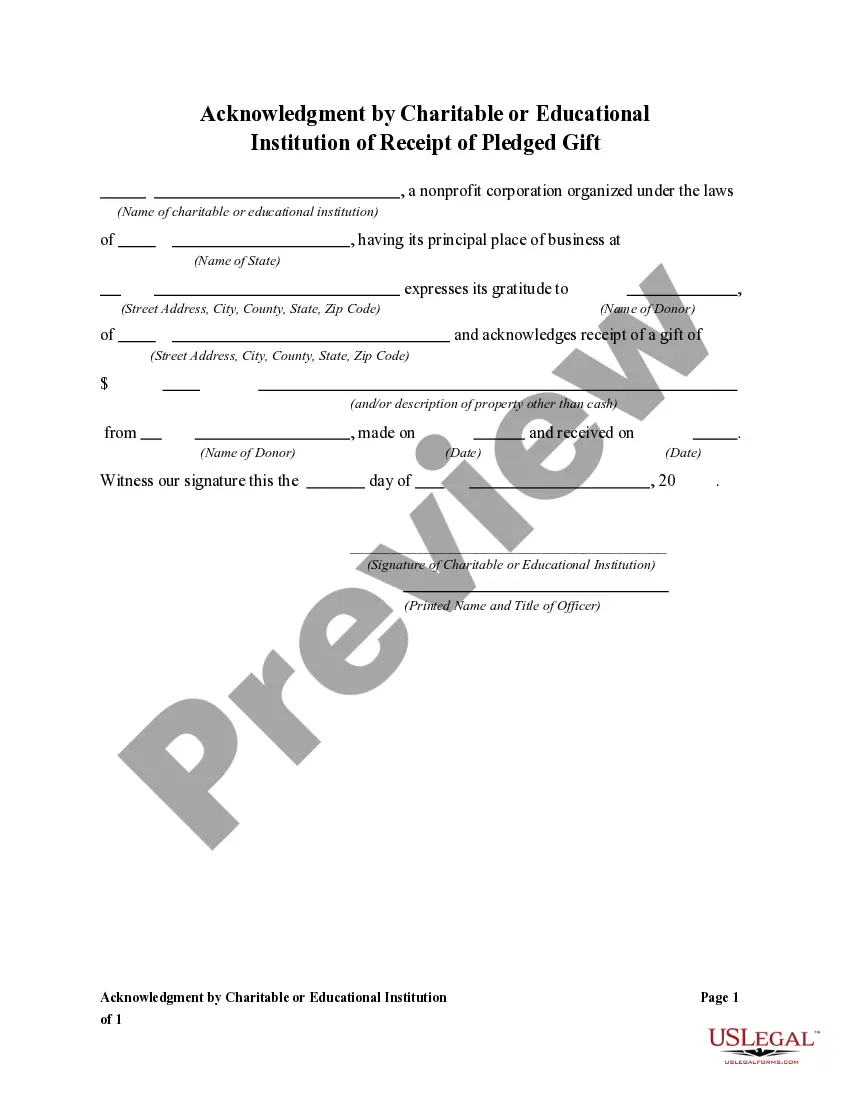

Alabama Acknowledgment by Charitable or Educational Institution of Receipt of Pledged Gift

Description

How to fill out Acknowledgment By Charitable Or Educational Institution Of Receipt Of Pledged Gift?

You can spend countless hours online trying to locate the proper legal document format that meets the federal and state requirements you need. US Legal Forms offers thousands of legal templates that are vetted by professionals. You can obtain or generate the Alabama Acknowledgment by Charitable or Educational Institution of Receipt of Pledged Gift from your assistance.

If you already possess a US Legal Forms account, you can sign in and click on the Download button. After that, you can complete, modify, print, or sign the Alabama Acknowledgment by Charitable or Educational Institution of Receipt of Pledged Gift. Every legal document format you acquire is yours forever. To get another copy of any obtained form, visit the My documents section and click on the relevant button.

If you are using the US Legal Forms site for the first time, follow the simple instructions below: First, ensure that you have selected the correct document format for the region/city of your choice. Review the form description to verify you have chosen the right form. If available, use the Review button to examine the document format as well.

Utilize professional and state-specific templates to address your business or personal needs.

- If you wish to obtain another version of the form, use the Search field to find the format that meets your needs and requirements.

- Once you have located the format you want, click on Buy now to proceed.

- Choose the pricing plan you prefer, enter your details, and create an account on US Legal Forms.

- Complete the transaction. You can use your credit card or PayPal account to pay for the legal document.

- Select the format of the document and download it to your device.

- Make adjustments to your document if possible. You can complete, modify, sign, and print the Alabama Acknowledgment by Charitable or Educational Institution of Receipt of Pledged Gift.

- Download and print thousands of document templates using the US Legal Forms site, which offers the largest selection of legal forms.

Form popularity

FAQ

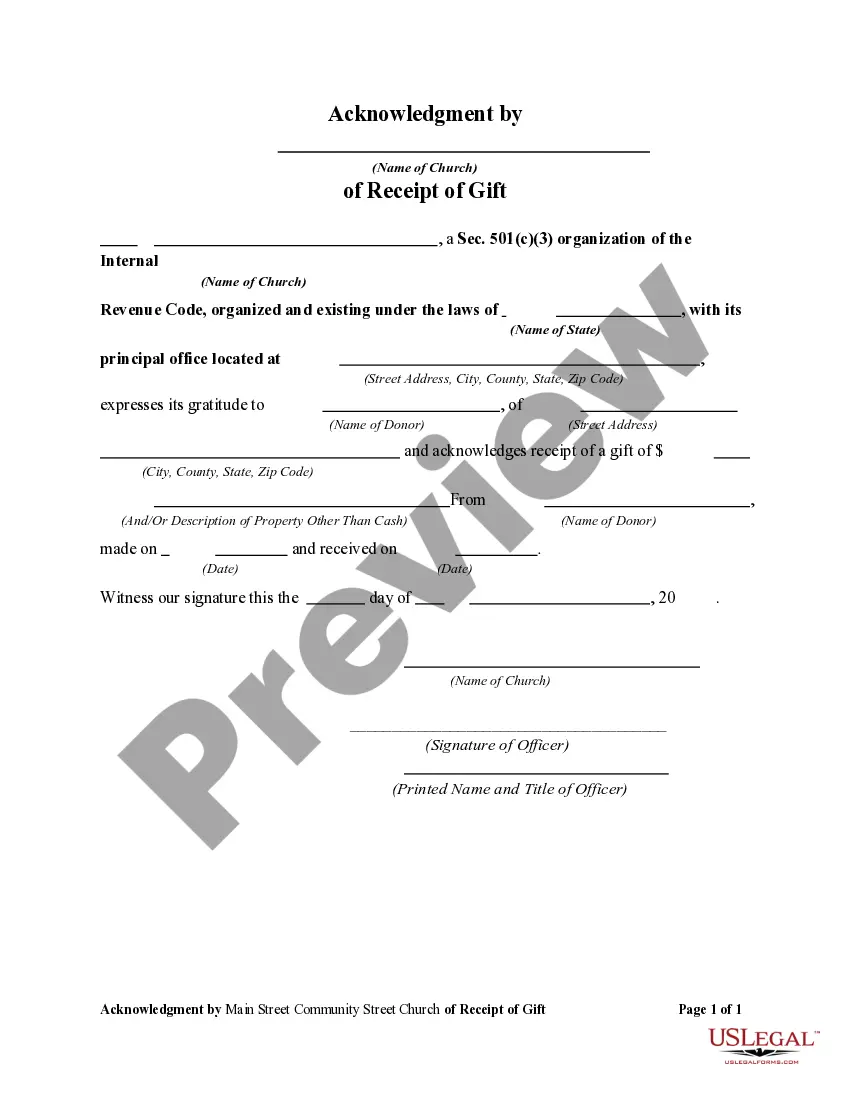

The following is an example of a written acknowledgment where a charity accepts contributions in the name of one of its activities: "Thank you for your contribution of $250 to (Organization) made in the name of its Kids & Families program. No goods or services were provided in exchange for your donation."

The following is an example of a written acknowledgment where a charity accepts contributions in the name of one of its activities: "Thank you for your contribution of $250 to (Organization) made in the name of its Kids & Families program. No goods or services were provided in exchange for your donation."

Sample Donor Acknowledgement Letter for Non-Cash Donation On [DATE], you donated [DESCRIPTION ? WITHOUT MONETARY VALUE]. This gift is greatly appreciated and will be used to support our mission. In exchange for this contribution, you received [GOODS OR SERVICES ? WITH ESTIMATE OF FAIR MARKET VALUE].

Ing to the IRS, donation tax receipts should include the following information: The name of the organization. A statement confirming that the organization is a registered 501(c)(3) organization, along with its federal tax identification number. The date the donation was made.

A good example of a donation receipt text would be: ?Thank you for your cash contribution of $300 that (organization's name) received on December 12, 2015. No goods or services were provided in exchange for your contribution.?

What do you need to include in your donation acknowledgment letter? The donor's name. The full legal name of your organization. A declaration of your organization's tax-exempt status. Your organization's employer identification number. The date the gift was received. A description of the gift and the amount received.

For contributions of cash, check, or other monetary gift (regardless of amount), you must maintain a record of the contribution: a bank record or a written communication from the qualified organization containing the name of the organization, the amount, and the date of the contribution.

Here are basic donation receipt requirements in the U.S.: Name of the organization that received the donation. A statement that the nonprofit is a public charity recognized as tax-exempt by the IRS under Section 501(c)(3) Name of the donor. The date of the donation. Amount of cash contribution.