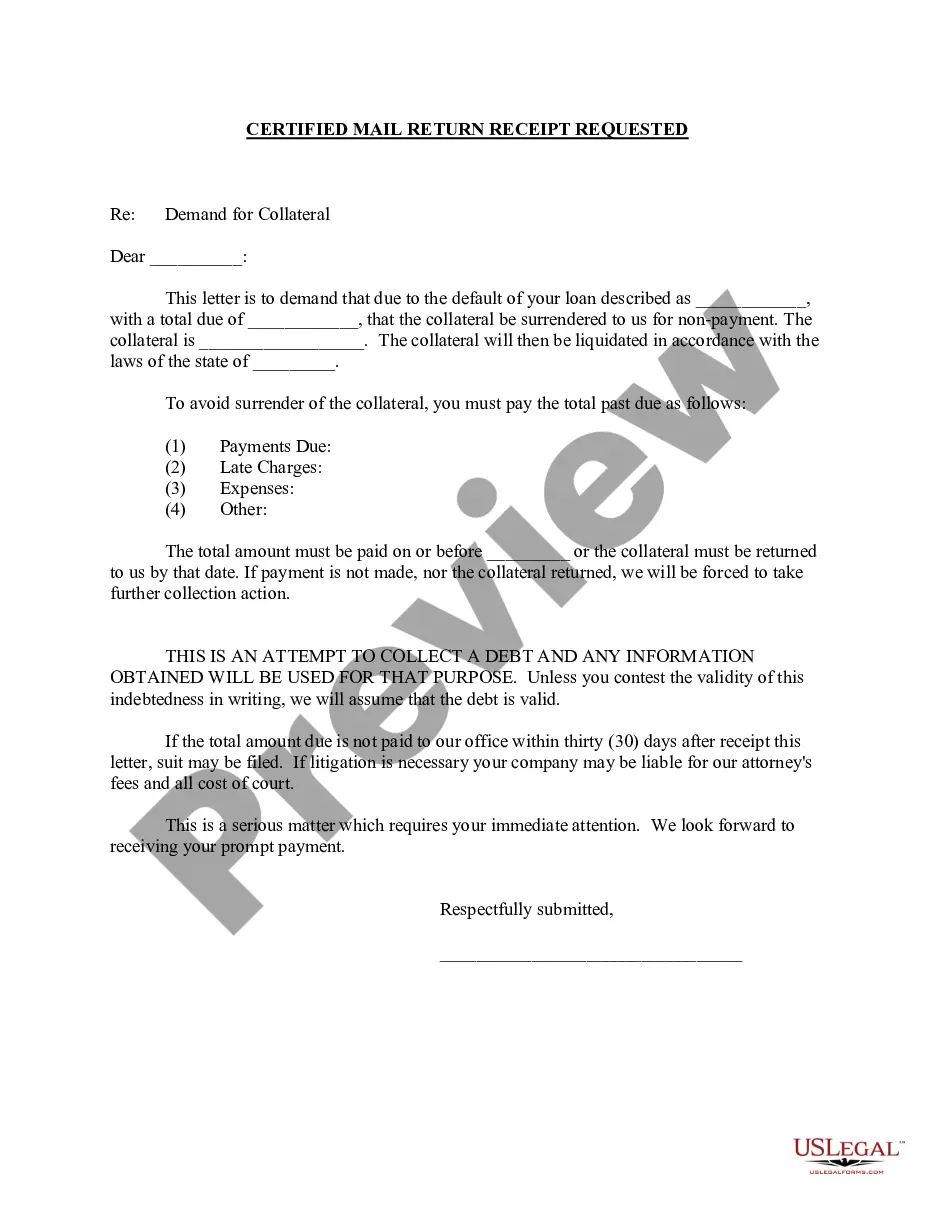

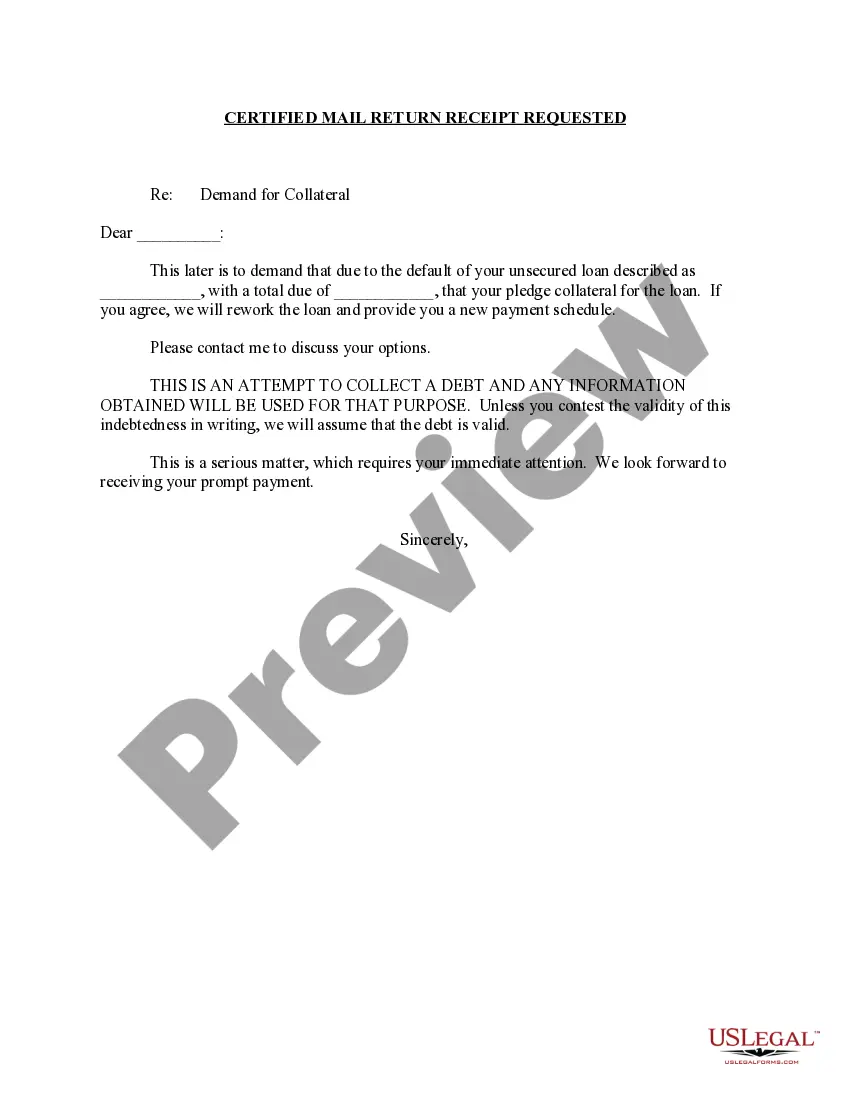

Alabama Demand for Collateral by Creditor is a legal provision that allows a creditor to demand additional collateral from a debtor in order to secure the existing debt or loan agreement. This provision is primarily used in commercial transactions or when lenders want to strengthen their position in case of a default. Under Alabama law, there are different types of demand for collateral by creditors. These include: 1. Alabama Uniform Commercial Code (UCC): This provision is codified under Article 9 of the Alabama UCC, which governs security interests in personal property. It grants a creditor the right to make a written demand for additional collateral from the debtor. 2. Written Demand: The creditor must make a written demand specifying the additional collateral required. This demand can be in the form of a letter or a formal legal notice, ensuring that the debtor is aware of the request for additional security. 3. Default or Risk of Default: The demand for collateral by the creditor is usually triggered by the default of the debtor. In case the debtor fails to make payments, breaches the terms of the loan agreement, or shows signs of financial instability, the creditor may request additional collateral to minimize the potential losses. 4. Scope of Additional Collateral: The creditor has the right to determine the type and value of the additional collateral to be provided. This can include real estate, vehicles, equipment, inventory, accounts receivable, or any other valuable asset. The value of the additional collateral must be reasonably related to the outstanding debt. 5. Negotiation and Agreement: Once the demand is made, the debtor and creditor can negotiate the terms of the additional collateral. The debtor can propose alternatives or negotiate the inclusion of certain assets. However, the final decision lies with the creditor, who can choose to accept or reject the debtor's proposals. 6. Consequences of Non-Compliance: If the debtor fails to comply with the demand for additional collateral, the creditor may exercise their legal remedies. This can include initiating legal proceedings, repossessing the existing collateral or assets, or enforcing the security interest through foreclosure or a public sale. 7. Transparency and Fairness: The Alabama Demand for Collateral by Creditor aims to promote transparency and fairness in commercial transactions. It ensures that creditors have the ability to protect their interests and secure their investment, while also allowing debtors the opportunity to negotiate and propose alternative forms of collateral. It is important to note that the specific provisions and processes regarding the Alabama Demand for Collateral by Creditor may vary based on the details of the loan agreement, the type of transaction, and any additional contractual terms agreed upon by the parties involved. Therefore, it is always recommended consulting legal professionals or review the applicable laws and regulations to ensure compliance.

Alabama Demand for Collateral by Creditor

Description

How to fill out Alabama Demand For Collateral By Creditor?

US Legal Forms - one of the biggest libraries of legitimate kinds in the States - delivers a wide array of legitimate papers web templates you may download or print. Using the internet site, you will get a huge number of kinds for organization and specific purposes, categorized by types, suggests, or keywords.You can find the most recent versions of kinds just like the Alabama Demand for Collateral by Creditor in seconds.

If you have a subscription, log in and download Alabama Demand for Collateral by Creditor in the US Legal Forms catalogue. The Download option will appear on each and every type you perspective. You have accessibility to all previously downloaded kinds in the My Forms tab of your respective account.

If you want to use US Legal Forms initially, here are easy recommendations to help you get began:

- Ensure you have selected the correct type to your area/area. Click on the Preview option to check the form`s content. Read the type outline to ensure that you have selected the right type.

- In the event the type doesn`t match your specifications, utilize the Research area at the top of the monitor to discover the one that does.

- In case you are happy with the shape, verify your choice by clicking the Buy now option. Then, pick the costs strategy you want and give your qualifications to sign up on an account.

- Procedure the deal. Use your bank card or PayPal account to accomplish the deal.

- Choose the formatting and download the shape on your device.

- Make modifications. Complete, revise and print and indication the downloaded Alabama Demand for Collateral by Creditor.

Every web template you included with your money lacks an expiry particular date which is your own eternally. So, if you want to download or print yet another duplicate, just check out the My Forms area and then click around the type you will need.

Obtain access to the Alabama Demand for Collateral by Creditor with US Legal Forms, probably the most comprehensive catalogue of legitimate papers web templates. Use a huge number of specialist and express-certain web templates that meet your business or specific requirements and specifications.