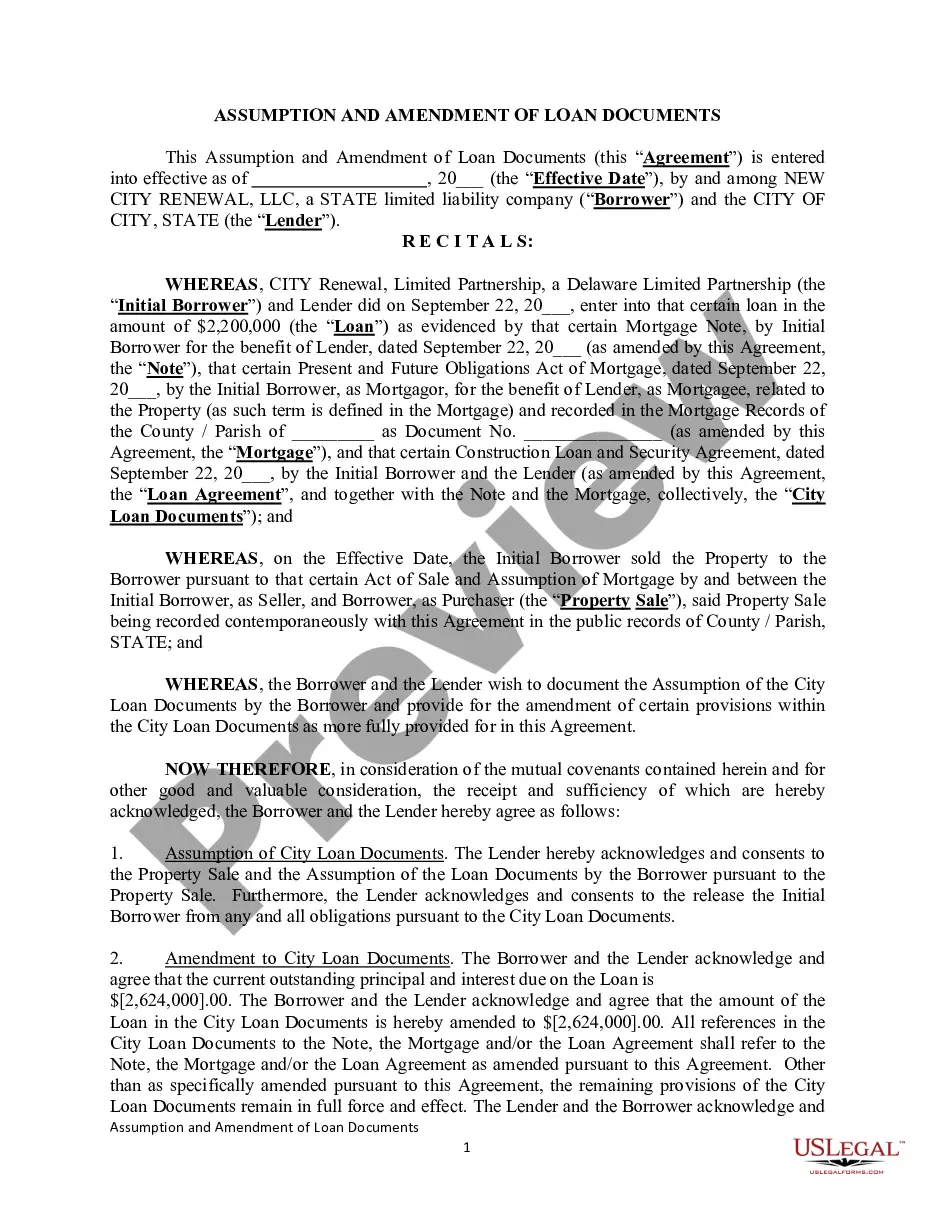

This form is an Assumption Agreement. The form provides that the grantee will assume a lien on property described in the agreement. The assumption will become effective on the date provided in the agreement.

Alabama Assumption Agreement of Loan Payments

Category:

State:

Multi-State

Control #:

US-00424

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Assumption Agreement Of Loan Payments?

Finding the right legitimate papers design can be a battle. Needless to say, there are a lot of layouts available online, but how do you find the legitimate type you will need? Use the US Legal Forms website. The service gives thousands of layouts, including the Alabama Assumption Agreement of Loan Payments, which you can use for organization and personal requires. Every one of the varieties are checked out by specialists and meet federal and state needs.

If you are previously authorized, log in to the bank account and click the Obtain switch to obtain the Alabama Assumption Agreement of Loan Payments. Make use of bank account to appear through the legitimate varieties you might have ordered in the past. Go to the My Forms tab of your bank account and obtain another backup in the papers you will need.

If you are a new consumer of US Legal Forms, listed below are straightforward recommendations for you to adhere to:

- First, make sure you have selected the right type for your personal area/area. You are able to look through the shape making use of the Review switch and study the shape information to guarantee it will be the best for you.

- In case the type is not going to meet your expectations, utilize the Seach area to obtain the right type.

- Once you are certain that the shape is acceptable, click on the Get now switch to obtain the type.

- Select the prices prepare you desire and enter the essential information. Create your bank account and pay money for your order making use of your PayPal bank account or credit card.

- Choose the data file file format and acquire the legitimate papers design to the gadget.

- Full, revise and produce and indicator the received Alabama Assumption Agreement of Loan Payments.

US Legal Forms will be the most significant catalogue of legitimate varieties in which you will find various papers layouts. Use the company to acquire professionally-manufactured files that adhere to condition needs.

Form popularity

FAQ

Assumption of Obligations. New Borrower covenants, promises, and agrees that New Borrower, jointly and severally if more than one, will unconditionally assume and be bound by all terms, provisions, and covenants of the Assumed Loan Documents as if New Borrower had been the original maker of the Assumed Loan Documents.

Calculation. The mortgage assumption value can be calculated as the net present value of the sum of the future monthly payment savings due to the assumable loan rate being lower than the prevailing new loan interest rate.

Loan assumption, however, allows a buyer to take over the current owner's mortgage while the loan's terms ? including the repayment period and interest rate ? remain the same. Ultimately, it can help people get into a home at a lower interest rate even as the housing market around them becomes more expensive.

An assumption agreement, sometimes called an assignment and assumption agreement, is a legal document that allows one party to transfer rights and/or obligations to another party. It allows one party to "assume" the rights and responsibilities of the other party.

When a buyer buys property and assumes a mortgage, the buyer becomes primarily liable for the debt and the seller becomes secondarily liable for the debt. "Assume" means the buyer takes on liability, and the seller is no longer primarily liable. "Subject to" means the seller is not released from responsibility.

Updated March 7, 2022. In real estate transactions, an assumption agreement allows a third party to ?assume? or take over the loan of the property's seller. Mortgages may be assumed when the house is sold, a divorcing spouse is awarded the property in a settlement or when someone inherits property.

An assumable mortgage is a home loan that can be transferred from the original borrower to the next homeowner. The interest rate and payment period stay the same. For example, if a 30-year mortgage is three years old, the person assuming the loan has 27 years to pay it off.

How long does the assumption process take? Assumption TypeProcessing TimeStandard Assumption60 ? 90 DaysAssumption Due to Divorce60 ? 90 DaysAssumption After Death30 ? 60 Days