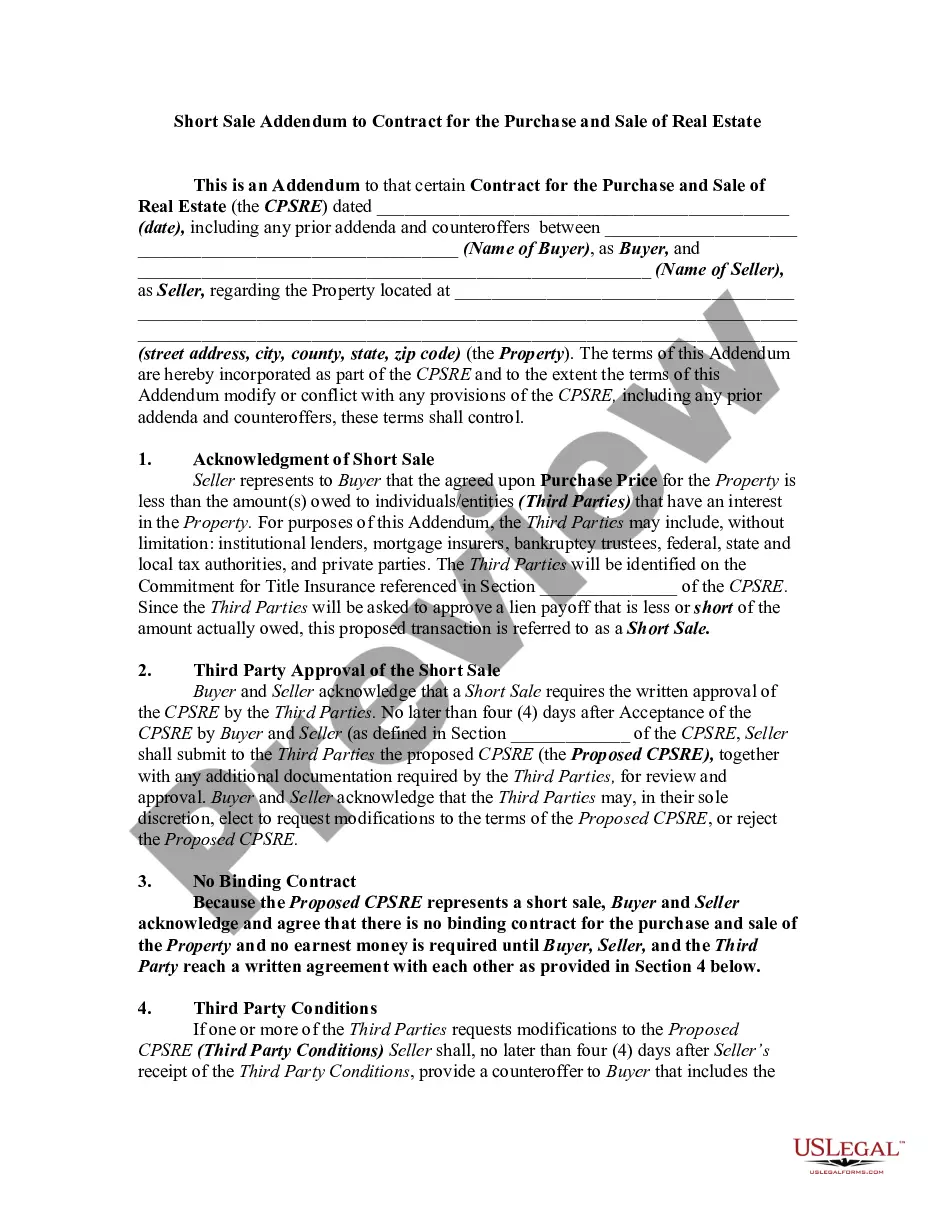

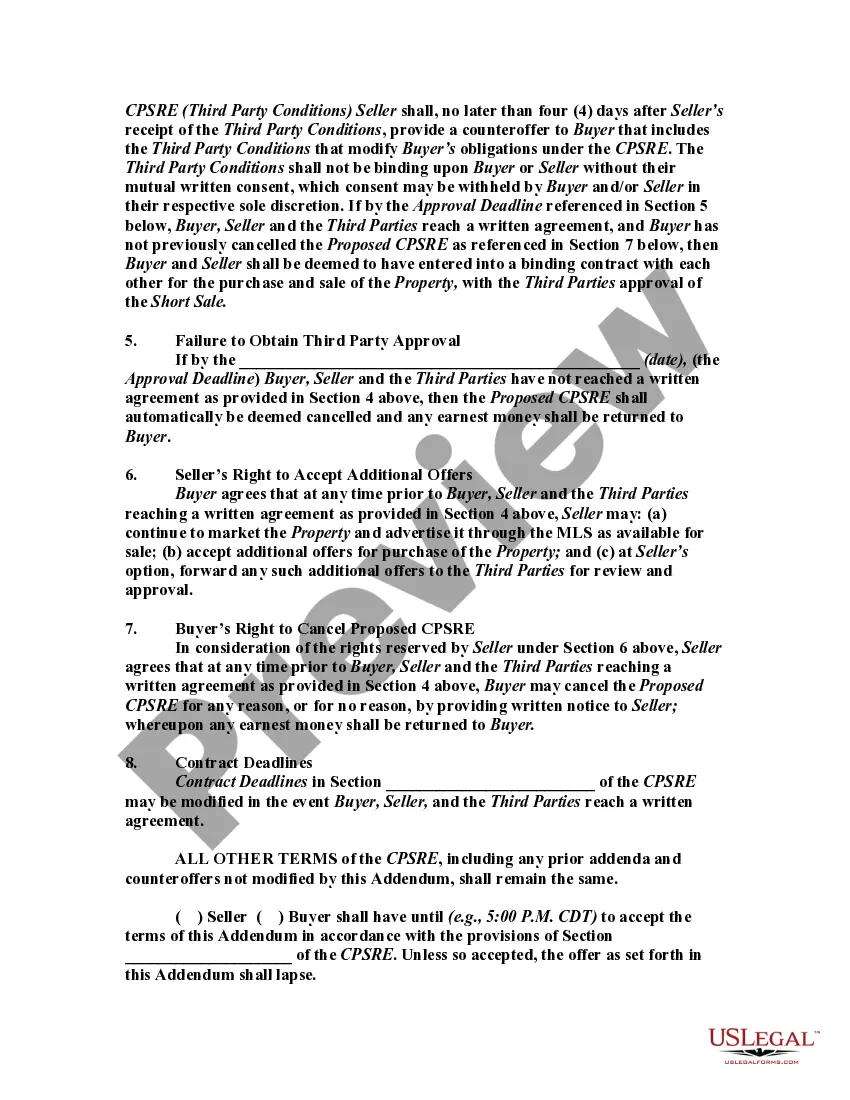

In real estate, a short sale occurs when a bank or mortgage lender agrees to discount a loan balance due to an economic hardship on the part of the mortgagor (i.e., the seller). Circumstances determine whether or not banks will discount a loan balance. These circumstances are usually related to the current real estate market climate and the individual borrower's financial situation. A short sale typically is executed to prevent a home foreclosure. Often a bank will choose to allow a short sale if they believe that it will result in a smaller financial loss than foreclosing.

This form is a sample of an Addendum to a standard real estate sales contract in order to incorporate the short sales provisions. This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

The Alabama Short Sale Addendum to Contract for the Price, Purchase and Sale of Real Estate is a crucial document in real estate transactions where the property being purchased is under a short sale. This addendum outlines specific terms and conditions unique to short sales, ensuring that both the buyer and seller are protected throughout the process. The Alabama Short Sale Addendum includes several important elements to address the complexities of short sales. These may vary depending on the specific circumstances, but there are two common types: 1) Alabama Short Sale Addendum to Contract for Price, Purchase, and Sale of Real Estate — This is the standard addendum used in most short sale transactions. It covers the basic requirements and provisions necessary to facilitate the short sale process successfully. 2) Alabama Short Sale Addendum with Special Conditions — In some cases, additional special conditions may be necessary to address unique circumstances or requirements in a specific short sale transaction. These conditions might include stipulations related to the seller's lender approval, documentation deadlines, or other specific terms unique to the property. The Alabama Short Sale Addendum covers various essential aspects, including: 1) Purchase Price: This section outlines the agreed-upon price for the property. In a short sale, the purchase price is typically lower than the property's current market value to accommodate the seller's financial situation. 2) Earnest Money Deposit: This clause specifies the amount of earnest money the buyer is required to deposit within a specified timeframe to solidify their commitment to the transaction. 3) Financing Contingency: This provision allows the buyer to back out of the contract if they are unable to secure financing within a specified period. It safeguards both parties, considering the complexities and potential delays involved in short sale transactions. 4) Seller's Lender Approval: Since the seller's lender(s) must approve the short sale, this section details the necessary steps for the seller to obtain lender approval, including potential timeframes and the expected cooperation of all parties involved. 5) Property Condition: This portion addresses the condition of the property and whether it will be sold in as-is condition or if repairs and inspections are required. 6) Closing Date and Extensions: The Alabama Short Sale Addendum outlines the expected closing date and includes provisions for possible extensions due to lender approval, unforeseen circumstances, or other factors. It is vital to work with a qualified real estate professional or attorney who is knowledgeable about Alabama short sales and can assist in accurately preparing and reviewing the appropriate addendum for the specific transaction.