment by Charitable or Educational Institution of Receipt of Gift. Use your account to view the legal forms you have previously purchased. Visit the My documents section of your account to obtain another copy of the documents you need.

If you are a new user of US Legal Forms, here are simple steps you can follow: First, make sure you have selected the correct form for your city/county. You can review the form by clicking the Review button and examining the form details to confirm it is indeed the right one for you. If the form does not satisfy your requirements, use the Search field to find the appropriate form. Once you are sure that the form is correct, click the Get now button to access the form. Choose the pricing plan you want and enter the necessary details. Create your account and pay for your order using your PayPal account or credit card.

In summary, US Legal Forms provides an extensive collection of legal templates that can ease the process of finding the right documents for your needs.

- Select the file format and download the legal document template to your device.

- Complete, modify, print, and sign the obtained Alabama Acknowledgment by Charitable or Educational Institution of Receipt of Gift.

- US Legal Forms is the largest repository of legal forms where you can find a wide range of document templates.

- Utilize the service to acquire professionally crafted documents that adhere to state requirements.

- Ensure compliance with all necessary legal standards and regulations.

Form popularity

FAQ

In Alabama, teachers can accept gifts from students, but there is a limit to ensure that the gifts do not create any ethical dilemmas. Typically, gifts should not exceed a nominal value, which helps maintain professionalism in the classroom. When teachers receive significant gifts, it’s advisable to have an Alabama Acknowledgment by Charitable or Educational Institution of Receipt of Gift to document these transactions appropriately.

In Alabama, the next of kin is typically defined as the closest living relatives of a deceased person. This usually includes spouses, children, parents, and siblings. Knowing who qualifies as next of kin is important in matters involving inheritance and the Alabama Acknowledgment by Charitable or Educational Institution of Receipt of Gift, especially when gifts are involved.

Alabama Code 36 25 7 outlines the requirements for public officials regarding the acceptance of gifts. This law aims to prevent conflicts of interest and ensure transparency in government dealings. Understanding this code is crucial for charitable institutions that frequently receive gifts, as it relates to the Alabama Acknowledgment by Charitable or Educational Institution of Receipt of Gift.

In Alabama, a bill of sale is typically required for a gifted car to legally transfer ownership. This document serves as proof of the transaction and helps avoid future complications. When using an Alabama Acknowledgment by Charitable or Educational Institution of Receipt of Gift, ensure that the gift is well documented to protect both the giver and the recipient.

Yes, once a gift is given and accepted, it becomes the legal property of the recipient. This means that the recipient has full rights to use, sell, or transfer the gift. When considering significant gifts, such as those acknowledged by the Alabama Acknowledgment by Charitable or Educational Institution of Receipt of Gift, it is essential to document the transfer to avoid any disputes later.

In Alabama, inheritance laws dictate how a person's estate is distributed after their death. If a person passes away without a will, state laws determine the distribution among heirs. The Alabama Acknowledgment by Charitable or Educational Institution of Receipt of Gift can play a role in documenting contributions to these institutions, ensuring clarity in the distribution of assets.

To acknowledge receipt of a donation, send a formal letter or receipt to the donor that includes essential details like the donor's name, the donation amount, and the date received. This communication fosters goodwill and encourages future contributions. By adhering to the Alabama Acknowledgment by Charitable or Educational Institution of Receipt of Gift standards, you ensure that your acknowledgment is both effective and compliant with tax regulations.

A contemporaneous written acknowledgment of a charitable gift must include the name of the organization, the donation date, the amount contributed, and a statement indicating whether any goods or services were exchanged. This acknowledgment must be provided to the donor within a reasonable timeframe, typically by the end of the year in which the donation was made. Following the Alabama Acknowledgment by Charitable or Educational Institution of Receipt of Gift requirements ensures proper tax documentation for donors.

To fill out a donation receipt, start with the donor's name and address, followed by the date of the contribution. Include details about the donation, such as the amount and the type of property donated, if applicable. For proper documentation, ensure that the receipt aligns with the Alabama Acknowledgment by Charitable or Educational Institution of Receipt of Gift guidelines to help the donor claim their tax benefits.

An example of a written acknowledgment for a charitable contribution includes a letter from the charitable organization that states the amount of the donation and confirms that no goods or services were provided in exchange. This acknowledgment serves as proof for the donor when claiming a tax deduction. For an effective Alabama Acknowledgment by Charitable or Educational Institution of Receipt of Gift, ensure this letter is dated and signed by an authorized representative.