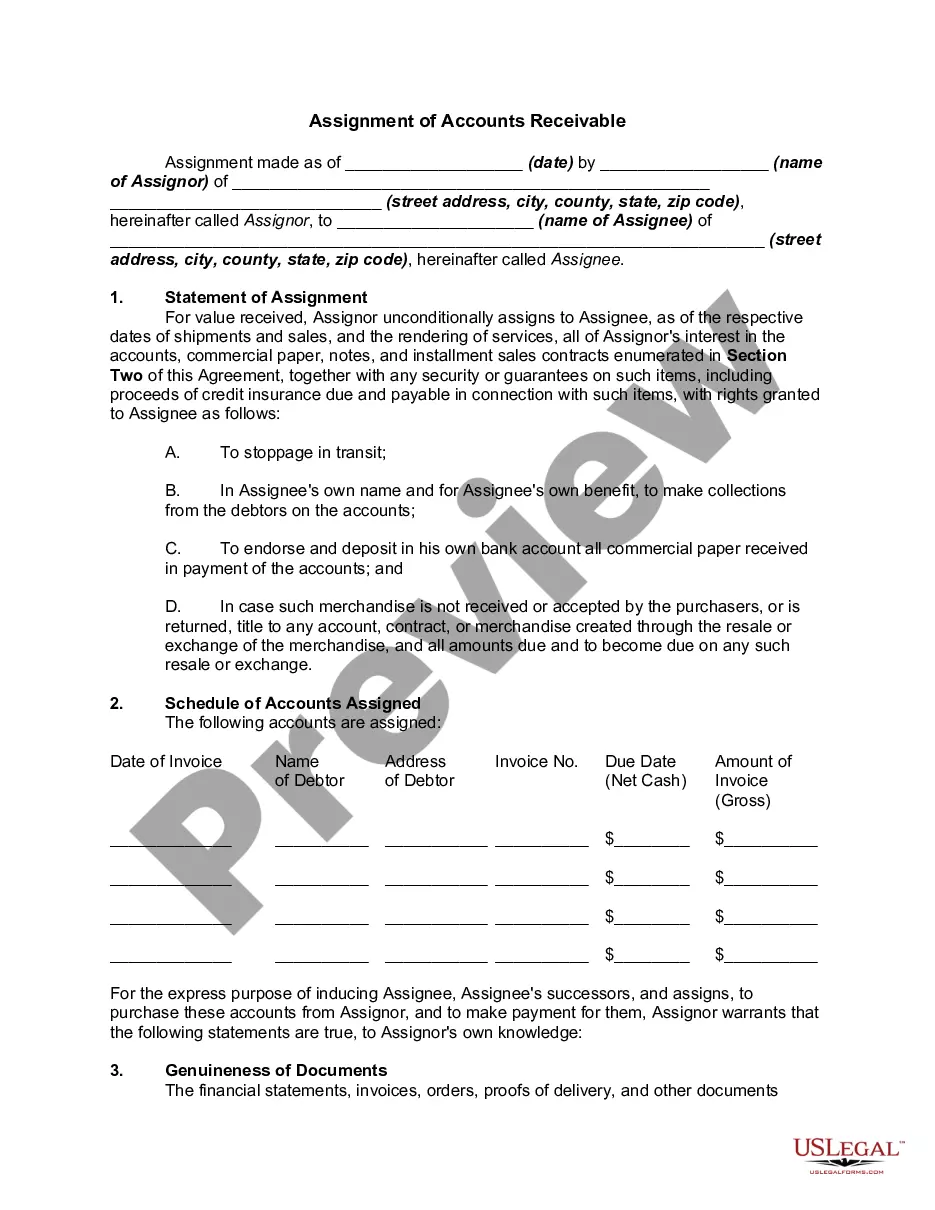

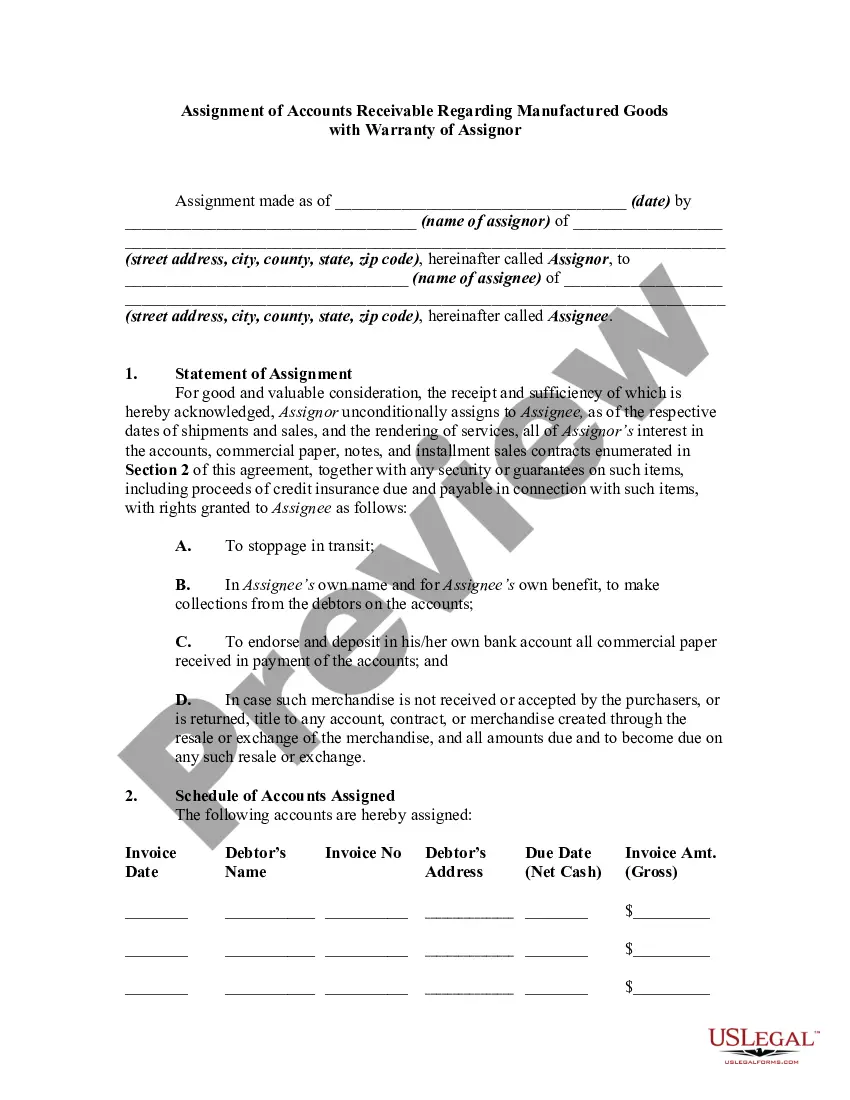

This form is an Assignment of Accounts Receivable. The assignor conveys all interest in the accounts listed on the Attachment included in the form. The accounts represent all outstanding accounts of the assignor from the sale of products or services.

Alabama Accounts Receivable - Assignment

Category:

State:

Multi-State

Control #:

US-00400

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Accounts Receivable - Assignment?

US Legal Forms - one of the largest collections of authentic forms in the United States - provides a broad selection of valid document templates that you can download or print. By using the site, you will find thousands of forms for both business and personal use, organized by categories, states, or keywords. You can access the latest versions of forms such as the Alabama Accounts Receivable - Assignment within moments.

If you already have an account, Log In and download the Alabama Accounts Receivable - Assignment from the US Legal Forms library. The Download button appears on each form you view. You can access all previously saved forms from the My documents tab in your account.

To use US Legal Forms for the first time, here are simple steps to help you get started: Ensure you have selected the correct form for your specific city/county. Click the Preview button to review the form's details. Check the form details to verify that you have selected the right form. If the form does not meet your requirements, use the Search field at the top of the screen to find one that does. If you are satisfied with the form, confirm your selection by clicking the Purchase now button. Then, choose the pricing plan you prefer and provide your information to register for an account. Process the payment. Use your credit card or PayPal account to complete the transaction. Select the format and download the form to your device. Make adjustments. Fill out, modify, and print and sign the saved Alabama Accounts Receivable - Assignment. Each template you added to your account has no expiration date and is yours indefinitely. So, if you want to download or print another copy, simply go to the My documents section and click on the form you need.

- Access the Alabama Accounts Receivable - Assignment with US Legal Forms, the most extensive collection of authentic document templates.

- Utilize a vast number of professional and state-specific templates that meet your business or personal needs.

Form popularity

FAQ

Certain entities are exempt from paying business privilege tax in Alabama. These typically include non-profit organizations, government entities, and businesses with minimal revenue. Understanding these exemptions can help you manage your Alabama Accounts Receivable - Assignment more effectively. For detailed guidance on exemptions, uslegalforms offers valuable resources that clarify your obligations and rights.

A BPT account number is a unique identifier assigned to businesses in Alabama for the Business Privilege Tax. This number is essential for any business conducting operations, as it ties directly to your tax obligations. If you need assistance with your BPT account number or managing your Alabama Accounts Receivable - Assignment, consider using resources available on uslegalforms that can help streamline your tax processes.

Filing your Alabama state income tax involves a few straightforward steps. First, gather all necessary documents, including W-2 forms and any other income statements. You can file online using the Alabama Department of Revenue’s e-file system or through a certified tax professional. Using platforms like uslegalforms simplifies the process, providing templates and forms that help you efficiently manage your Alabama Accounts Receivable - Assignment.

To write a check to the Alabama Department of Revenue, start by ensuring you have the correct payee name, which is ‘Alabama Department of Revenue.’ Next, include your account number in the memo section to associate your payment with your Alabama Accounts Receivable - Assignment. Make sure to write the amount clearly and include your signature at the bottom. Finally, mail your check to the appropriate address listed on the department's website.

To solve for accounts receivable, start by reviewing your outstanding invoices and identifying which ones are overdue. Then, implement a follow-up system to remind customers of their obligations. You can also consider using Alabama Accounts Receivable - Assignment to streamline your collections process. This can help ensure you receive payments more quickly and efficiently.

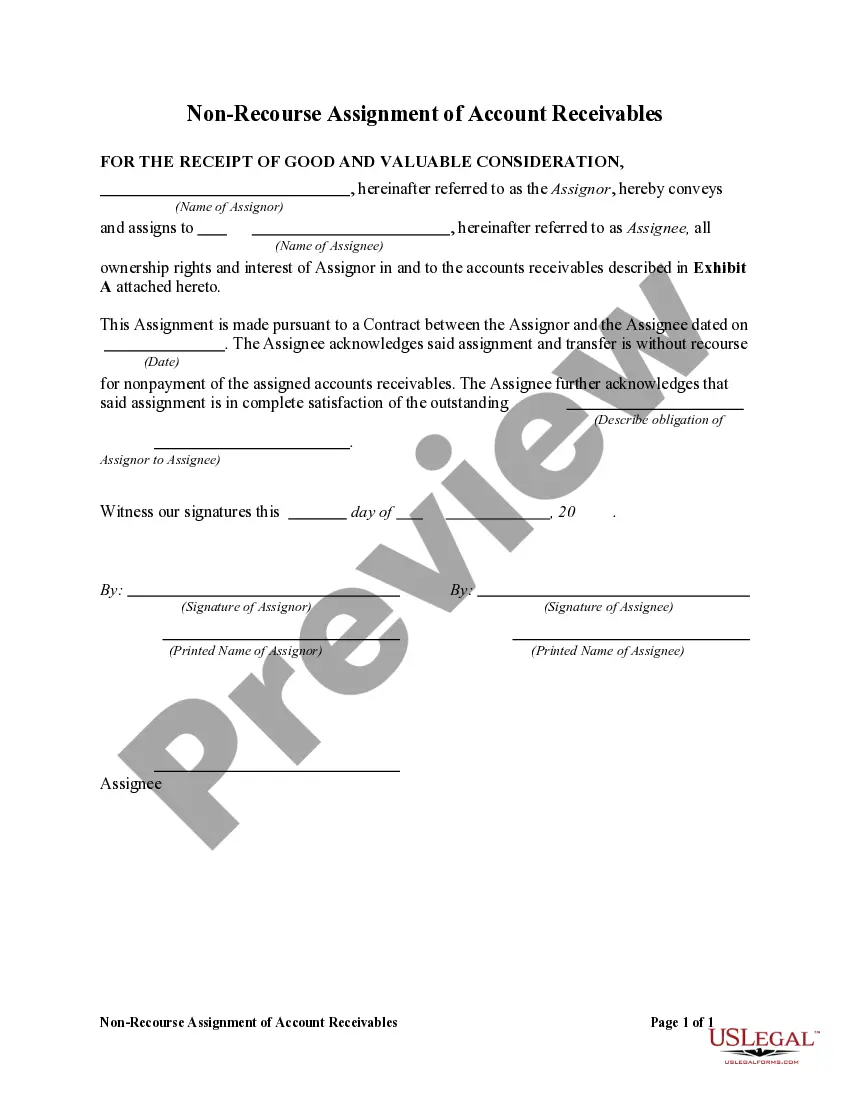

What are the journal entries for assigning Accounts Receivable as collateral for a loan? The entry to record assignment of Accounts Receivable as collateral would be a credit to cash, and a debit to assign Accounts Receivable. The cash account is debited because the company gave up the assigned receivables.

Assignment of accounts receivable is a lending agreement whereby the borrower assigns accounts receivable to the lending institution. In exchange for this assignment of accounts receivable, the borrower receives a loan for a percentage, which could be as high as 100%, of the accounts receivable.

Example of the Assignment of Accounts Receivable ABC Corp. approaches XYZ Bank to obtain financing using its accounts receivable as collateral. XYZ Bank agrees to provide a loan of 85% of the total accounts receivable value, which amounts to $170,000 (85% of $200,000).

In the accounts receivable assignment process, a company assigns receivables to a lending institution to borrow money. The borrower pays interest plus additional fees. The borrowing company retains ownership of the accounts receivable and collects payment from its customers.

Assignment of receivables would mean sale of the lease rentals, not the asset. In that case, the leased asset still remains the property of the assignor ? that is, the assignor has retained the residual interest in the asset. However, it would be different if the lessor sells the asset that has been leased out.